Key takeaways

- To start your manual payroll, gather information about each employee’s pay, benefits, deductions, and tax withholding.

- Tread carefully: You’ll need a thorough understanding of federal, state, and local labor laws and tax codes if you’re doing payroll by yourself.

- You can use a payroll record book, spreadsheet, or our free payroll template if you want to do your own payroll by hand.

- Manual payroll is prone to errors that could result in severe fines from tax and labor law violations, but using free or low-cost payroll software is usually safer and more reliable.

Disclaimer: TechnologyAdvice is not a tax or legal service/agency. The portions of this article about federal, state, and local employee and employer tax withholdings are for informational purposes only and are not intended as legal advice. Please consult your accountant, tax expert, or labor law attorney for specific situations.

- March. 04, 2026: Robie Ann Ferrer updated the copy and sample payroll computations to reflect 2026 tax details. She also revised some of the screenshots and added relevant links.

- Aug. 28, 2025: Hanna Sillo added copies and updated the elements in some sections.

- May 13, 2025: Robie Ann Ferrer tweaked the copy to improve readability, adjusted link placements, and corrected some of the calculations based on the changes to the IRS tax table.

- Apr. 30, 2024: Jessica Dennis reviewed and rewrote most of the copy to include more practical steps for completing payroll yourself. She also added relevant links, an infographic, and a template download to help.

Payroll is more than just paying people. A big part of it is also keeping your business compliant and your people satisfied with their compensation. For people handling small businesses, doing payroll yourself can save money, but it is also risky if you are not familiar with the rules.

In this guide, I’ll walk you through the steps of computing and processing payroll yourself. It also contains a spreadsheet for computing payroll, including the pros and cons of doing it manually and of using an online payroll system, like QuickBooks Workforce.

With QuickBooks Workforce (formerly QuickBooks Payroll), you get automatic wage calculations, payroll tax filing services, and basic HR tools for managing employee data and documents. And if you use its accounting software, QuickBooks Online, your payroll information is easily synchronized with the general ledger, eliminating the need for manual data entry and reducing the risk of errors.

Free payroll spreadsheet template

Do-it-yourself (DIY) payroll can be scary, but our payroll spreadsheet template is a great starting point. Use it calculate paychecks for your employees, including tax liabilities at the federal and state levels.

Download our payroll template for free:

How to do your own payroll

Payroll is a complex and time-consuming process. Your employees depend on it for their livelihoods, so getting it right is crucial. If you make payroll mistakes, you’re not just dealing with unhappy workers; you could also face fines, audits, and even jail time, depending on the error and its frequency and severity.

That said, running payroll yourself is possible. And if you’re a new startup or small business owner with 10 or fewer employees, it’s often more practical to process payroll manually before investing in a service or software solution.

