A credit card payment app lets you accept customer payments using Tap to Pay, a mobile card reader, payment links, invoices, or an online checkout. The best credit card payment app should work wherever sales happen: at a checkout counter, at an event, on a job site, via an invoice, or on a mobile device. The right app should make payments easy to accept without adding unnecessary hardware, setup time, or processing costs.

For this guide, I focused on merchant-side apps that are easy to use, support multiple payment methods, and fit common small business sales channels. Then, I compared each provider across pricing, payment methods, app reliability, integrations, and recent user feedback. I also considered how well each app fits real business needs, including general small business payments, ecommerce, custom online payments, social selling, and high-volume processing.

| Best for | Monthly fee | |

| Square | Overall credit card payment app | $0 |

| Helcim | Scalability | $0 |

| Shopify | Ecommerce | $5 |

| Stripe | Customizations and integrations | $0 |

| PayPal | Fast and convenient payments | $0 |

| Venmo | Selling on social media | $0 |

| Stax | Large-volume transactions | $99-$199 |

Credit card payment apps vs mobile card readers vs payment processors

A credit card payment app is the software a business uses to accept card payments from a phone, tablet, computer, invoice, payment link, or online checkout. In this guide, we are focusing on merchant-side apps that help businesses take payments from customers, not consumer payment apps used only to send money or pay at checkout.

| Term | What it means | Example |

| Credit card payment app | Software used to accept customer card payments from a phone, tablet, invoice, payment link, or online checkout. | Square POS, PayPal Zettle, Shopify POS, Stripe Dashboard |

| Mobile card reader | Hardware that connects to a payment app so a business can accept swipe, chip, or tap payments in person. | Square Reader, Shopify Tap & Chip Card Reader, PayPal card reader |

| Payment processor | The provider that authorizes card payments, moves funds, and charges processing fees. | Square, Stripe, Helcim, PayPal, Stax |

| Mobile wallet | A customer-side payment method used to pay with a phone or wearable device. | Apple Pay, Google Pay, Samsung Pay |

Best credit card payment apps compared

| Provider | Business type or need | In-person transaction fee | Card reader options | Funding speed | My score (out of 5) |

| Square | New and small businesses | 2.4%-2.6% + 15 cents | Square magstripe and contactless$0-$59 | Next day; instant for fee | 4.41 |

| Helcim | Growing businesses | Interchange plus 0.15% + 6 cents to 0.4% + 8 cents | Helcim 2-in-1 card reader$99 | Standard deposits | 4.35 |

| Shopify | Ecommerce sellers | 2.4% + 10 cents to 2.6% + 10 cents | Shopify 2-in1 card reader$49 | 3+ business days | 4.34 |

| Stripe | Custom online payments | 2.7% + 5 cents | Stripe Reader M2 3-in-1$59 | 7-14 days first payout; then 2 days | 4.26 |

| PayPal | Freelancers and occasional sellers | 2.29% + 9 cents | PayPal Point of Sale (formerly Zettle) 2-in-1 card reader$29-$79 | Minutes to PayPal; next day to bank | 4.25 |

| Venmo | Social sellers | 1.9% + 10 cents (Venmo app) | Not required | Instant transfer for fee | 4.24 |

| Stax | High-volume businesses | Interchange plus 8 cents | SwipeSimple 3-in-1 card reader | Next business day | 4.19 |

All of my recommended providers above support both iOS and Android devices. But if you’re looking for more specific options, check out our sections for:

What payment app fees look like in practice

Advertised processing rates only tell part of the story. Your actual cost depends on monthly card volume, average ticket size, sales channel, and whether transactions are tapped, dipped, keyed in, invoiced, or processed online.

Here is a simple way to estimate payment processing costs:

Estimated processing cost = percentage fee × monthly card volume + fixed transaction fee × number of transactions

For example, a business processing $10,000 per month across 200 in-person transactions with Square would pay about $290 in processing fees: $260 from the 2.6% percentage fee plus $30 from the 15-cent fixed fee.

| Scenario | What to compare | Likely takeaway |

| $10,000 in in-person sales | In-person processing rate, fixed transaction fee, and average ticket size | Flat-rate apps like Square are easy to predict and often work well for small businesses with mostly in-person sales. |

| $10,000 split between in-person and keyed payments | In-person fee plus keyed, invoice, or card-not-present fee | Keyed and card-not-present payments usually cost more, so businesses that take phone orders, send invoices, or accept remote payments should compare those rates separately. |

| $50,000 monthly card volume | Flat-rate pricing vs interchange-plus or subscription pricing | Interchange-plus providers like Helcim or subscription-based processors like Stax may become more cost-effective once volume is high enough to offset added setup, approval, or monthly plan costs. |

The cheapest credit card payment app is not always the one with the lowest advertised rate. A no-monthly-fee flat-rate app may be the better deal for a new or low-volume business, while a processor with interchange-plus or subscription pricing may save money for a growing business with higher card volume.

Square: Best overall credit card payment app

Star rating

4.41/5

Pricing

4.06/5

Mobile features

4.5/5

Support and reliability

4.38/5

User experience

4.38/5

Average user review scores

4.75/5

Pros

- All-in-one POS and payment system

- Highly rated mobile pos app

- Waived chargeback fees

- Large-business solutions

Cons

- Limited customer support hours

- Reports of frozen funds

- Account stability issues

Why I chose Square

Square is an all-in-one POS and payments platform with a built-in credit card payment app. The mobile app connects directly to Square’s processing service and integrates with its in-store POS and online store, so you can use the same system for card-present payments, invoices, and basic ecommerce.

You do not need a separate merchant account, which makes Square especially appealing for new or very small businesses that want to accept cards without a long underwriting process. In my testing, account signup was quick, and the guided setup inside the app made it easy to run first test transactions and configure basic payment settings within minutes.

