Finding a reliable high risk merchant account is critical for businesses that face stricter underwriting, higher fees, or frequent account declines. High risk classification can stem from industry type, business model, chargeback history, or regulatory requirements. To help you identify the best fit, we evaluated leading high risk merchant account providers based on pricing, features, reliability, and approval flexibility.

The table below highlights the top options and the types of businesses each provider is best suited for.

| PaymentCloud | Best overall high risk merchant account with flexible underwriting | Healthcare services, real estate, online coaching, subscription ecommerce, high-ticket services, MATCH-listed merchants |

| Host Merchant Services | Best for transparent pricing and polished user experience | Professional services, growing ecommerce brands, B2B merchants, subscription businesses with moderate risk |

| Easy Pay Direct | Best for high risk SaaS and subscription-based businesses | SaaS platforms, digital products, online education, coaching programs, nutraceutical subscriptions |

| Durango Merchant Services | Best for hard-to-place and international high risk merchants | Adult content, auction houses, travel agencies, forex services, international ecommerce businesses |

| SoarPay | Best mid-market high risk specialist | CBD brands, firearms and accessories, nutraceuticals, ticketing services, travel merchants |

| PayKings | Best for businesses with high or rising chargeback ratios | Subscription services, online marketplaces, continuity programs, digital goods sellers with frequent disputes |

| Flowhub Pay | Best for cannabis payment processing | Licensed cannabis dispensaries, medical marijuana retailers, recreational cannabis stores |

| Payline Data | Best for merchants transitioning out of high risk | B2B service providers, professional services, ecommerce businesses with improving chargeback history |

Understanding high risk merchants

Businesses can be classified as high risk for different reasons, including the industry they operate in, how they process payments, or their historical transaction behavior. Understanding why a business is considered high risk helps narrow down which high risk merchant account providers are the best fit before comparing specific services.

Best high risk merchant accounts compared

| Provider | Our Rating (Out of 5) | Monthly Account Fee | Works with MATCH List* | High Risk Account Approval Rate | Approval Processing Time |

| PaymentCloud | 4.59 | From $10 | Yes | ~98% | ~48 hours |

| Host Merchant Services | 4.52 | Custom/ quote-based | Not disclosed | Not disclosed | Not disclosed |

| Easy Pay Direct | 4.44 | $39 | Yes (via partners) | Not disclosed | 24-48 hours |

| Durango Merchant Services | 4.35 | $30 | Yes | Not disclosed | 4-6 business days |

| SoarPay | 4.25 | Custom | No | Not disclosed | Pre-approval within 24 hrs; full approval 3-5 business days |

| PayKings | 4.23 | $25-$75 | Yes | ~99% | 24-48 hour setup |

| Flowhub Pay | 4.19 | $0 | No | Not disclosed | 1 business day |

| Payline Data | 4.13 | Custom | No | Not disclosed | 1-3 business day |

*The Member Alert to Control high risk Merchants (MATCH) list is a register of all merchants that have had their accounts terminated in the past. Previously known as terminated merchant file (TMF) list, it includes businesses that were found to be in violation of their merchant services agreement, such as high chargeback ratio and non-compliance. Businesses remain on the MATCH list for a period of five to seven years.

Why you can trust TechnologyAdvice

My high risk merchant account recommendations are based on more than three years of evaluating merchant account services providers across different industries and business types. I spent hours of research comparing available features and gathering feedback from real-life users to score each one based on a 22-point criteria.

PaymentCloud: Best overall high risk merchant account provider

Overall Score

4.59/5

Pricing

4.69/5

Features

4.64/5

Support & Reliability

4.50/5

User Experience

4.50/5

Average User Review Scores

4.70/5

Pros

- Customizable fee structure

- Payment gateway–agnostic

- Supports surcharge-based “zero-cost” credit card processing*

- Works with MATCH list businesses

- Dedicated account managers

Cons

- Monthly account fees apply

- No guaranteed same-day funding

Why I chose PaymentCloud

PaymentCloud is a high risk merchant account provider known for its hands-on, white-glove approach to underwriting and onboarding. It supports a broad range of high risk and regulated industries, including healthcare-related services, professional services, ecommerce, subscription businesses, and other chargeback-prone models, and is one of the few providers that openly works with MATCH-listed merchants on a case-by-case basis.