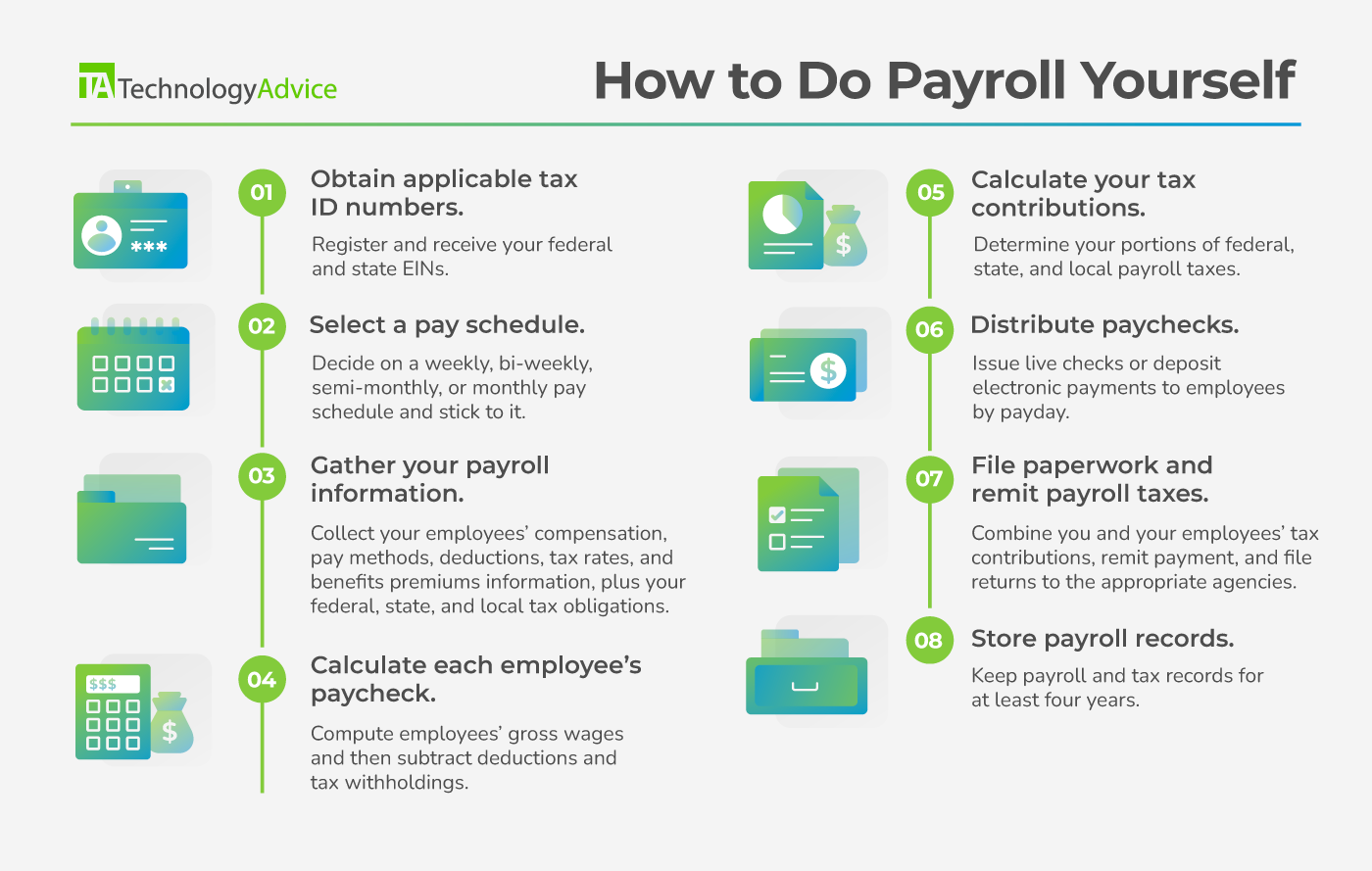

Here’s a summary of the steps involved:

If learning how to do payroll yourself is daunting, you have other options. Check out our Top Free Payroll Software and Best Payroll Software guides for free and low-cost solutions that can handle the majority of the process for you.

Before you start

There are three things to do before processing payroll for the first time:

- Familiarize yourself with the state and local labor and tax laws of your employees. This how-to goes into depth about calculating federal payroll taxes but only provides cursory guidance on state and local laws. Understanding the payroll laws where your employees live and work will reduce the likelihood of inaccurate deductions and tax contributions from you and the employee.

- Understand common payroll terms. Jump to our HR glossary and learn about this guide’s different terms.

- Decide on your DIY method. You’ll need a paper payroll record book with a pen and calculator or a basic computer spreadsheet program to calculate and track your payroll expenses.

Pro tip: Download our payroll template to get started.

Further, this guide will only help with how to do your own payroll for workers classified as employees, not contractors. And while paying contract workers is similar to paying business vendors, they’re not identical processes.

Want a refresher? Check out the Quick Glossary: Payroll (TechRepublic Premium)

If you only pay contractors

There are several software platforms that can simplify the process. Most vendors typically offer contractor-only plans at lower costs than their full-service payroll subscriptions. For options, check out our Top Contractor Payroll Solutions guide.

Step 1: Obtain applicable tax ID numbers

Before doing any manual payroll, you must first apply for a federal Employer Identification Number (EIN) with the IRS. You will need this EIN to:

- Open a business bank account

- Hire employees

- File federal, state, and local taxes

You may also need to obtain separate tax IDs for each state, county, and/or city where your business operates, depending on your tax obligations.

After you receive your EINs, register with the Electronic Federal Tax Payment System (EFTPS). All employers must use this system to electronically remit payroll tax payments, so it’s a good idea to have your account ready before your first payday.