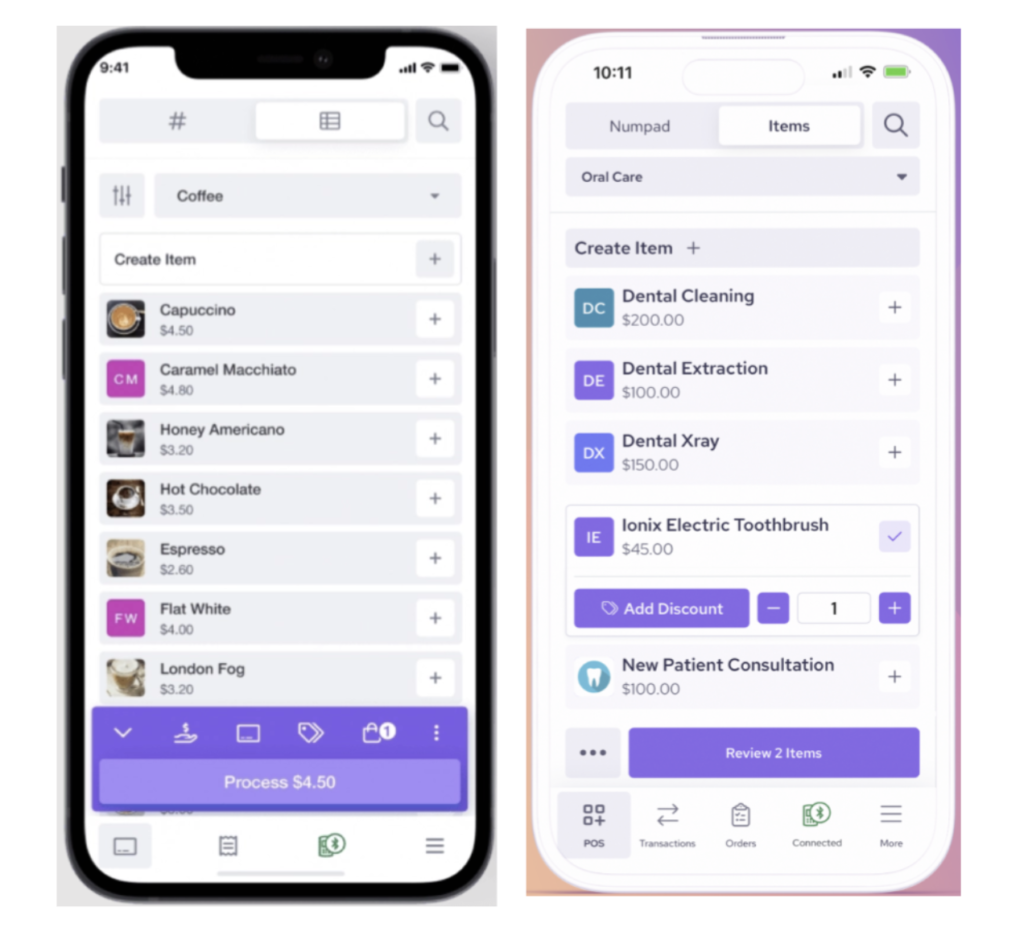

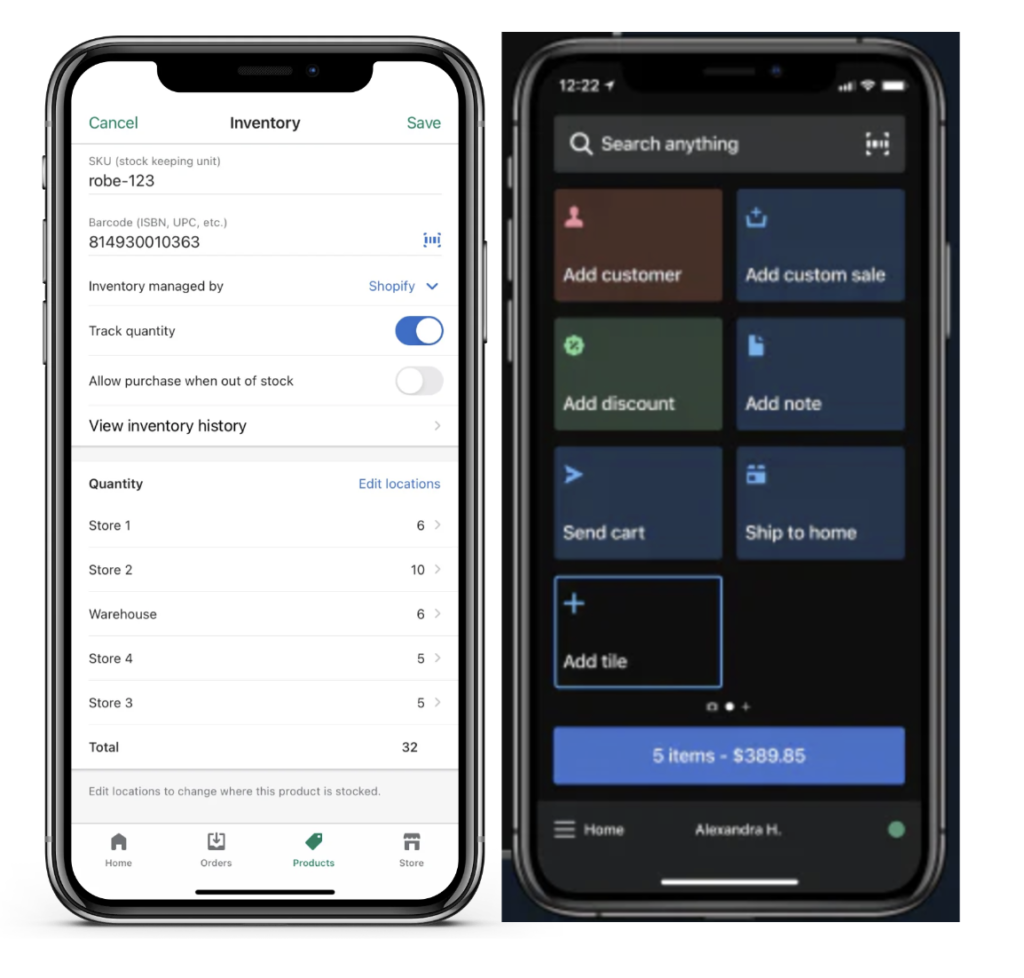

From a credit card payment app standpoint, Square scored highly in my rubric because it covers the core use cases most small businesses care about. The app supports tap, chip, and swipe payments with a compatible reader, and you can accept Tap to Pay directly on a phone. It also lets you key in card details, send payment links, create simple invoices, add items, track basic inventory, view real-time sales, and issue digital receipts without upgrading to a paid POS plan.

That breadth is what makes Square stand out from simpler payment apps. It is not just a way to collect card payments. It gives small businesses enough POS, reporting, inventory, and checkout tools to run early-stage sales from one account. User reviews support this experience, with many reviewers praising Square for its easy setup, smooth checkout flow, and ability to manage payments, bookings, inventory, and sales tracking in one place.

The tradeoff is flexibility and account control. Square’s credit card payment app only works with Square’s own processing, so you cannot plug it into another POS system or bring an outside merchant account to negotiate separate rates. Some users also report account stability issues, fund holds, and difficulty reaching timely customer support, which is worth considering if your business has higher-risk transactions, unusual sales patterns, or needs predictable access to funds.

I would not use Square if you already have a preferred merchant account, need custom-negotiated processing rates, or want a payment app that can sit on top of another POS or processor. But if you want an all-in-one provider that handles the app, POS tools, card readers, online payments, and processing in one place, Square is still the strongest starting point for most small businesses.

Brick-and-mortar shops, pop-ups, mobile service providers, and new businesses that want a free, all-in-one app to start taking in-person payments quickly.

Users consistently praise Square for its ease of use, quick setup, and ability to handle payments, inventory, and reporting in one app, but some report account stability issues, fund holds, and difficulty reaching timely customer support.

