Quick answer: Square is the best free merchant account for most small businesses because it has no monthly fee, no setup cost, built-in payment processing, free POS tools, and fast activation. Helcim is better for B2B businesses that want interchange-plus pricing, while Stripe is best for online payments and ecommerce.

A free merchant account allows businesses to accept credit and debit card payments without paying monthly fees or setup costs, often bundling payment processing with point-of-sale (POS) or online checkout solutions. These accounts can streamline operations and improve cash flow for small businesses with tight budgets, while larger businesses benefit from scalable, cost-effective processing that supports higher transaction volumes.

If you’re in the market for a free merchant account, I’ve evaluated the top providers to help you find the best option for your business needs.

The six best free merchant accounts for 2026 are:

| Provider | Best for | Paid plan starts at |

| Square | Overall free merchant account | $49 per month |

| Helcim | B2Bs | No paid plans |

| Stripe | E-commerce | No paid plans |

| Payment Depot | Growing local U.S. merchants | No paid plans |

| PayPal | Freelancers | No paid plans |

| Adyen | International payments | No paid plans |

Featured partners

Best free merchant accounts compared

Company

Our score

(out of 5)

Transaction fee structure

Chargeback fee

Merchant account type*

Funding speed

4.62

Flat rate, custom rate for enterprise merchants

Waived up to $250/month

Aggregated

1-2 business days

(same day with fee)

4.20

Interchange plus with automated volume discounts

$15 refundable

Dedicated

Next business day

4..07

Flat rate or custom interchange plus

$15

Aggregated

1-2 business days

(same day with fee)

4.07

Custom interchange plus

$25

Dedicated

2 business days

(next business day with fee)

4.04

Flat rate

$15-$20

Aggregated

1-2 business days

(same day with fee or instant via PayPal balance)

*A merchant account can either be dedicated (traditional) or aggregated (shared). Payment facilitators like Square and PayPal hold a primary merchant account, which is then shared among their merchant clients. Although it provides less flexibility than traditional accounts, a shared account allows businesses to skip the lengthy approval process for a faster and simpler setup. Meanwhile, a dedicated merchant account means fewer risks of account holds and more stability as you grow.

When evaluating the best free merchant account services, I focused on identifying the most feature-rich and cost-effective providers, with software, hardware, and payment processing tools that can scale to accommodate new, mid-market, and enterprise-level businesses.

After careful consideration, I narrowed down my list to the following:

- Square

- PayPal

- QuickBooks

- Stripe

- Helcim

- Chase Payment Solutions

- Wave Payments

- Payanywhere

- Braintree

- US Bank Merchant Services

- Payment Depot

- Adyen

- Fiserv via Clover

I then hand-picked six providers based on the following criteria:

- Pricing & contract (30%): I looked closely at the true cost of doing business, beyond just the monthly fee. I awarded top marks to providers that offer free or low-cost card readers, transparent interchange-plus pricing, no volume commitments, and zero cancellation or chargeback fees. These are the accounts I trust to offer real value, especially for businesses that can’t afford hidden costs or restrictive terms.

- Account features (30%): I assessed whether a merchant account can grow with your business, and that starts with scalable infrastructure and fast deposit speeds. I prioritized providers that offer built-in tools like POS systems, dispute management, and cloud-based reporting, ideally without extra charges. The best options also provide hardware flexibility and strong, built-in security, so you’re never locked into outdated technology or risky compliance gaps.

- Transaction features (25%): A great merchant account should let you accept payments however your customers prefer, whether in person, online, or remotely. I looked for chip and contactless support, invoicing, virtual terminals, ACH/eCheck, and card-on-file capabilities, all ideally included without hidden fees.

- User experience (15%): I evaluated both aggregate review scores from platforms like Capterra and G2, as well as the quality of support, onboarding, and everyday usability. I know how frustrating poor service or clunky interfaces can be, especially when you’re running a business, so I awarded the highest marks to providers that are consistently well-reviewed, easy to get started with, and stand behind their products with great support.