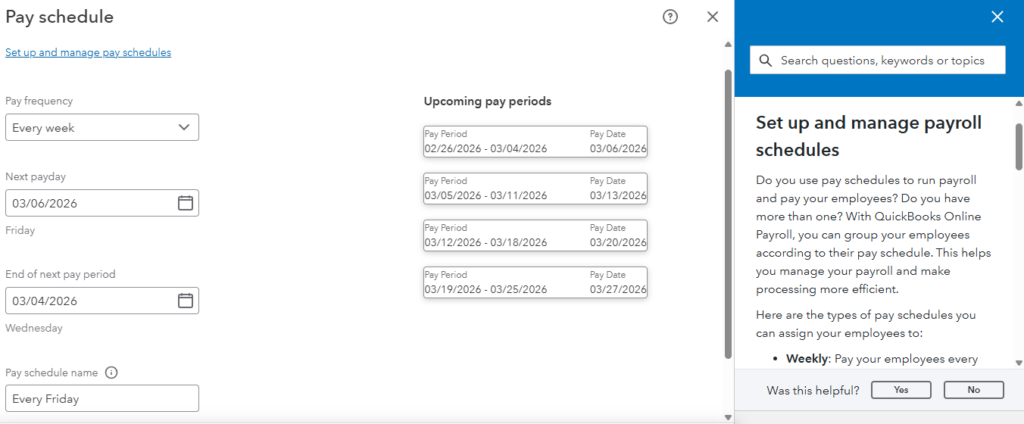

Step 2: Select a pay schedule

The four most common pay schedules you’ll choose from when processing payroll manually are:

- Weekly (52 pay periods per year)

- Bi-weekly (26 pay periods per year)

- Semi-monthly (24 pay periods per year)

- Monthly (12 pay periods per year)

If you use a pay processing program like QuickBooks Workforce, selecting pay schedules for employees is easy. It supports all pay periods and comes with an in-app guide you can access at any time if you need help setting this up.

To learn more about its features, visit its website.

Of course, the best schedule for your business depends on your cash flow and the types of workers you have.

Example: Let’s say you offer a monthly subscription service and bill customers on the 15th or the last day of the month, depending on when they signed up.

- A semi-monthly payroll schedule would align with your cash influx and ensure you have enough money to pay your labor costs on time.

- In contrast, a weekly schedule may be easier if you have many non-exempt hourly employees, as it is much simpler to calculate overtime payments.

Factoring in the employee experience is also important, as workers in some industries, like construction, may expect their paychecks at a particular frequency.

Heads up!

While the Fair Labor Standards Act (FLSA) doesn’t set how often employees must be paid, most states have pay schedule laws regulating payday frequency and how long you can wait to pay employees following the end of a pay period.

To see the pay frequency laws that apply to you, check out the Wage and Hour Division’s (WHD) State Payday Requirements.

Step 3: Gather your payroll information

At the end of your pay period, you’ll need the following information to process payroll:

To calculate employees’ earnings, you’ll need their compensation information. Salary-exempt employees will receive the same gross pay each payroll, with a few exceptions. However, for hourly non-exempt employees, you’ll need their:

- Straight-time rate.

- Overtime rate.

- Premium pay rates for any shift differentials.

- Hours worked at each pay rate in the pay period*

- Any paid time off (PTO) hours for things like holidays, injury/illness, or vacation

You may also need to collect information on any supplemental wages for your employees, including:

- Commissions

- Bonuses

- Tips

- Reimbursements

*Note: The FLSA defines overtime as any hours worked over 40 a week. However, some states have more stringent laws. California’s overtime law, for example, requires employers to pay employees at their overtime rate for any hours worked over eight in a day. Make sure to double-check state requirements before calculating overtime.

You’ll need to collect your employees’ W-4 forms to determine what they owe per paycheck in Federal Income Tax (FIT). You should also gather their state and local W-4 equivalents, if applicable. Each form will help you determine the appropriate tax withholding amounts since they depend on the employee’s tax filing status, income level, and number of dependents.

In addition to income taxes, employees pay their portion of Federal Insurance Contribution Act (FICA) taxes from their paychecks. As an employer, you are responsible for calculating, withholding, and remitting these taxes to the appropriate agency on your employees’ behalf.

What if I don’t have an employee’s W-4 form?

Collecting Form W-4 from new employees should be part of your onboarding practices. If they fail to provide you with a completed form by the time you process payroll, you must still pay them per your established pay schedule.

In this case, you can determine their tax payments as if they are filing single without any dependents or additional withholding amounts. However, you must still check the federal tax tables to calculate FIT deductions correctly based on the employee’s taxable earnings and pay schedule. You’ll also need each state’s income tax rates and tables, if applicable.