Average user ratings:

- 4.8 out of 5 stars in the Apple App Store

- 4.6 out of 5 stars in Google Play

“Square has been amazing for my business! It’s easy to use, reliable, and makes the whole checkout process smooth for both me and my clients. I love how professional it looks and it gives me everything I need in one place — from payments and bookings to tracking sales.” — Apple App Store reviewer

- Monthly account fee: $0-$149 (including POS software)

- Mobile app fee: $0

- Card-present fee: 2.4%-2.6% + 15 cents

- Card-not-present fee: 2.9%-3.3% + 30 cents

- American Express transactions: $0

- Volume discounts: By request for businesses with sales volume greater than $250,000/year

- Chargeback fee: Waived up to $250 per month

- Mobile card reader cost: $0-$59

- Application/set-up fee: $0

- Cancellation fee: $0

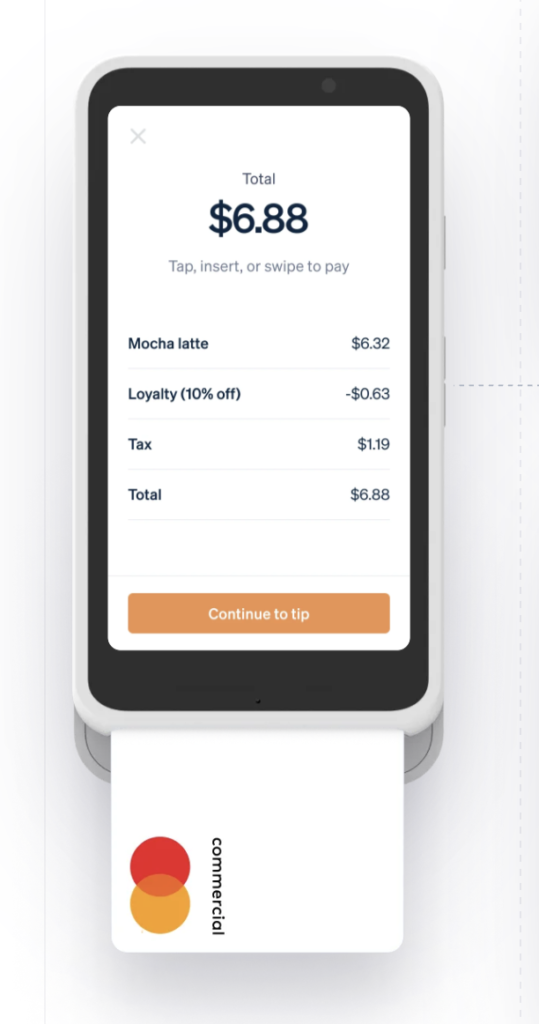

- Payment methods: Square’s mobile POS app provides a complete range of in-person payment processing methods, including hardware-free payments via manual entry, QR code scanning, tap-to-pay, and mobile wallet transactions.

- App compatibility: Square’s mobile POS app is exclusive to Square users but has one of the highest user ratings for both iOS and Android users.

- Mobile card readers: Square offers the first free magstripe card reader for all Square merchants. The Square EMV and contactless card reader allows for dipped and tapped credit card payments.

- Scalability: Square offers custom pricing for businesses that process more than $250,000 per year. It also offers customizable and scalable solutions for enterprise-level businesses, including multiple account access and a wide range of business integrations.

Related: Square 2026 Overview

Helcim: Best for scalability

Star rating

4.35/5

Pricing

4.5/5

Mobile features

4.5/5

Support and reliability

4.06/5

User experience

4.69/5

Average user review scores

3.65/5

Pros

- Automated volume discounts

- No additional approval for surcharging

- Interchange-plus rates

Cons

- Low mobile app rating for Android users

- Additional cost for Amex transactions

- Expensive mobile card reader

Why I chose Helcim

Helcim is a strong choice for businesses that want the stability and lower long-term costs of a full merchant account. While Square emphasizes simplicity and Stripe leans into online-first infrastructure, Helcim is built for growing small and midsize businesses that want transparent pricing, account stability, and more control over processing costs.

Its credit card payment app is part of a broader integrated platform that includes inventory tools, a CRM, invoicing, payment links, ACH payments, and a secure card vault with no monthly software fee. That gives Helcim more back-office depth than many free mobile payment apps, especially for businesses that sell through more than one payment channel.

Helcim scored well in my rubric because its mobile POS app ties directly into the merchant account and unlocks more advanced features than most free apps offer. You can accept chip and tap payments, store cards securely for later use, create detailed customer profiles, and run itemized transactions from a centralized catalog.

The standout benefit with Helcim is its interchange-plus, volume-based pricing model. As your sales increase, your rates adjust automatically, so you do not need to renegotiate or upgrade plans the way you would with many flat-rate providers. The platform also includes automated surcharging for businesses that choose to offset card fees, giving it more built-in cost-control tools than many competitors.

The tradeoff is onboarding. Unlike Square, where you can sign up and start accepting payments in minutes, Helcim requires a full merchant account approval process. That means stricter requirements and a longer wait before you can process live transactions. The upside is that you can still explore the app while waiting for approval, and once approved, you gain access to more advanced features and lower long-term rates than most aggregator-based providers offer.

I would not use Helcim if you need to start taking card payments today, process very low monthly volume, or want the simplest possible app with the least setup. It is also not the best fit for sellers that only need occasional mobile payments and do not want to go through merchant account underwriting. Helcim is a better fit for growing businesses that care about transparent pricing, account stability, invoicing, customer management, and lower long-term processing costs.

Retailers, professional services, and B2B companies that expect volume to increase and prefer transparent, interchange-plus pricing.

Users appreciate Helcim for its transparent pricing and ability to manage payments, invoicing, and inventory in one app, but many report app crashes, card reader connectivity issues, and slow or inconsistent customer support.

Average user ratings:

- 4.1 out of 5 stars in the Apple App Store

- 3.1 out of 5 stars in Google Play

“The best point of sale equipment I have used yet, the machine works every time with zero issues. I connect mine to my cellphone via Bluetooth and works fantastic!” — Apple App Store reviewer

- Monthly account fee: $0

- Mobile app fee: $0

- Card-present fee: Interchange plus 0.15% + $0.06 to 0.4% + $0.08

- Card-not-present fee: Interchange plus 0.15% + $0.15 to 0.50% + $0.25

- American Express transactions: + 0.10% + $0.10

- Volume discounts: Automated

- Chargeback fee: $15 refundable

- Mobile card reader cost: $99

- Application/setup fee: $0

- Cancellation fee: $0

- Payment methods: Helcim’s mobile POS app offers tap, chip, and PIN debit in-person credit card payment methods with the help of Helcim’s mobile card reader. Hardware-free payment options include manual entry, QR code, mobile wallet, and tap to pay.

- Mobile card readers: Helcim’s mobile POS app works with the Helcim card reader that collects payments via EMV and contactless, plus a PIN debit option for debit card payments.

- App compatibility: The Helcim mobile POS app is exclusive to Helcim merchants and is available on iOS and Android smart devices. The app is getting better reviews from Apple than Android users.

- Scalability: Helcim’s pricing structure provides automated discounts for growing sales. Developer tools are available for custom branding, white-label embedded payment gateway, multi-currency, and multi-user functionalities.