Note that the scores are based on current available pricing and features, while the criteria set reflects the latest in POS technology and customer demands. All product scores are re-evaluated during every update to ensure that I provide you with the most relevant recommendations.

Why you can trust my advice

My recommendations for the best free merchant account are based on more than seven years of experience evaluating POS systems, payment processors, merchant accounts, and retail software. My background includes hands-on testing of payment terminals, mobile card readers, Tap to Pay tools, online checkout flows, virtual terminals, invoicing tools, and in-person payment workflows.

To score each one, I compared system specifications on 22 data points, tested the system when possible, and gathered feedback from real-life users.

Square: Best overall (and for new merchants)

Overall Score

4.62/5

Pricing

4.63/5

Account features

4.38/5

Transaction features

4.75/5

User experience

4.75/5

Pros

- No monthly fees for merchant account

- Easy setup and onboarding

- Robust POS features

- Transparent flat-rate pricing

Cons

- Higher fees for small tickets

- Account stability issues

- Few advanced customization options

Why I chose Square

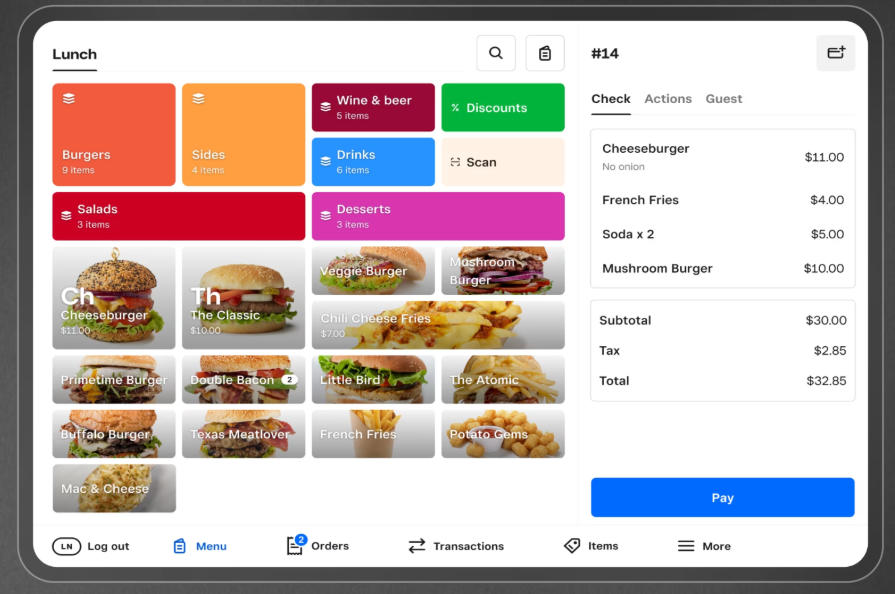

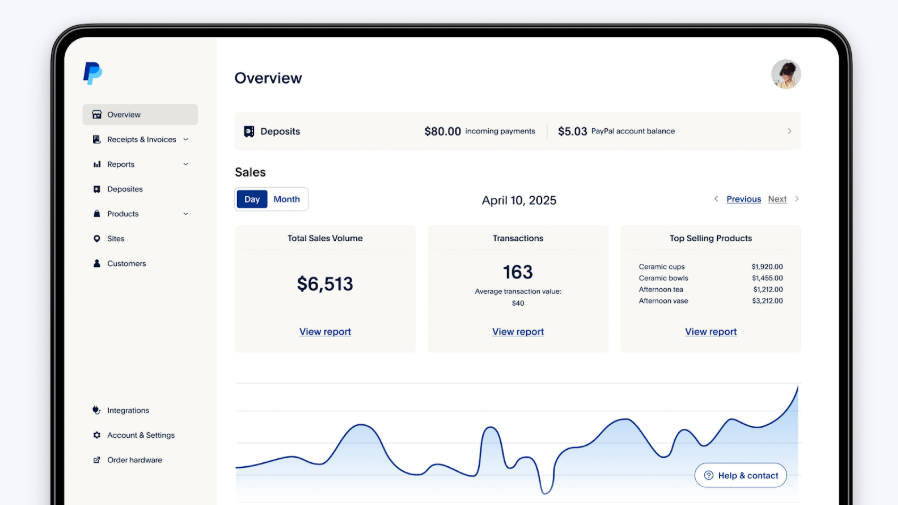

Square is primarily a POS solution that provides a suite of tools for businesses to accept payments, manage operations, and grow sales both online and in-person. It’s known for offering a simple, all-in-one system with the most feature-rich free plan. This, combined with its ease of setup and little to no upfront cost, earned Square the top spot in this guide.

I like how Square simplifies both merchant account setup and payment processing, making it accessible whether you’re a solo entrepreneur or managing multiple locations. Its free plan offers strong value and lets businesses start accepting payments quickly, often the same day. I’ve also found its flat-rate pricing structure to be clear and predictable, with no hidden fees or unexpected rate changes.

Additionally, Square’s sleek, mobile-friendly hardware is perfect for events and pop-up shops, while its ecosystem of tools makes it easy to scale as your business grows. Square adapts to your needs without locking you into long-term contracts whether you’re just starting or expanding,

Square is also featured in our roundup of the best credit card payment apps, where it stands out for its ease of use and mobile-friendly features.

Upfront cost: From $0; Square offers a free magstripe reader for each account and supports Tap to Pay for iOS and Android.

- Small brick-and-mortar businesses that need a simple way to accept in-person payments

- Mobile businesses, pop-ups, and event sellers that want fast setup and no monthly fee