You’ll need to collect information on items employees pay through payroll. Typical employee deductions include:

- Health, dental, and vision insurance premiums.

- Disability and life insurance premiums.

- Commuter benefits.

- Flexible Spending Account (FSA) and Health Savings Account (HSA) contributions

- Retirement plan contributions, like 401(k) plans

- Wage garnishments

- Company expenses, such as uniform or equipment deductions.

- Other voluntary deductions for things like pet insurance or charitable donations.

To determine each employee’s premium amount for their plan, you’ll need their insurance enrollment forms plus information from your broker and carrier. Employees complete similar paperwork during open enrollment season. Other deductions, like uniforms, also need written authorization before you can deduct the amount from their paychecks.

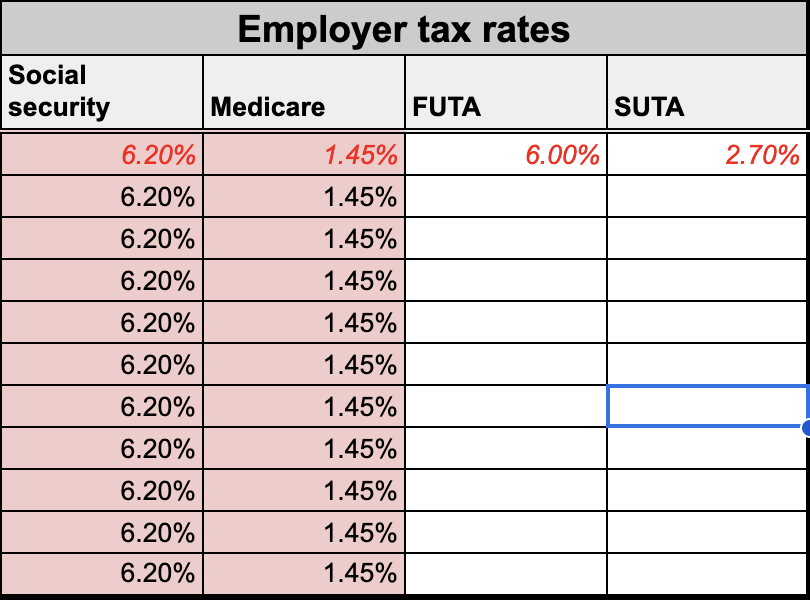

You are responsible for withholding and remitting your employees’ portion of payroll taxes. There are also several payroll taxes that only employers pay, including:

- Federal Unemployment Tax (FUTA): At 6%, but check state regulations for additional FUTA rules

- State Unemployment Tax (SUTA): Varies by state

- FICA: Shared between you and the employee—you match the employee’s contribution of 6.2% for Social Security and 1.45% for Medicare

You should also look into workers’ compensation (WC) insurance requirements for your employees’ states. Most employers traditionally receive a bill from their private insurance carriers or state fund with the premium amounts they owe outside of payroll.

Similarly, you’ll receive health insurance premiums and other benefits from your carriers. These payments usually occur outside payroll, but you’ll want to record what you pay monthly for end-of-year Form 1095-C and Form W-2.

Pro tip: If you’re using our payroll template, you must add your payroll tax rates in the “Employer taxes” tab under the section “Employer tax rates.” Since FICA rates are the same for everyone, you only need to enter your FUTA and SUTA rates, plus any other employer payroll taxes specific to your employee’s state and municipality. The rest of the chart auto-populates as you complete payroll.

Another critical part of running payroll is knowing each employee’s preferred payment method. It can be by paycheck, pay card, or direct deposit.

You must collect direct deposit authorization forms from employees with account and routing numbers for any electronic payment method. It’s also wise to request a voided check, bank letter, or pay card form with account and routing numbers from the issuing bank to verify that you received the correct information.

Step 4: Calculate each employee’s paycheck

Let’s use an example to calculate an employee’s paycheck step-by-step. Here’s an employee record for Mikhail Scotch, the regional manager at a paper company called Blunder Bifflin:

Name: Mikhail Scotch

Title: Regional Manager

Branch: Scranton, PA

Straight-time rate: $30 per hour

Overtime rate: $45 per hour

Pay schedule: Weekly

Medical: $200 per paycheck

Dental: $27 per paycheck

Vision: $3 per paycheck

Pet: $30 per paycheck

401(k) contribution: $150 per paycheck

Garnishments: $25 per paycheck

Filing status: Married, filing jointly

Dependents: One

Expected interest payments: $1,500

Additional withholding amount: $10

Pennsylvania state income tax rate: 3.07%

To calculate Mikhail’s paycheck amount by hand, we need to determine his gross pay, deductions, taxes, and net pay in order. This is where it can get tricky—take your time and double-check each detail to avoid costly mistakes.