Shopify: Best for ecommerce

Star rating

4.34/5

Pricing

3.44/5

Mobile features

4.75/5

Support and reliability

4.38/5

User experience

4.69/5

Average user review scores

4.35/5

Pros

- Full-suite ecommerce solution

- Omnichannel features

- Accepts PayPal payments

Cons

- Advanced tools require an ecommerce subscription

- Reports of frozen funds

- Low app ratings from Android users

Why I chose Shopify

Shopify is the strongest option on this list for businesses that operate primarily online but also need a reliable credit card payment app for in-person sales. While Square is built around brick-and-mortar simplicity and Stripe focuses on online payments with developer tools, Shopify is the better fit when ecommerce is the center of the business.

As an ecommerce expert, I consistently recommend Shopify as one of the best ecommerce platforms because its ecosystem goes beyond payment acceptance. It includes an online store builder, checkout tools, marketing features, fulfillment support, marketplace integrations, and a POS system that runs on phones and tablets. For retailers that sell online, in person, and across multiple channels, that connected setup is the main reason to choose Shopify over a simpler payment app.

From a credit card payment app standpoint, Shopify scored well in my rubric because its POS app is tightly integrated with Shopify Payments and the broader ecommerce platform. Card-present sales, whether tapped, dipped, or manually entered, flow into the same dashboard used to manage online orders, abandoned carts, shipping, customer profiles, and product inventory.

Compared with providers like PayPal or SumUp, which are better suited for simple in-person or occasional transactions, Shopify offers deeper inventory management, cleaner product syncing, and more complete customer data. That makes it one of the best choices for ecommerce brands that are adding pop-ups, markets, retail events, or permanent in-person selling.

User reviews support this strength, with many Shopify POS users praising its online store integration, inventory tools, and organized app experience. However, reviewers also report card reader connectivity issues, payout holds, and limited customer support during account problems. Those complaints matter because Shopify is strongest when your sales channels are connected, but payment or account delays can disrupt both online and in-person operations.

I would not use Shopify mainly as a standalone credit card payment app if you do not already sell online or plan to build an ecommerce store. It can be more setup than a small service business, mobile seller, or occasional vendor needs. But if your online store is the source of truth for products, inventory, orders, and customer data, Shopify is one of the best payment apps for bringing in-person sales into the same system.

Ecommerce brands, omnichannel retailers, and online-first businesses that want in-person payments, online orders, inventory, and customer data to live in one unified system.

Related: Best 8 Square Alternatives & Competitors.

Users like Shopify POS for its seamless integration with online stores and strong inventory management tools, but many report issues with card reader connectivity, payout holds, and limited customer support during account problems.

Average user ratings:

- 4.5 out of 5 stars in the Apple App Store

- 4 out of 5 stars in Google Play

“What a great app! It’s a little slow BUT so convenient and it’s very well organized.” — Google Play reviewer

Shopify’s mobile POS Lite is free with any of Shopify’s ecommerce plans. Large businesses can upgrade to the paid POS plan to access advanced features.

- Monthly account fee:

- POS only: $5

- Ecommerce + POS plan: $39-$399 + $0-$89

- Mobile app fee: $0

- Card-present fee: 2.4% + 10 cents to 2.6% + 10 cents

- Card-not-present fee: 2.5% + 30 cents to 2.9% + 30 cents

- American Express transactions: $0

- Volume discounts: Via paid plans + custom plans for enterprise-level businesses

- Chargeback fee: $15 refundable

- Mobile card reader cost: $49

- Application/set-up fee: $0

- Cancellation fee: $0

- Payment methods: Shopify’s POS app supports a full suite of in-person payment methods, including hardware-free payments such as QR codes, mobile wallet, and tap to pay.

- App compatibility: Shopify is an exclusive mobile POS app that’s compatible with both Apple and Android users. However, the iOS app is getting significantly better reviews from real-life users than the Android version.

- Mobile card readers: Shopify provides an affordable proprietary mobile card reader that can process tap and chip payments as well as mobile wallet transactions. Swipe transactions are possible with the Shopify standalone terminal.

- Scalability: Shopify offers an enterprise program that supports high-level customization for B2C, B2B, and large retail businesses. The developer tools can be used to create custom branding, multi-user profiles, and other POS functions that will also be reflected in the mobile app.

Stripe: Best for customizations and integrations

Star rating

4.31/5

Pricing

3.13/5

Mobile features

4.5/5

Support and reliability

4.69/5

User experience

4.69/5

Average user review scores

4.6/5

Pros

- Integrates with other payment platforms

- Advanced customization features

- Custom pricing for large businesses

- Industry-leading API and developer documentation

Cons

- Add-on fees for invoicing and recurring billing

- Limited in-person payments for native mobile app

- Requires third party or custom developer for card-reader payments

Why I chose Stripe

Stripe is a strong pick for businesses that treat payments as part of a broader online operation rather than just a simple mobile card reader setup. Compared with Square, which is built around plug-and-play POS tools, Stripe is better suited to businesses that sell across websites, apps, marketplaces, subscriptions, or multiple brands and want one payment platform behind those channels.

Stripe scored well in my rubric for flexibility and scalability. Used with Stripe Terminal and compatible readers, Stripe lets businesses accept chip and contactless cards in person, then sync those payments with online sales data. It also supports manual card entry and can be built into custom payment flows through Stripe’s APIs.

Stripe gives businesses more room to customize checkout, connect payments to internal systems, support recurring billing, manage online and in-person payments together, and expand across countries and currencies. If your business has a developer, uses custom software, or needs payments embedded into an app or platform, Stripe is usually stronger than a plug-and-play provider like Square, PayPal, or SumUp.

However, Stripe’s in-person payment tools are not as turnkey as Square’s mobile POS, and setup can feel more technical if you are not already using Stripe online. In my evaluation, Stripe made the most sense when it was part of a larger payment infrastructure, not when used as a standalone credit card payment app for a small shop or mobile seller.

I would not use Stripe if you mainly need a simple phone-based POS app, fast in-person setup, built-in retail workflows, or the easiest way to start taking card payments today. It is also not the best fit if you do not have the technical resources to configure and maintain a more flexible payments setup.

Software companies, subscription businesses, marketplaces, and multichannel brands that need a customizable payment stack for websites, apps, and in-person transactions.

Users consistently praise Stripe Dashboard for its clean interface, real-time payment tracking, and strong reporting tools, but some report issues with account holds, payout delays, and limited support when problems arise.

Average user ratings:

- 4.7 out of 5 stars in the Apple App Store

- 4.5 out of 5 stars in Google Play

“The process to set up my account was pretty easy and connecting to my bank. I love receiving the notifications so I can track payments received and the low processing fee. However, I would like for them to allow more fields to obtain additional information from customers like a note section, phone number, and a field for additional information. I had a couple of tickets purchased on behalf of others but nowhere to put their name.” — Google Play reviewer

- Monthly account fee: $0

- Mobile app fee: From $0 (for custom-designed apps); third-party mobile payment apps will charge anywhere from 1%-1.5% per transaction.