- Solo operators and low-volume merchants that want built-in payment processing without a traditional merchant account setup

- Standard Square POS software

- Basic industry-specific POS software

- Invoicing with basic recurring billing

- Payments processing

- Virtual terminal

- Mobile POS app

- Customer directory

- Square e-commerce platform

- Square payment links (online checkout)

- Chargeback management

- Customizable reports

- Starter team management plan

- Shift management

- First magstripe mobile card reader

- Chargeback fee waived at $250/month

Transaction processing fees:

- In-person: 2.6% + 15 cents

- Online: 2.9% + 30 cents

- Keyed-in: 3.5% + 15 cents

- American Express transactions: $0

- Tap to Pay: + 10 cents per transaction

- Volume discounts: By request for businesses with sales volume greater than $250,000/year

- Chargeback fee: Waived up to $250 per month

- Application fee: $0

- Set up/ installation fee: $0

- Cancellation fee: $0

While Square’s free plan is generous and ideal for testing the waters, it has a few limitations that growing businesses should be aware of. First, the free plan doesn’t include advanced team management features, in-depth reporting, or tools like customer loyalty programs and marketing automation. You will also need to upgrade to a paid plan if you intend to customize your online store.

If you start needing tools like employee time tracking, multi-location inventory management, or advanced API integrations, upgrading to a paid plan, such as Square Plus or Premium, becomes a smart move. The upgrade unlocks operational efficiency and richer insights that can fuel long-term business strategy.

Cost to upgrade:

- Software: From $49/month

- Hardware: From $10

- Feature-rich free plan: Square’s feature-rich free plan includes essential tools like POS software, invoicing, virtual terminal, mobile payments, and even a free online store. It’s designed to help small businesses start accepting payments and managing operations without upfront costs or monthly fees.

- Omnichannel payments: Square’s omnichannel payments feature lets you accept payments in-store, online, by invoice, or through a mobile device within one unified system. It seamlessly syncs sales and customer data across channels, making it easier to manage and grow your business.

- Security: Square is PCI-compliant by default, meaning you don’t have to manage your own compliance. Transactions are encrypted end-to-end and monitored 24/7 for fraud. Additionally, Square offers chargeback support and account security features, including two-factor authentication.

- Ease of onboarding: Getting started with Square takes minutes. There is no application process, approvals, or merchant ID required. Everything from account creation to hardware setup is guided and user-friendly, making it perfect for first-time business owners or seasonal vendors.