You should calculate your employees’ payroll deductions before their tax withholdings, since deductions affect what part of their income is taxable. For example, the IRS considers retirement contributions and medical, dental, vision, and commuter benefits premiums to be pre-tax deductions for calculating employees’ federal income tax (FIT) withholdings.

By comparison, only health insurance premiums are pre-tax deductions for determining FICA withholdings. You’ll want to confirm what each state and local tax considers pre- and post-tax deductions so you don’t over- or under-withhold taxes.

With this in mind, let’s determine Mikhail’s total deductions plus what portion of his wages are taxable for FIT and FICA. First, compute Mikhail’s total deductions for health insurance, pet insurance, $401(k), and garnishment:

$200 + $27 + $3 + $30 + $150 + $25 = $435 total deductions

Now, let’s deduct Mikhail’s health insurance premiums and retirement contribution from his gross pay to determine taxable gross pay for FIT:

$1,290 – ($200 + $27 + $3 + $150) = $910 taxable gross pay (FIT)

And finally, let’s do the same for FICA. Remember, the IRS considers retirement contributions post-tax deductions for determining taxable income for FICA, so we’ll remove Mikhail’s 401(k) contribution from our formula.

$1,290 – ($200 + $27 + $3) = $1,060 taxable gross pay (FICA)

Now, take note of these totals. We’ll need them to calculate Mikhail’s tax withholdings next.

To calculate tax withholdings, make sure you have the employee’s taxable income amounts from the previous step, their W-4 forms, and the appropriate rates for state and local taxes. In the sections below, I’ll show you how to calculate the most common tax withholding amounts: FIT, state income, and FICA.

There are two ways to calculate employee FIT withholdings: wage bracket or percentage. Although the bracket method is easier, it only applies to employees who make less than $100,000 annually. We’ll use the percentage method since it covers a broader range of compensation amounts and produces more accurate tax withholdings.

The easiest way to determine the employee’s withholding amount for FIT is to use the percentage method tables included in IRS Publication 15-T. Using Mikhail’s information, let’s take a look at it together:

To determine the adjusted wage amount, divide any additional, non-job-related income Mikhail expects to receive this year, such as interest or dividend payments, by the number of pay periods in the year. Then add this amount to Mikhail’s taxable gross income for this paycheck.

If an employee wants to reduce the amount you withhold from their paycheck for FIT, their W-4 will include an annual amount they want deducted from their FIT payments. Like above, you’ll divide this amount by the number of pay periods in the year, but subtract the amount from their taxable gross income.

You can find this information listed on lines 4(a) and 4(b) of the W-4 form. For Mikhail, he expects to receive $1,500 in interest payments for the year and does not have anything on line 4(b). With this, let’s figure out his adjusted wage amount:

| 1. Taxable gross pay (FIT) | $910 |

| 2. Expected non-employee extra income for the year (line 4(a) from W-4 form) | $1,500 |

| 3. Additional income per pay period ($1,500 / 52 pay periods) | $28.85 |

| 4. Add the additional amount to taxable gross pay (FIT) | $938.85 |

| 5. FIT deductions (line 4(b) from W-4 form) | $0 |

| 6. FIT deductions per pay period ($0 / 52) | $0 |

| 7. Subtract the deduction amount from the amount in Step 4 ($938.85 – $0) | $938.85 |