- Card-present: 2.7% + 5 cents

- Keyed-in: 3.4% + 30 cents

- Touchless: 2.9% + 30 cents

- Tap-to-pay on mobile: +10 cents per authorization

- Volume discounts: Custom interchange-plus pricing for larger businesses

- Chargeback fee: $15

- Mobile card reader cost: $59

- Application/set-up fee: $0

- Cancellation fee: $0

- Payment methods: Stripe’s mobile dashboard app can process hardware-free payments such as manual entry, QR code, and tap to pay. Users can also accept swipe, chip, and tap credit cards if they use a third-party or custom-developed mobile payment app.

- App compatibility: The Stripe mobile app is compatible with iOS and Android devices and is exclusive to Stripe users.

- Mobile card readers: Stripe offers a 3-in-1 mobile credit card reader that can process magstripe, EMV, and contactless payments, including mobile wallet transactions.

- Scalability: Stripe’s well-documented APIs and advanced developer resources power its potential for growing with a business. Businesses can customize their mobile payments app, and Stripe provides a list of developer solutions (e.g., Ciklum and Happy Cog), enterprise POS and PMS integrations (e.g., Microsoft Dynamics and Adobe Commerce), and Stripe Professional Services.

PayPal: Best for fast and convenient payments

Star rating

4.25/5

Pricing

4.06/5

Mobile features

4.25/5

Support and reliability

4.06/5

User experience

4.69/5

Average user review scores

4.3/5

Pros

- Ease sign up and set up

- Free POS

- Instant access to funds via PayPal Balance

- Wide range of payment options

Cons

- Complex pricing

- Can be pricey with add-on tools

- Reports of frozen funds

Why I chose PayPal

PayPal is one of the most recognizable names in digital payments, which makes it a strong choice for businesses that want fast setup, broad customer familiarity, and flexible ways to accept payments.

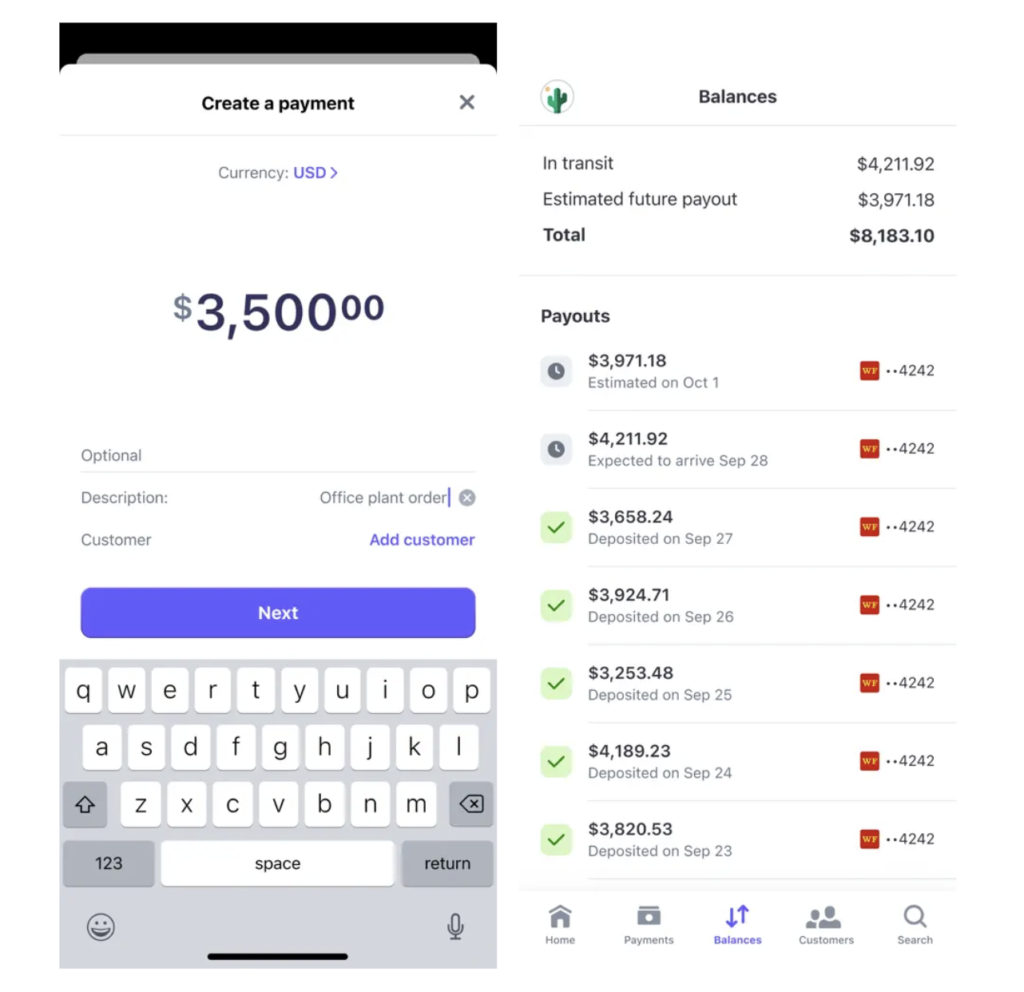

PayPal’s biggest advantage is convenience. From a credit card payment app standpoint, PayPal scored well in my rubric because it supports common small business payment needs without much setup. You can accept in-person payments with a compatible card reader, take contactless payments, send invoices, and offer customers a checkout option they likely already know. This makes PayPal especially useful for low-volume sellers, service providers, and businesses that process occasional international or tourist payments.

The tradeoff is that PayPal is not as strong as Square or Shopify for full POS operations. It can handle payments well, but it is not the best choice if you need advanced inventory tools, deep retail reporting, employee management, or a more complete in-store checkout system. User reviews reflect this split: many customers like PayPal Business for convenience, invoicing, mobile payment tracking, and easy account access, but others report account limitations, fund holds, and difficulty reaching reliable support when issues come up.

I would not use PayPal as the main credit card payment app for an inventory-heavy retail store, a growing brick-and-mortar business, or a seller that needs stronger POS controls. But for freelancers, casual sellers, mobile service providers, and small businesses that want quick access to familiar payment tools, PayPal is still one of the easiest apps to start with.

Freelancers, small online sellers, and businesses that want fast setup and familiar PayPal checkout options.

Users appreciate PayPal Business for its convenience in sending invoices, tracking sales, and managing payments on the go, but many report issues with account limitations, fund holds, and difficulty reaching reliable customer support when problems arise.

Average user ratings:

- 4.2 out of 5 stars in the Apple App Store

- 4.4 out of 5 stars in Google Play

“Very simplified for my vendor marketing registries.” — Google Play reviewer

- Monthly fee: $0

- In-person transaction fee: 2.29% + 9 cents

- Online transaction fee: 2.99% + 49 cents

- Keyed-in transaction fee: 3.49% + 9 cents

- Invoicing: 3.49% + 9 cents

- QR code payments: 2.29% + 9 cents

- Venmo payments: 3.49% + 49 cents

- Hardware: $0-$269

- Payment methods: PayPal’s mobile payment app offers card and PayPal payment methods. It also supports QR and manual entry payments, as well as invoicing and subscription management tools. PayPal can also accept foreign credit card transactions.