What sets PaymentCloud apart is its flexibility. Instead of forcing merchants into a fixed pricing or gateway setup, PaymentCloud builds each account around the business’s risk profile, processing history, and operational needs. Pricing structures can be tailored (interchange-plus, tiered, flat-rate, or subscription-style), and merchants are not locked into a proprietary gateway. This allows businesses to keep their existing ecommerce platform, POS system, or integrations and avoid unnecessary downtime during onboarding.

PaymentCloud is compatible with popular POS systems such as Clover and, depending on the offer and merchant profile, may provide promotional hardware such as a smart terminal. As with all high risk merchant accounts, rates and fees are typically higher than those for low-risk processors, but PaymentCloud offsets this with strong approval support, flexible contracts, and ongoing account management.

PaymentCloud uses custom, risk-based pricing. The fees below reflect commonly reported averages from PaymentCloud representatives and third-party reviews; actual costs vary by business type, processing history, and bank placement.

- Monthly fee: $10-$45

- Mid risk transaction fee: 2.3%-3.4%

- High risk transaction fee: 2.7%-4.3%

- Early termination fee: Waived

- Payment gateway fee: $15

- Virtual terminal fee: $15-$45

- Rolling reserve requirement*: 0-10%

- Chargeback fee: $25

- Free smart wireless terminal

*A rolling reserve is a common requirement for high risk merchant accounts. It withholds a percentage of processed funds for a set period to offset chargeback and fraud risk. Reserve terms vary by acquiring bank and are periodically reviewed.

- Payment gateway–agnostic: PaymentCloud works with most major payment gateways, allowing merchants to retain their existing ecommerce carts, billing systems, or integrations. If needed, the team can also recommend alternative gateways better suited to specific high risk use cases.

- Customized pricing and account structure: Rather than using a one-size-fits-all model, PaymentCloud tailors pricing, reserve terms, and account configuration based on the merchant’s risk level, volume, and history. This flexibility can be especially valuable for growing or previously declined businesses.

- Hands-on onboarding and underwriting support: PaymentCloud assigns dedicated account managers who guide merchants through documentation, underwriting requirements, and bank placement. This level of support improves approval odds, particularly for high risk or MATCH-listed applicants.

- Surcharge-enabled credit card processing: PaymentCloud supports compliant credit card surcharging programs that allow eligible merchants to pass processing costs to customers. Availability depends on state laws, card brand rules, and business eligibility.

Related: Learn why PaymentCloud is among my top alternatives for Stripe.

PaymentCloud user sentiment is largely positive, with many reviewers praising the company’s staff, guided onboarding, clear communication, and help getting businesses approved. Some negative reviews mention concerns around partner processors, fund holds, account reviews, or transparency after approval.

My take: PaymentCloud remains a strong choice for hard-to-place merchants, but applicants should confirm which bank or processor will underwrite the account, how reserves work, and who handles support after approval.

Host Merchant Services: Best for transparent pricing and polished user experience

Overall Score

4.52/5

Pricing

4.69/5

Features

4.46/5

Support & Reliability

4.50/5

User Experience

4.50/5

Average User Review Scores

4.30/5

Pros

- Transparent, interchange-plus pricing

- No long-term contracts or early termination fees

- Strong fraud prevention tools, including 3D Secure support

- Wide range of POS and ecommerce integrations

Cons

- Not designed for hard-to-place or MATCH-listed merchants

- Limited support for highly regulated or restricted industries

Why I chose Host Merchant Services

Host Merchant Services earns its spot for its transparent pricing, flexible contracts, and polished user experience, which are uncommon among providers that support higher-risk business models. It offers interchange-plus pricing with no long-term contracts or early termination fees, making it a strong choice for businesses that want predictable costs without being locked in.

HMS supports many edge high risk industries, including ecommerce, subscriptions, nutraceuticals, and federally compliant CBD, and pairs this with modern fraud tools like 3D Secure and responsive customer support. While it’s not designed for hard-to-place or MATCH-listed merchants, Host Merchant Services is an excellent fit for growing businesses with manageable risk profiles that prioritize clarity, usability, and support.

Host Merchant Services uses a transparent interchange-plus pricing model tailored to each business’s transaction volume, card mix, and sales channels. Rather than publishing a single flat rate, HMS structures pricing around actual interchange fees plus a small, clearly defined markup, which helps reduce overall processing costs as volume grows.