| Adjusted wage amount: | $938.85 |

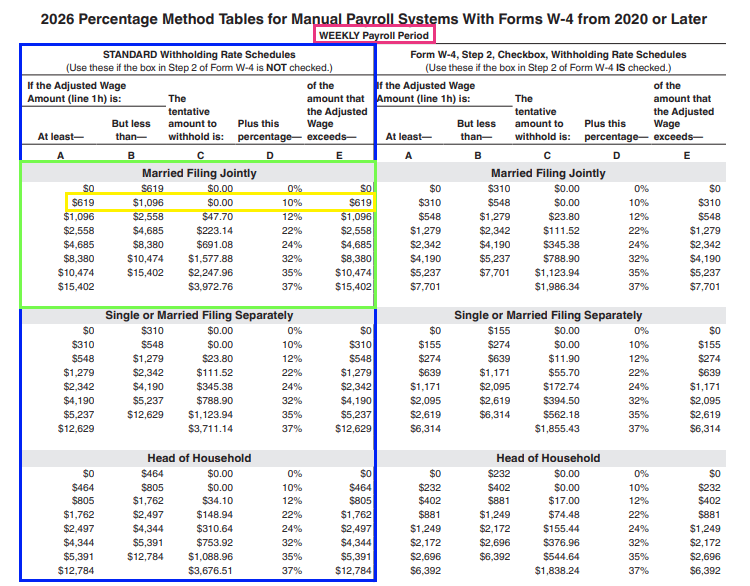

Next, we’ll calculate Mikhail’s tentative withholding amount based on his adjusted wage from Step 1. You’ll also need the IRS’s percentage withholding tables listed on Publication 15-T, Mikhail’s filing status, multiple job status, and payroll schedule.

First, find the percentage withholding table for a weekly payroll schedule. Next, narrow your chart scope by whether Mikhail works multiple jobs in Step 2 of the W-4 form. Then, find the section of the table based on Mikhail’s filing status. And finally, we’ll look at the information in the row of that chart based on his adjusted wage amount.

Mikail has a weekly pay schedule, does not work multiple jobs, files his taxes as married, jointly, and has an adjusted wage amount of $938.85. According to the 2026 IRS table, his adjusted wage amount is between $619 and $1,096, so the tentative amount to withhold is $0 plus 10% of any amount over $619.

So, to calculate the tentative withholding amount, we’ll need to do the following:

| 1. Subtract the lowest amount in the employee’s wage bracket from their adjusted wage amount ($938.85 – $619) | $319.85 |

| 2. Multiply the amount from Step 1 by the percentage amount of that wage bracket ($319.85 X 0.10) | $31.98 |

| 3. Add the amount from column C in the percentage wage table to the amount in Step 2 ($0 + $31.98) | $31.98 |

| Tentative withholding amount: | $31.98 |

If you need help finding the right wage bracket, check out how we found Mikhail’s in the picture below.

Employees may claim tax credits for dependents by marking Step 3 of the W-4 form. Like how we calculated Mikhail’s adjusted wage amount, we’ll take the total tax credit amount in Step 3 of the W-4 form and divide it by the number of pay periods in the year to determine how much tax credit the employee receives per paycheck.

In Mikhail’s case, he has one qualifying dependent under the age of 17, which is equivalent to a $2,000 annual tax credit. Here’s how it affects his FIT withholdings for this paycheck:

| 1. Total amount for qualifying dependents (Step 3 of W-4 form) | $2,000 |

| 2. Total tax credit per pay period ($2,000 / 52) | $38.46 |

| 3. Subtract the amount above from the tentative withholding amount ($31.98 – $38.46) | $0* |

| Tentative withholding amount with tax credits | $0 |

*Note: If the amount is less than 0, write $0.

Finally, we’ll add any additional amounts the employee wants withheld from each paycheck to get their final withholding amount. You can find these amounts on line 4(c) of the employee’s W-4 form. For Mikhail, he wants an additional $10 withheld every paycheck for federal income tax.

Considering Mikhail’s filing status and tax credits, his tentative withholding amount is currently $0. Once we add the additional withholding amount to his tentative withholding amount, we’ll get what we actually withhold from his paycheck for FIT:

$0 (tentative withholding amount with tax credits) + $10 (additional withholding amount per pay period) = $10 (final withholding amount for FIT)

You must also deduct state and local income taxes depending on where your employee lives and works. You may even be responsible for withholding other state- or local-specific taxes. You should check with the state’s labor department for this information.

Mikhail lives and works in Pennsylvania, which uses a flat 3.07% for determining state income tax withholdings based on the employee’s taxable gross income.* So Mikhail’s total state income tax withholding is:

$910 (taxable gross pay) X 0.0307 (Pennsylvania income tax rate) = $27.94 (total state income tax)

*Note: Pennsylvania employees must also pay local income and services taxes from their paychecks. They are also responsible for contributing a small percentage to SUTA. However, for simplicity, we only focus on federal and employee state income taxes in this guide.

Employees pay a flat 6.2% for Social Security and 1.45% for Medicare. These two taxes also go by Federal Insurance Contribution Act (FICA) contributions.