- Mobile card readers: PayPal Point of Sale (formerly Zettle) comes with an EMV chip and contactless reader. It’s also equipped with a PIN pad for debit card transactions. The card reader connects via Bluetooth to a smartphone, tablet, or iPad with a PayPal business app.

- App compatibility: The PayPal business app is exclusive to PayPal merchants and is available on iOS and Android. The app is getting decent review scores, although recent feedback is better from Apple users.

- Scalability: PayPal’s primary pricing and payment tools are ideal for small businesses. However, PayPal also offers enterprise payment services where you can add custom payment features and branding to the payment app, plus custom rates for large-volume transactions.

Venmo: Best for businesses selling on social media

Star rating

4.24/5

Pricing

4.06/5

Mobile features

4.25/5

Support and reliability

4.06/5

User experience

4.69/5

Average user review scores

4.25/5

Pros

- Social media integrations

- Native marketing tools

- Tap to pay for non-Venmo customers

- Easy business account sign-up

Cons

- Limited payment options

- No volume discounts

- Limited seller protection

Why I chose Venmo

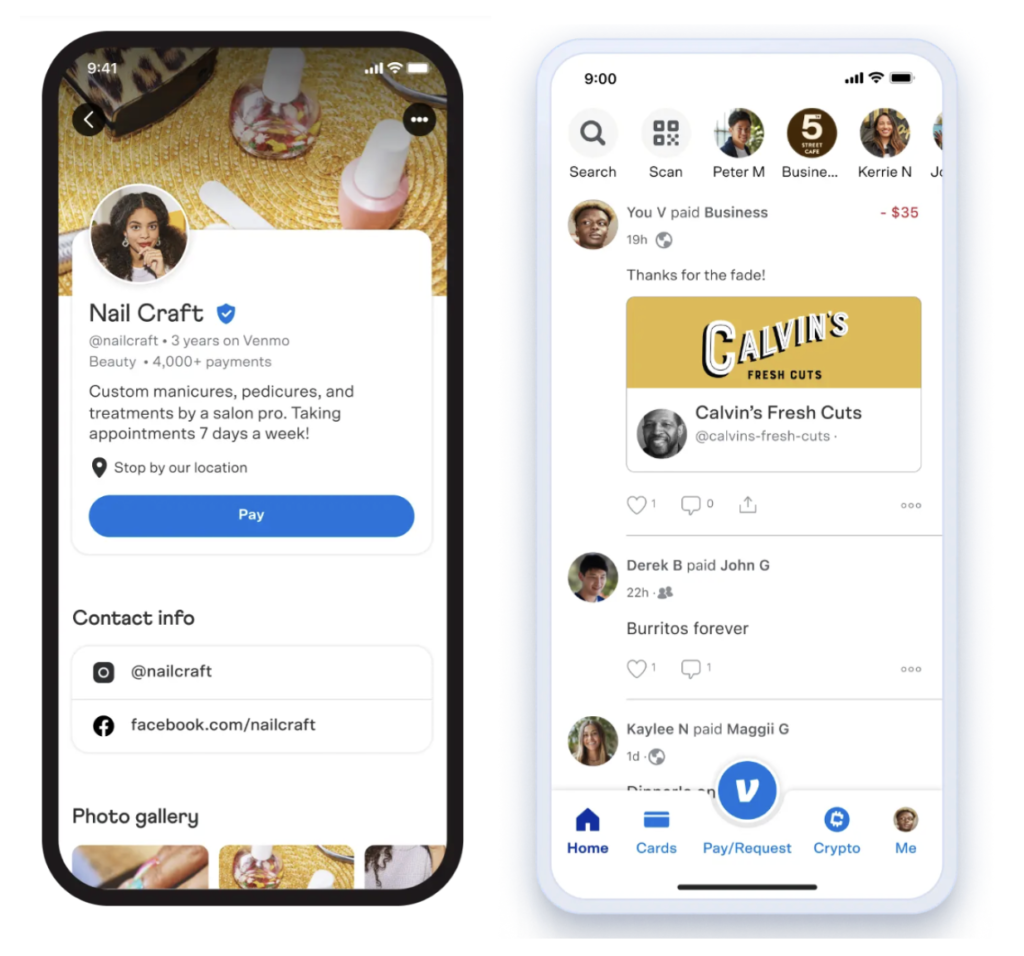

Venmo is a peer-to-peer payment app popular for its social media integration. It recently launched a business profile feature that allows individuals to create a separate account for processing business transactions.

As it is owned by PayPal, Venmo supports direct PayPal integration so customers can use their PayPal account to pay for their products and services via Venmo. There are no monthly fees for using the service, and Venmo-to-Venmo transaction rates are considerably lower than those of other in-app payments, including PayPal.

Unlike other providers in this list, Venmo is not compatible with mobile credit card readers, so Venmo merchants can only accept payments from Venmo individual users. However, with the latest addition of the tap-to-pay function, it’s now possible to accept contactless payments from credit cards and other mobile wallets. This makes it possible to actually perform in-person transactions via Venmo with one of the lowest flat transaction rates in the market.

User reviews reinforce Venmo’s main appeal: it is easy, familiar, and fast. However, complaints about account freezes, payment holds, support issues, and the social-style feed make it a weaker fit as a primary business payment tool.

I would not use Venmo for a retail store, restaurant, or growing business that needs inventory, staff permissions, itemized checkout, reporting, or dependable POS workflows. It works better as a secondary payment option for solo sellers, microbusinesses, market vendors, and social sellers.

Microbusinesses and solo sellers who take payments through social platforms and want a familiar, peer-to-peer style experience for customers.

Users consistently praise Venmo for its ease of sending and splitting payments, along with its familiar, social-style interface. However, some report issues with account freezes, payment holds, and slow or unhelpful customer support during disputes.

Average user ratings:

- 4.9 out of 5 stars in the Apple App Store

- 3.5 out of 5 stars in Google Play

“‘I found Venmo is very easy to use. I like that the transactions are instant even when coming from my bank account. The only thing I don’t like is that I have to see all of the receivers’ transactions with others. I only care about mine. Theirs is none of my business. Otherwise it’s good.” — Google Play reviewer

- Monthly fee: $0

- Setup fee: $0

- In-person:

- Through Venmo app: 1.9% + 10 cents

- Tap to pay: 2.29% + 9 cents

- At POS: 3.49% + 49 cents

- Online checkout: 3.49% + 49 cents

- Instant transfer: 1.75%

- Payment methods: Venmo can accept payments from PayPal and other Venmo apps, including card payments and QR codes. And with the tap-to-pay feature, it can now process payments from other mobile wallets and EMV chip-enabled cards.

- App compatibility: The Venmo payment processor is exclusive to Venmo business accounts. It’s compatible with both iOS and Android smartphones, tablets, and iPads, although the app is performing so much better than its Android counterpart, according to real-life user reviews.