- Pricing model: Interchange-plus (wholesale interchange + processor markup)

- Monthly account fee: Typically low or variable based on plan and volume; often around $14.99/month on standard plans and may be waived with higher volume or certain pricing structures

- Interchange-plus rates: Example published ranges include:

- Retail (card-present): ~Interchange + 0.20%-0.25% + ~$0.09-$0.10 per transaction

- Ecommerce: ~Interchange + ~0.35% + ~$0.10 per transaction

- Gateway fee: Optional (often ~$5/month) depending on gateway choice

- Annual or compliance fees: May apply (e.g., PCI reporting or statement fees)

- Contract: Month-to-month with no early termination fees

- Funding: Next-day funding available for eligible accounts

- Transparent interchange-plus pricing: HMS avoids teaser rates and long-term lock-ins, offering clear pricing that scales predictably as businesses grow.

- Advanced fraud and authentication tools: Host Merchant Services supports AVS, CVV, velocity rules, and 3D Secure, helping reduce fraud and mitigate chargebacks for ecommerce and subscription-based merchants.

- Broad integrations for ecommerce and POS: Merchants can integrate HMS with a wide range of ecommerce platforms, gateways, and POS systems, supporting both online and in-person sales.

- Highly rated customer support: HMS consistently earns strong user reviews for its responsive, knowledgeable support team, which assists merchants throughout onboarding and ongoing account management.

Host Merchant Services has strongly positive user sentiment. Reviewers frequently mention responsive support, smooth setup, helpful account reps, and improved payment workflows for small businesses and nonprofits.

Easy Pay Direct: Best for high risk SaaS and subscription-based businesses

Overall Score

4.44/5

Pricing

3.44/5

Features

5/5

Support & Reliability

4.75/5

User Experience

4.25/5

Average User Review Scores

3.80/5

Pros

- Built specifically for high risk and subscription-based businesses

- Advanced payment routing and redundancy options

- Supports MATCH-listed merchants on a case-by-case basis

- Strong recurring billing and subscription management tools

- Gateway-agnostic with broad integrations

Cons

- Higher upfront and ongoing costs than most traditional processors

- Not ideal for small or low-volume merchants

- Pricing is less transparent than interchange-plus providers

Why I chose Easy Pay Direct

Easy Pay Direct is a high risk payment gateway and merchant account provider designed for businesses with complex risk profiles, particularly SaaS, digital products, coaching, and subscription-based models. Rather than focusing on basic card processing, Easy Pay Direct emphasizes approval survivability, offering tools that help businesses reduce declines, manage risk, and maintain processing continuity as they scale.

One of Easy Pay Direct’s standout strengths is its payment routing and redundancy capabilities. Merchants can distribute transactions across multiple acquiring banks and MIDs, which helps reduce downtime, mitigate processor shutdown risk, and improve approval rates — features that are especially valuable for high-volume or fast-growing businesses.

Easy Pay Direct also supports businesses that have been declined elsewhere, including MATCH-listed merchants, although approvals are handled on a case-by-case basis. While it is not the lowest-cost option on this list, its technology-first approach makes it a strong choice for businesses that prioritize stability, scalability, and long-term processing resilience over minimal fees.

Easy Pay Direct publishes standard gateway pricing, though total processing costs vary based on business risk, volume, and acquiring bank placement.

- One-time setup fee: ~$99 (online gateway)

- Monthly gateway fee: ~$36 (online only)

- Transaction fees: Vary by processor and risk profile

- Rolling reserve: May apply, depending on underwriting

- Early termination fee: Not disclosed

- Contract terms: Varies by acquiring bank

Easy Pay Direct’s pricing reflects its focus on advanced routing, redundancy, and subscription-management capabilities rather than low-cost processing.

- Advanced payment routing and redundancy: Easy Pay Direct allows merchants to route transactions across multiple processors and acquiring banks, reducing the risk of account shutdowns and improving approval stability for high risk businesses.

- Subscription and recurring billing optimization: Built with SaaS and continuity businesses in mind, Easy Pay Direct offers tools to manage recurring billing, retries, declines, and subscription lifecycles more effectively.

- Gateway-agnostic integrations: Merchants can integrate Easy Pay Direct with a wide range of ecommerce platforms, CRMs, and billing systems, making it suitable for complex or custom tech stacks.

- Support for high risk and MATCH-listed merchants: Easy Pay Direct works with businesses that have elevated risk profiles or prior account issues, though approvals depend on documentation, compliance, and underwriting review.