- Scalability: Square grows with your business. You can start with mobile payments and expand to a full POS system, e-commerce store, and even payroll, all within the same ecosystem. As you scale, you can add tools for inventory, marketing, customer engagement, and employee management.

- Dispute management: Square handles chargebacks on your behalf, collecting and submitting evidence to the bank. You can track dispute status directly from your dashboard. Their system also flags suspicious transactions and provides clear guidance to reduce the risk of future disputes.

Helcim: Best for B2B merchants

Overall Score

4.20/5

Pricing

4.44/5

Account features

3.69/5

Transaction features

5/5

User experience

3.5/5

Pros

- Interchange-plus pricing with built-in volume discounts

- Full free access to all payment services

- Free surcharging and discounts program

- Automated fee optimization for B2B transactions

Cons

- Surcharge for Amex transactions

- Limited hardware options

- No same-day deposits

Why I chose Helcim

Helcim is a full-service merchant account provider known for its transparent pricing, in-house payment processing, and built-in volume discounts. Unlike Square, Helcim offers true merchant accounts, which translates to greater stability and fewer unexpected account holds. Its interchange-plus pricing model ensures businesses know exactly what they are paying and that they will save significantly compared to flat-rate providers.

The combination of cost transparency and free, robust payment services features made Helcim an easy choice during my evaluation. Helcim doesn’t charge monthly fees to access any of its payment processing tools without the “customized fees,” which is rare in the merchant services space. And I especially like how Helcim automatically pulls Level 2 and 3 data for B2B transactions, ensuring businesses always receive the best possible interchange discounts without extra effort.

Overall, Helcim is an excellent choice if you need a solution that delivers enterprise-level payment solutions without the enterprise-level headaches. The all-in-one platform includes invoicing, recurring billing, e-commerce tools, and even inventory management, although like Square, this is exclusively for use with Helcim’s POS.

Helcim is also highlighted in our guide to the cheapest credit card processing options, thanks to its transparent pricing and low interchange-plus rates.

Upfront cost: $0 if you opt for a Tap-to-Pay for iOS setup; the basic Helcim card reader costs $199 upfront, or purchase the smart terminal on installment at $32/month for 12 months

- Growing service businesses that want transparent interchange-plus pricing and no monthly account fee

- Cost-conscious B2B businesses that process invoices, larger tickets, or recurring payments

- Wholesalers, automotive businesses, and professional service providers that want lower-cost processing as sales volume grows

- Payment processing

- Free merchant processing (Surcharging and cash discounts)

- Invoicing

- Subscription management

- POS software

- E-commerce tools

- Customer portal

- CRM

- Chargeback management

- Customizable reports

Transaction processing fees:

- In-person: Interchange plus 0.15% + 6 cents to 0.4% + 8 cents

- Online: Interchange plus 0.15% + 15 cents to 0.50% + 25 cents

- Keyed-in: Interchange plus 0.15% + 15 cents to 0.50% + 25 cents

- American Express transactions: + 0.10% + $0.10

- Volume discounts: Built-in, based on tiers

- Chargeback fee: $15

- Application fee: $0

- Set up/ installation fee: $0

- Cancellation fee: $0

Helcim is unique in that it technically doesn’t gatekeep features behind a traditional paid plan, as the core platform is free to use. However, you may still feel the need to “upgrade” in terms of adding volume-based services or optional hardware purchases.

For example, businesses processing higher volumes may choose to opt into custom interchange-plus rates that lower costs even further. The biggest limitation in the base account is that it doesn’t include advanced POS features, offline mode, or multi-user access unless you configure them manually.

Also, while the software is rich, scaling to multiple locations or integrating with other systems may require additional investment or developer support. So, while there’s no official paid plan tier, growing businesses will naturally reach a point where investing in extras becomes worthwhile.

Cost to upgrade:

- Software: $0

- Hardware: $199-$349

- Add-on tools: $0

- Free credit card processing: Helcim’s Fee Saver program lets merchants offset processing costs by adding a surcharge or offering a cash discount for both in-person and online payments, and it can be easily toggled on or off. Any business that accepts ACH payments and uses the Helcim Smart Terminal automatically qualifies for this program at no extra cost.