- Mobile card readers: Venmo does not require any mobile credit card reader to function. This essentially limits Venmo’s payment processing capability to contactless transactions, but the fees are significantly lower than other in-person and contactless flat rates.

- Scalability: Venmo is primarily for low-volume businesses like solo professionals and home-based retailers. Larger businesses should consider PayPal Enterprise, where you can customize mobile app features, including payment method options to include Venmo.

Stax: Best for large-volume businesses

Star rating

4.19/5

Pricing

4.38/5

Mobile features

4.75/5

Support and reliability

4.38/5

User experience

4.38/5

Average user review scores

2.4/5

Pros

- Wholesale payment processing rates

- Wide range of enterprise-level customizations

- Robust reporting and analytics

Cons

- Poor mobile app user ratings

- Limited mobile card reader options

- Reports of crashes and connectivity problems

Why I chose Stax

Stax is a traditional merchant account provider with subscription-style processing, making it a better fit for established businesses than for new or low-volume sellers. Like Helcim, Stax requires a more involved merchant account approval process, but the trade-off is access to a more comprehensive payment platform built for higher-volume businesses.

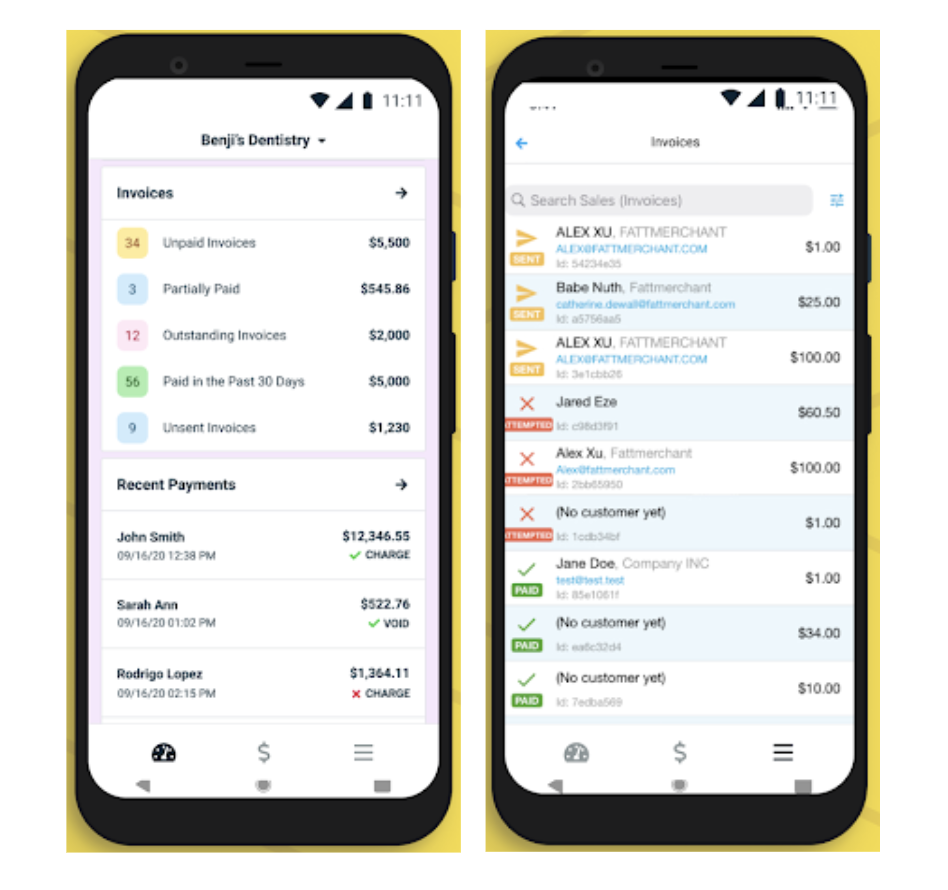

Stax Pay supports mobile payments, invoicing, reporting, and payment management from one system. I like that Stax can scale beyond simple payment acceptance as a business grows, with options such as Stax Bill for subscription management and Stax Processing for more customized payment setups.

The main reason to choose Stax is pricing structure. Instead of relying only on flat-rate processing, Stax uses subscription-style pricing that can become more cost-effective for businesses with enough monthly card volume to offset the membership fee.

The tradeoff is app reliability. User reviews praise Stax Pay for managing payments, invoices, and reporting in one place, but many also mention login issues, app crashes, and card reader connectivity problems. That makes Stax harder to recommend as a plug-and-play mobile payment app, especially for businesses that depend heavily on daily in-person transactions.

I would not use Stax if you are a new business, process low monthly volume, or need the simplest mobile payment app for fast setup. It is better for established businesses that can benefit from subscription-style pricing and are willing to go through a more traditional merchant account process.

Clinics, multi-location service providers, and mature retailers that process large volumes and can benefit from subscription-style or blended pricing.

Users like Stax Pay’s ability to manage payments, invoicing, and reporting in one place, but many report frequent login issues, app crashes, and unreliable card reader connectivity that disrupt daily use.

Average user ratings:

- 2.1 out of 5 stars in the Apple App Store

- 2.6 out of 5 stars in Google Play

“Love the way the app is seamless when taking a payment. Perfect app for business owners.” — Apple Store reviewer

- Monthly account fee: $99-$199

- Mobile app fee: $0

- Card-present fee: Interchange plus $0.08

- Card-not-present fee: Interchange plus $0.18

- American Express transactions: $0

- Volume discounts: Volume-based subscription plan

- Chargeback fee: $25

- Mobile card reader cost: Contact Stax for pricing

- Application/set-up fee: $0

- Cancellation fee: $0

- Payment methods: The Stax Pay mobile app can process a complete range of credit card payment methods. This includes hardware-free payments such as manual entry, QR code scanning, digital wallet payments, card scanning, and tap to pay.

- App compatibility: Stax Pay mobile app is exclusive to Stax merchants. The app can be upgraded to a more customized solution for larger businesses.

- Mobile card readers: Stax Pay is used in conjunction with the SwipeSimple B250 mobile card reader, which supports contactless and mobile wallet payments.

- Scalability: Stax can be customized and upgraded to support a wide range of businesses. For larger businesses, Stax offers more advanced plans that support developer tools, white-label custom branding, and multiple employee profiles.

How to select the right credit card payment app for your business

After deciding on the features that are non-negotiable for your business, follow the steps below. They mirror how product reviewers and consultants often evaluate payment apps for real businesses.

Step 1: Map how and where you accept payments

Start by listing your current and planned sales channels. Note whether you accept payments in a physical store, at events, in the field, online, or over the phone. Also, record where you might want to expand, such as adding pop-up markets or mobile service calls.

This will tell you whether you need mobile readers, tap-to-phone capability, full POS support, or tight ecommerce integrations, and it ensures you do not choose an app that only covers a portion of your payments.

Step 2: Estimate your monthly processing volume and costs

Processing fees are one of the largest ongoing costs for businesses that accept cards, so compare total cost, not just the advertised rate. Review each provider’s in-person, online, and keyed-in transaction fees, then estimate your monthly cost based on your sales volume and average ticket size.