Easy Pay Direct has mixed user sentiment. Positive reviews often mention helpful support and strong tools for online or high risk payment processing, while negative reviews raise concerns about account closures, fund holds, approval friction, subscription payment issues, and unclear fees.

Durango Merchant Services: Best for businesses in hard-to-place industries

Overall Score

4.35/5

Pricing

4.38/5

Features

4.29/5

Support & Reliability

4.50/5

User Experience

4.25/5

Average User Review Scores

4/5

Pros

- Specializes in hard-to-place and previously declined merchants

- Works with MATCH-listed businesses

- Strong domestic and international banking relationships

- Supports omnichannel and cross-border payments

- Dedicated high risk account managers

Cons

- Slower approval timeline than some competitors

- Does not support marijuana-related businesses

- No guaranteed same-day funding

Why I chose Durango Merchant Services

Durango Merchant Services is a long-established provider specializing in hard-to-place and previously declined high risk merchants. With decades of experience and a broad network of US and international banking partners, it offers strong approval odds for businesses operating in heavily scrutinized industries.

Durango also works with MATCH-listed merchants on a case-by-case basis and provides customized pricing based on risk profile and transaction flow. While approvals can take longer and require more documentation, Durango is a reliable choice for businesses that need flexible underwriting and international processing support.

Durango Merchant Services offers custom, risk-based pricing. The fees below reflect commonly reported averages provided by Durango representatives and third-party reviews; actual pricing varies by industry, volume, and bank placement.

- Monthly fee: $30

- Ecommerce/MOTO processing: Interchange plus 0.25% (markup)

- Payment gateway fee: 10 cents per transaction

- Authorization fees: 15-25 cents

- Rolling reserve requirements: 0%-10%

- Chargeback fee: $25

- Early termination fee: $0 (month-to-month contracts)

- Recurring billing and subscription management: Durango supports recurring billing and subscription payments, with a secure customer vault hosted in a PCI Level 1–certified environment.

- Authorize.Net emulator support: For merchants migrating from Authorize.Net, Durango offers an emulator that allows existing shopping carts and integrations to continue functioning with minimal changes.

- Fraud management tools: Merchants can configure fraud filters and manually review transactions to reduce fraud and chargeback exposure, particularly for card-not-present and international transactions.

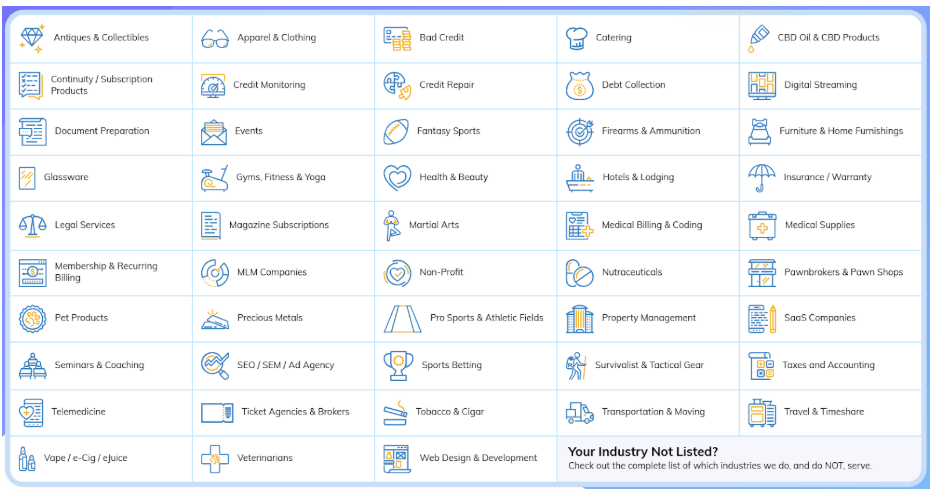

- Multicurrency and international support: Durango enables acceptance of 26 international currencies across more than 200 countries, with gateway localization in up to 15 languages and options for fixed or variable currency conversion.

Durango Merchant Services has mixed sentiment, though many positive reviews emphasize its ability to help businesses that were declined elsewhere. Users often mention strong communication, repeat account approvals, and help dealing with banks.