Remember the taxable gross wages for FICA we calculated earlier? Now we’ll use that to determine Mikhail’s withholdings for FICA:

$1,060 (taxable gross pay for FICA) X 0.062 = $65.72 (Social Security tax)*

$1,060 (taxable gross pay for FICA) X 0.0145 = $15.37 (Medicare tax)**

*You can only calculate and withhold Social Security tax on the first $184,500 of FICA taxable gross income the employee earns with you as of 2026. Monitor employees’ yearly taxable income and stop withholding once they reach that threshold.

**Employees must pay an additional Medicare tax of 0.9% on any taxable gross income over $200,000 for single filers. The limit changes to over $250,000 for married employees filing jointly and over $125,000 for married workers filing separately. There is no employer match for the additional Medicare tax. Be sure to track the employee’s total income earned with you throughout the year and adjust the tax amount accordingly.

The last step is calculating the employee’s net pay, which is the employee’s gross pay minus all deductions and tax withholdings. The net pay represents the actual amount of their paycheck.

So, let’s see what Mikhail takes home:

| 1. Employee’s gross pay | $1,290 |

| 2. Total deductions (outside taxes) | $435 |

| 3. Total taxes ($10 + $27.94 + $65.72 + $15.37) | $119.03 |

| Net pay [$1,290 – ($435 + $119.03)] | $735.97 |

Save time and effort: If this seems too much to do by hand, our downloadable payroll template can do the calculations for you. Or you can get a pay processing system like QuickBooks Payroll. It computes wages and deductions, automatically produces payslips for each pay period, and provides access to a wide range of payroll reports for viewing pay details, tax liabilities, and more.

Additional examples

There may be instances where you have to compute employee payments with tip credits or adjust rates because of pay adjustments. Here’s how you can handle these.

Step 5: Calculate employer tax contributions

As an employer, you are responsible for withholding and remitting all employee-specific payroll taxes on their behalf. However, you must also calculate and remit employer-specific federal, state, and local payroll taxes.

- FUTA: As of 2026, the FUTA tax rate is 6% with a $7,000 taxable wage base, but you can get a 5.4% tax credit if you pay your state unemployment insurance (SUTA) on time. This means you only pay 0.06%.

- FICA: This is easy to determine since your Social Security (6.2%) and Medicare (1.45%) tax rates match what your employee pays. Like your employee, you also stop paying the Social Security portion of FICA once they hit the taxable wage base for the year.

- SUTA: You’ll receive your SUTA rates from your respective state agencies. Most states base their rates on your unemployment history, so the fewer employees you have claiming unemployment benefits historically, the lower your unemployment rate. Some states also take your industry into account.

- State or local taxes: Research the employer tax requirements in each state where you have employees and remit these amounts accordingly.

Continuing the Mikhail Scotch example above, assume we’re in a low-risk industry—paper sales. Our FUTA rate is 6%, and our SUTA rate for Pennsylvania is 3.82%. Let’s figure out our portion of taxes for Mikhail below.

| 1. Social Security tax ($1,060 X 0.062) | $65.72 |

| 2. Medicare tax ($1,060 X 0.0145) | $15.37 |

| 3. FUTA tax ($1,060 X 0.06) | $63.60 |

| 4. SUTA tax ($1,290 X 0.0382) | $49.28* |

| Total employer taxes | $193.97 |

*Double-check what the employee’s state considers taxable income for SUTA purposes. Generally, it is the same as gross pay, without pre-tax deductions.

Step 6: Distribute paychecks

Once you’ve processed payroll, you must distribute everyone’s paychecks via the payment method they chose during onboarding. Remember to send positive pay information to your financial institution if you issue live checks.

Employees should also receive their pay on their scheduled payday. In some states, like California, you may incur waiting time penalties for every day of late pay. You must also present a paystub to the employee as proof of payment, even if they receive it electronically.

Although payroll processing times differ for each company, direct deposits generally take at least one to three days to reach employee bank accounts. While you can print and hand-deliver checks to your on-site staff, you must ensure you mail checks early enough to reach your off-site employees by payday.

Learn more about how long it takes to process payroll from start to finish:

Payroll software speeds up payment processing

Knowing how to do payroll yourself is great, but using payroll software can streamline processes. Plus, you save time, especially if it can print checks and send direct deposits to employees within the platform. Several payroll vendors even offer their own paycheck signing and delivery services.

Moreover, these solutions automatically produce pay stubs that employees can access 24/7 through online portals. QuickBooks Workforce, for example, has built-in pay stub and check printing features and even provides access to compatible check paper stock you can order online. To learn more, visit the website.