Also check for monthly software fees, chargeback fees, hardware costs, instant transfer fees, and paid add-ons for tools such as invoicing, virtual terminals, or recurring billing. If your volume is growing, compare flat-rate pricing against interchange-plus or subscription pricing to see when a lower markup may offset monthly fees.

Related:

Step 3: Shortlist providers that match your channels and devices

Once you know how you sell, remove any providers that do not support your main payment methods, devices, or sales channels. A good credit card payment app should work with the phones, tablets, card readers, POS hardware, and ecommerce tools your business already uses or plans to use.

Then look at workflow fit. Check whether the app supports invoicing, stored cards, recurring billing, customer profiles, item catalogs, inventory tracking, automated surcharging where allowed, and integrations with your POS, ecommerce platform, accounting software, or CRM. If you have advanced needs, look for APIs or developer tools so you can build custom workflows without replacing the system later.

By the end of this step, you should have a short list of realistic candidates that fit both your sales setup and your budget.

Step 4: Compare fees, contracts, and payout times

Once you have a shortlist, compare the total costs side by side. Look at in-person, online, and keyed-in rates, but also scrutinize for chargeback fees, monthly minimums, and paid add-ons for features such as invoicing or virtual terminals.

Next, check whether the provider requires a long-term contract or early termination fees. Finally, confirm the standard payout schedule so you know when funds will reach your bank account and whether same-day deposits are available if you need faster access to cash.

Step 5: Test the app, reader, and support experience

Download the apps from your shortlist and, if possible, test them with real or demo accounts. Pay attention to how long setup takes, how intuitive the interface is, and whether the card reader connects quickly and stays connected during multiple transactions.

Contact customer support with a simple question and note how fast and how clearly they respond. Ask practical questions such as how long funds are held during reviews, what can trigger account holds or frozen payouts, whether offline processing is supported, and whether there are limits on high-value or keyed-in transactions. These details often matter more in day-to-day use than a small difference in the posted rate.

Step 6: Review security, dispute handling, and account-hold policies

Before you make a final decision, review each provider’s security documentation and policies for chargebacks and account reviews. Confirm that the provider meets Level 1 PCI DSS requirements, uses tokenization and encryption, and offers clear tools for tracking disputes.

Ask how merchants are notified about chargebacks, what support is available during investigations, and how long funds may be held if there is suspected fraud. A provider that is clear and specific on these topics usually delivers a smoother experience when issues arise.

How apps for credit card payments help your business

The primary benefit of credit card apps is mobility. Being able to accept payments anywhere and anytime gives businesses more opportunities to create a sale. Other benefits of credit card payment apps include:

- Lower transaction fees: Accepting payments in person is cheaper than remote transactions.

- Affordable investment cost: Most payment apps are free, and you only need to invest in a mobile credit card reader ($30 to $100) to start accepting payments.

- Multichannel functionality: A mobile credit card payment terminal can be programmed as an additional sales channel for store-based POS.

- Compatibility with multiple payment processors: Businesses will be able to continue using the same payment app, so there is no operational downtime.

- Ability to scale: Most credit card payment apps can be easily programmed with custom features to match a growing business’ needs.

- Additional layer of security from smartphones: Smart devices are equipped with native authentication tools, including biometrics, that help in securing payments.

Emerging trends in credit card payment apps

Payment apps respond to consumer preferences and trends, so they continue to change quickly. The following trends have a direct impact on how you accept payments over the next few years.

Tap-to-phone adoption

Tap-to-phone technology is moving from pilot programs into mainstream use, especially among smaller merchants. Visa reports that nearly 30% of Tap to Phone sellers are new small businesses, which shows how strongly micro and small merchants are embracing the ability to accept contactless payments using only an NFC-enabled smartphone.

A recent guide from the US Chamber of Commerce also highlights tap to pay and smartphone acceptance as key tools for small businesses that want low-cost ways to take contactless payments on the go.

For very small businesses or field-service operations, tap-to-phone can be enough to handle everyday card payments without buying separate terminals. This reduces hardware costs, simplifies setup for new staff, and makes it easier for mobile teams to take payments immediately wherever they meet customers.

Unified payment workflows

Providers are also investing in unified payment platforms that manage in-store, online, and mobile transactions in one system. Deloitte describes unified commerce as the next step beyond omnichannel, where front-end and back-end systems are connected on a single platform so retailers can see and manage all sales channels together rather than in separate tools.

Industry commentary from firms such as Forbes Tech Council emphasizes that unified payment orchestration acts as the “glue” that links online, in-store, mobile, and even IoT (Internet of Things) transactions into one intelligent system.

For small and midsize businesses, this shift shows up as payment apps that combine card-present checkout, invoicing, pay-by-link, QR-code payments, and stored cards in one dashboard instead of forcing you to juggle multiple providers.

Instead of using one system for the store, another for invoices, and a third for payment links, providers are building dashboards that manage all payment activity in one place.

Related also:

- Total Commerce for Small Retailers: A Practical Guide

- Payment Orchestration: A Small Business Guide

Smarter fraud and dispute tools

Fraud and chargebacks are becoming more complex, and that is pushing payment providers to roll out smarter tools. The Federal Trade Commission reported that consumers lost $12.5 billion to fraud in 2024, and KPMG notes that AI-driven systems are increasingly being used by financial institutions to strengthen payment security.

In response, many payment apps now promote AI-powered fraud scoring, real-time alerts, and guided chargeback workflows as core features, which is especially important if you process higher-ticket or card-not-present transactions.

If your business handles higher-ticket transactions or a large share of card-not-present payments, these tools can be a significant advantage when comparing payment apps.

FAQs

Yes, most payment processors provide a free mobile POS or payment app. These payment apps are compatible with tablets and smartphones and can be connected to a mobile credit card reader that can process swipe, chip, and tap payments.

Most credit card payment apps are free to use unless they come from a third-party app developer. The only monthly fees involved are the costs to process transactions.

The best credit card payment app is one that provides payment methods and features that match your business needs. Also, consider your business sales volume and choose a payment processor with a free payment app that can offer you the most savings.

Many small businesses look for an app that works right away without long approval times. Options like Square and Venmo are popular because you can sign up, verify your identity, and start taking payments within minutes.

These apps include basic tools such as tap-to-pay, invoicing, and payment links, which makes them easy for new businesses or seasonal sellers to adopt without extra hardware or contracts.

Yes. Most modern payment apps offer hardware-free options such as tap-to-phone, QR-code checkout, payment links, or mobile invoicing. These tools let you accept payments even if you do not want to invest in a reader or if you need a backup method when hardware is unavailable.

However, if you regularly take in-person payments, a reader can speed up checkout and reduce manual entry.

Reputable payment apps follow Level 1 PCI DSS standards and use tokenization and encryption to protect card data. Many also include fraud-monitoring tools and built-in authentication through your smartphone’s biometrics.

For added peace of mind, review each provider’s policies on chargebacks, account holds, and dispute management so you know what support is available if an issue arises.