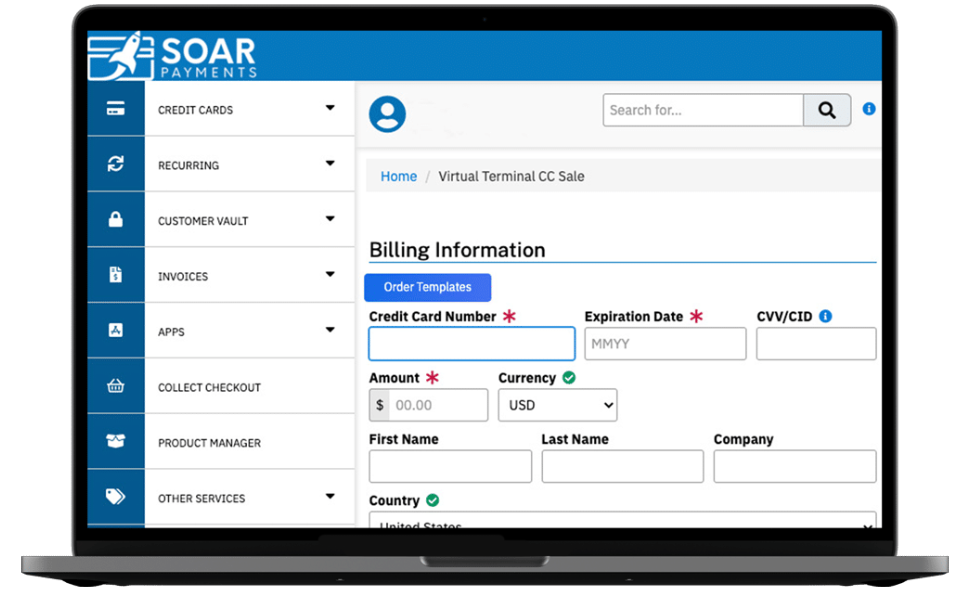

SoarPay: Best mid-market high risk specialist

Overall Score

4.25/5

Pricing

4.06/5

Features

4.29/5

Support & Reliability

4.5/5

User Experience

4.5/5

Average User Review Scores

4/5

Pros

- Specializes in high risk merchant accounts

- Supports a wide range of regulated and higher-risk industries

- Dedicated account managers and consultative onboarding

- Omnichannel payment support (online, in-person, MOTO)

- Flexible, risk-based underwriting

Cons

- Does not work with MATCH-listed merchants

- Pricing is not publicly disclosed

- Approval times can be longer for higher-risk profiles

Why I chose SoarPay

SoarPay is a well-established high risk merchant account provider designed for growing businesses that need more underwriting flexibility than traditional processors but don’t require hard-to-place or offshore solutions. It supports many higher-risk industries, including CBD, nutraceuticals, firearms-related businesses, travel, and subscription-based ecommerce.

What makes SoarPay stand out is its balanced approach to risk and usability. Merchants receive dedicated account managers and customized account setups, while still benefiting from modern payment tools and omnichannel support. While Soar does not work with MATCH-listed merchants, it is a strong option for mid-market businesses with elevated risk that are still operationally compliant and scaling.

Soar Payments offers custom, risk-based pricing based on business type, processing history, volume, and sales channels. Specific rates are not publicly listed and are provided during underwriting.

- Monthly account fee: Custom

- Transaction fees: Custom (risk-based)

- Rolling reserve: May apply, depending on risk profile

- Chargeback fees: Varies

- Early termination fee: Not disclosed

- Contract terms: Varies by acquiring bank

- High risk industry support: Soar Payments works with a wide range of higher-risk industries that are often declined by low-risk processors, provided the business is compliant and not MATCH-listed.

- Dedicated account management: Merchants are assigned account managers who assist with underwriting, documentation, and account setup throughout onboarding.

- Omnichannel payment acceptance: Soar supports online payments, in-person transactions, and mail/telephone orders, allowing businesses to sell across multiple channels.

- Risk and fraud management tools: The platform includes standard fraud prevention features to help manage chargebacks and reduce transaction risk.

SoarPay has mixed but generally positive sentiment. Positive reviews mention helpful service, strong communication, and support for niche or higher-risk businesses. Negative sentiment is more concentrated, so merchants should ask clear questions about pricing, approval requirements, and account expectations upfront.