Step 7: File paperwork and remit payroll taxes

Keep tabs on how much you owe in payroll taxes for each employee. Depending on the tax, you must remit these payments to various agencies on different schedules. Usually, the schedule for filing payroll tax returns differs from when you remit payments. Check with your employee’s state treasury department for information on these schedules.

As for depositing federal payroll taxes, FIT and FICA taxes are due to the IRS semi-weekly or monthly, depending on your tax liability. FUTA deposits also depend on your tax liability, but generally occur only once a quarter or longer. You must submit all payments through the Department of the Treasury’s EFTPS.

In addition, you must submit tax returns at the appropriate time. Form 940 details your FUTA payments and is due annually on January 31 for the previous year’s data. Meanwhile, Form 941 shows your FIT and FICA payments. You’ll file these quarterly by the last day of the month following the end of each quarter.

Pro tip: Check out the IRS’ employment tax due dates page for more information on tax filing and deposit schedules. You may also want to speak with an accountant or tax advisor to ensure you meet all deposit and filing schedules for federal, state, and local payroll taxes.

Step 8: Store payroll records

The FLSA requires you to keep employee wage information for at least three years, while the IRS requires you to keep payroll tax records for at least four. Other payroll records have longer or shorter storage requirements, depending on state and local jurisdictions.

You’ll also need to keep payroll records for the year to send W-3 forms to the IRS and Social Security Administration (SSA) and W-2 and 1099-NEC forms to your workers. W-3 forms summarize the information on W-2 forms and are due to the IRS and the SSA on January 31. Similarly, W-2s and 1099-NECs are due to your employees and contractors on January 31.

Thorough payroll recordkeeping simplifies year-end payroll paperwork and minimizes compliance issues in case the IRS audits you. In fact, periodic payroll audits are a great way to improve your payroll process efficiency while proactively addressing issues before they become major problems.

Advantages of doing your own payroll

In some cases, calculating your own payroll is the most affordable and practical option. Here’s why.

Disadvantages of doing your own payroll

Running payroll by yourself can be time-consuming, prone to human error, and legally risky.

Running payroll by hand takes a lot of time, especially if you have more than one or two employees. Besides how long it takes to process paychecks, you also spend valuable time researching payroll laws and complying with tax deposit and filing schedules.

Payroll software simplifies the whole process and allows you to spend your time on more valuable tasks. Some solutions can even run payroll and issue direct deposits automatically, so you don’t have to worry about remembering your payroll schedule.

QuickBooks Payroll, for example, includes an Auto Payroll feature that processes payroll automatically for salaried and hourly employees who work the same hours each workday. This saves you time from manually completing each pay run yourself.

Processing payroll on your own also significantly increases the chances of errors compared to using software. You might enter the data incorrectly or make a mistake while calculating wage garnishments by hand.

You must also account for any updates each pay period, such as new state or federal income tax rates or increased employee withholding allowances. Such frequent changes also increase your chances of making mistakes.

However, most payroll software includes code to minimize errors. QuickBooks Payroll, for example, comes with pay warnings you can set up to alert you of missing payment details, leave request approval and accrual issues, and incomplete pay run tasks.

Legal risks

If you don’t check or fix any payroll errors, you expose yourself and your business to the consequences of these compliance issues whenever you process payroll. You may face an audit, penalty, or lawsuit for incorrect employee wages.

If any of these situations arise, the legal fees and penalties will typically far outweigh any money you would have spent on payroll software. In fact, many come with compliance monitoring or in-app HR support.

Providers like QuickBooks Payroll offer a tax accuracy guarantee that covers penalties arising from tax filing errors made by its representatives. It even has a premium option for its highest plan that pays up to $25,000 in tax penalties, regardless of who made the mistake. For HR advisory services, QuickBooks Payroll’s partnership with Mineral grants you access to HR professionals who can provide expert advice to ensure you comply with federal, state, and local laws.

Alternatives to doing payroll yourself

There are several different options that you can pursue if you no longer want to calculate your small business payroll on your own:

FAQs about manual payroll processing

DIY payroll saves money, but not time

Manual payroll might be your small business’s only option as you scour for investors, drum up funding, and funnel what little you have straight into your business operations. Completing payroll yourself may be your reality until your headcount and profit margin grow enough to warrant payroll software or services.

Until then, take advantage of our payroll resources below to better understand the process and perhaps make it just a little less tedious.