PayKings: Best for businesses with growing chargeback claims

Overall Score

4.13/5

Pricing

3.13/5

Features

4.46/5

Support & Reliability

4.75/5

User Experience

4.25/5

Average User Review Scores

4/5

Pros

- Works with MATCH-listed merchants (case-by-case)

- Strong chargeback monitoring and mitigation tools

- Supports online and in-person payments

- Customizable fraud and risk controls

- Dedicated account managers

Cons

- Monthly and setup fees apply

- Approval process can take several business days

- Limited international payment support

Why I chose PayKings

PayKings is a high risk merchant account provider designed for businesses that struggle with elevated or increasing chargeback ratios. Rather than focusing solely on fast approvals, PayKings emphasizes risk management and dispute prevention, making it a strong option for merchants that need to stabilize their accounts to avoid termination or MATCH list placement.

What sets PayKings apart is its proactive approach to chargeback mitigation. The platform includes automated chargeback alerts, built-in dispute response tools, and refund and cancellation management features that help resolve customer issues before they escalate into formal disputes. PayKings also offers configurable risk controls, allowing merchants to fine-tune fraud prevention rules and reduce false declines.

PayKings works with MATCH-listed merchants on a case-by-case basis and assigns dedicated account managers familiar with different high risk verticals. While approvals are not instant and fees tend to be higher than low risk processors, PayKings is a strong fit for businesses that need hands-on support and structured chargeback management rather than just basic payment acceptance.

PayKings uses custom, risk-based pricing. The ranges below are estimates published on the PayKings website and confirmed by third-party reviews; actual fees vary by business profile and underwriting outcome:

- Monthly fee: $25-$75

- Transaction fee: 2.9%-4.5%

- Setup fee: $100-$300

- Early termination fee: Not disclosed

- Rolling reserve: May apply, depending on risk profile

- Proactive chargeback mitigation: PayKings offers automated alerts, built-in dispute tools, and refund/cancellation management to help merchants address issues before they result in chargebacks.

- Fraud and risk controls: Merchants can configure fraud rules and risk-scoring settings to balance security with approval rates and reduce false positives.

- Omnichannel payment support: PayKings supports ecommerce, virtual terminal, and mobile/in-person payments, allowing merchants to accept payments across channels.

- Fully online application process: Merchants can apply through PayKings’ online portal, which provides guidance on documentation requirements and underwriting expectations.

PayKings has very positive user sentiment. Reviewers frequently praise its staff for being helpful, knowledgeable, and efficient, especially during setup and approval.

Flowhub Pay: Best for cannabis payment processing

Overall Score

4.19/5

Pricing

4.06/5

Features

3.39/5

Support & Reliability

5/5

User Experience

4.75/5

Average User Review Scores

3/5

Pros

- Designed specifically for licensed cannabis businesses

- Compliant alternative to credit card processing

- Fast setup once documentation is approved

- Integrates with Flowhub POS and select cannabis POS systems

- Strong support and industry expertise

Cons

- Does not support credit card payments

- Customer convenience fees apply per transaction

- Requires one-time hardware and setup costs

Why I chose Flowhub Pay

Cannabis businesses face some of the strictest banking and payment restrictions in the US, which makes traditional high risk merchant accounts difficult — or impossible — to obtain. Flowhub Pay is built specifically for licensed cannabis retailers, offering a compliant way to accept payments without relying on credit cards.

Instead of card payments, Flowhub Pay enables ACH and debit-based transactions in line with cannabis banking requirements. The solution is deeply integrated with the Flowhub POS system but can also operate as a standalone payment terminal or alongside other cannabis POS platforms. For dispensaries that struggle to secure banking relationships, Flowhub can also connect merchants with cannabis-friendly banking partners.

While Flowhub Pay lacks the flexibility and customization of general high risk processors, its ease of use, regulatory alignment, and industry-specific design make it one of the most reliable payment options available for cannabis retailers.

Because cannabis merchants cannot legally accept credit cards, Flowhub Pay does not charge traditional credit card processing fees. Instead, costs are structured around hardware and customer-paid convenience fees.

- Monthly fee: $0

- Transaction fee: $0

- Customer convenience fee: Charged per transaction

- Hardware fee: One-time (varies by terminal)

- Setup fee: One-time (not publicly disclosed)

- Early termination fee: $0

- Compliant, non-card payment processing: Flowhub Pay enables ACH and debit-based payments designed to align with cannabis banking requirements, avoiding the risks associated with card network violations.

- POS-integrated or standalone operation: Flowhub Pay works natively within Flowhub POS but can also function as a standalone terminal or alongside other cannabis POS systems.

- Industry-specific compliance tools: Flowhub offers optional add-ons such as ID verification and compliance monitoring tools built for cannabis retailers.

- Banking partner support: Flowhub assists cannabis businesses in accessing banking services through its network of cannabis-friendly financial institutions.

Flowhub’s available Capterra review sample is very limited, so I would not weigh it heavily. The available review points to concerns about customer support and unresolved reporting questions, while the product profile shows features relevant to cannabis retail, including POS, inventory, reporting, and multi-location tools.

Payline Data: Best for merchants transitioning out of high risk

Overall Score

4.13/5

Pricing

4.38/5

Features

4.29/5

Support & Reliability

3.75/5

User Experience

4/5

Average User Review Scores

4.87/5

Pros

- Transparent interchange-plus pricing

- No long-term contracts

- Strong reporting and analytics tools

- Supports ecommerce and B2B payments

- Reputable, well-established provider

Cons

- Not a hard-to-place or MATCH-list specialist

- Limited tolerance for ongoing high chargeback ratios

- Fewer advanced risk-routing tools than high risk specialists

Why I chose Payline Data

Payline Data is best suited for businesses that are on the edge of high risk or actively transitioning out of a high risk classification. While it is not a hard-to-place merchant account provider, Payline offers transparent pricing and a reliable processing infrastructure for merchants whose risk profiles are stabilizing.

What stands out about Payline Data is its commitment to interchange-plus pricing with minimal add-on fees, which is uncommon among providers willing to work with higher-risk ecommerce and B2B businesses. Merchants also benefit from clear contract terms, strong reporting tools, and a straightforward onboarding experience.

Payline Data is not designed for MATCH-listed businesses or companies with severe chargeback issues. However, for merchants that have improved their chargeback ratios, strengthened compliance practices, or outgrown higher-cost high risk providers, Payline can be a strong next step.

Payline Data uses interchange-plus pricing and does not publicly publish fixed rates. Pricing varies based on business type, processing volume, and sales channel.

- Monthly fee: Custom

- Transaction fee: Interchange plus markup

- Setup fee: Not disclosed

- Early termination fee: $0 (month-to-month contracts)

- Rolling reserve: Not typical; may apply in select cases

- Interchange-plus pricing transparency: Payline Data emphasizes straightforward pricing with fewer bundled fees, making it easier for merchants to understand true processing costs.

- Ecommerce and B2B integrations: Payline integrates with common ecommerce platforms, virtual terminals, and invoicing tools to support online and card-not-present transactions.

- Reporting and analytics: Merchants have access to detailed transaction reports, settlement data, and performance insights through Payline’s dashboard.

- ACH and alternative payment support: In addition to card payments, Payline supports ACH processing for eligible businesses.

Payline Data has positive sentiment on Capterra, though the review sample is small. Users praise ease of use, stable payment processing, fair fees, virtual terminal access, and customer service. Some feedback notes that pricing can feel high or that product options under the same company can be confusing.

How to choose a high risk merchant account provider

The best high risk merchant account provider depends on your industry, chargeback risk, payment methods, processing history, and approval needs. Before applying, compare providers by underwriting fit, contract terms, fraud tools, and how clearly they explain fees and reserves.

Step 1: Match the provider to your industry

Start with providers that already support your business type. High risk industries vary widely, so a processor that works with CBD, coaching, nutraceuticals, travel, or adult businesses may not support every other high risk category.

Step 2: Ask about approval requirements upfront

Before submitting a full application, ask what documents the provider needs and whether your business model is likely to qualify. This can help you avoid unnecessary declines and repeated credit or underwriting checks.

Step 3: Compare fees, reserves, and contract terms

High risk accounts often come with higher rates, monthly fees, rolling reserves, and stricter contract terms. Ask for reserve percentages, review timelines, cancellation terms, chargeback fees, and gateway costs in writing.

Step 4: Review chargeback and fraud tools

Look for fraud filters, 3D Secure, chargeback alerts, dispute tools, velocity controls, and clear billing descriptor support. These tools can help reduce disputes and improve account stability.

Step 5: Check payment and gateway flexibility

Make sure the provider supports the payment methods and platforms you need, such as online checkout, recurring billing, ACH, virtual terminals, payment links, subscriptions, shopping carts, or gateway integrations.

Step 6: Test support before applying

High risk merchants need responsive support during underwriting, chargebacks, and account reviews. Contact the provider before applying to see how quickly and clearly they answer questions about pricing, reserves, approval odds, and documentation.