- B2B level 2 and 3 data processing: Helcim’s automated Level 2 and 3 data processing is built to optimize interchange fees for B2B and government transactions without requiring manual input. This feature is included at no extra cost, helping businesses consistently qualify for the lowest possible rates.

- Security: Helcim is PCI-DSS Level 1-compliant, ensuring top-tier security protocols for all transactions. It uses tokenization and encryption to protect customer data and offers built-in fraud detection tools. Merchants get peace of mind knowing sensitive information is never stored on their systems.

- Ease of onboarding: The sign-up process is fast, straightforward, and doesn’t involve complicated underwriting like many traditional merchant account providers. Approval is typically completed within a few days. Helcim also provides onboarding assistance and clear documentation for every feature.

- Scalability: Helcim supports growing businesses with integrated tools for ecommerce, subscriptions, inventory management, and customer relationship tracking. Its APIs and built-in tools help eliminate the need for third-party add-ons.

- Dispute management: Helcim offers centralized tools for tracking and responding to chargebacks within your dashboard. It provides proactive alerts and templates to streamline your response process. Unlike many processors, Helcim supports you directly rather than outsourcing dispute handling to third parties.

Stripe: Best for e-commerce businesses

Overall Score

4.07/5

Pricing

4.25/5

Account features

3.81/5

Transaction features

3.75/5

User experience

4.5/5

Pros

- Developer-friendly APIs and integrations

- Supports 135+ currencies and global payments

- Customizable pricing structure

- Robust tools for subscriptions and invoicing

Cons

- Limited in-person payment features

- Requires technical expertise for customization

- Potential for sudden account holds

Why I chose Stripe

Stripe is a developer-friendly payment processing platform designed for businesses of all sizes to accept payments online, in-app, or in-person. It powers many of the world’s top e-commerce brands and startups thanks to its flexible APIs and global reach.

For this guide. I chose Stripe because it gives me complete control over how businesses handle payments, subscriptions, and customer billing without needing to juggle third-party tools. Stripe particularly shines for online payments, with its highly customizable payment gateways that allow you to create seamless checkout processes tailored to your business needs. However, my favorite feature is its flexible pricing structure, where any merchant can apply to qualify for custom interchange-plus rates, unlike Square.

Overall, Stripe offers a powerful combination of performance, customization, and reliability that’s hard to beat. Its transparent flat-rate pricing structure and custom interchange-rate options make Stripe an ideal scalable solution for all business sizes. Stripe is simply unmatched for online-first businesses or those wanting to build custom checkout flows.

Stripe is also featured in our guide to Square Alternatives, making it a strong option for businesses seeking more customization and developer-friendly tools.

Upfront cost: Entirely free to sign up and set up, however, if you need an in-person payment solution, you will likely need to purchase a Stripe payment app from a third-party provider or develop your own. You will also need to invest in a Stripe card reader that starts at $59 or use tap-to-pay.

- Tech-savvy businesses that want a free online merchant account with developer-friendly tools

- SaaS companies that need subscriptions, recurring billing, automation, and custom checkout flows

- Ecommerce businesses that want strong API access, online payments, and flexible integrations

- Payment processing

- Stripe Checkout

- Payment Links

- Invoicing

- Recurring Billing

- API and SDK Integrations

- International payment methods

- Chargeback management

- Customizable reports

Transaction processing fees:

- In-person: 2.7% + 5 cents

- Online: 2.9% + 30 cents

- Keyed-in: 3.4% + 30 cents

- Tap-to-pay: +10 cents per transaction

- Volume discounts: Interchange plus for qualified businesses

- Invoicing: + 0.4%-0.5%

- Recurring billing: + 0.5%-0.8%

- Chargeback fee: $15

- Application fee: $0

- Set up/installation fee: $0

- Cancellation fee: $0

Stripe’s base offering is technically “free” in that there are no setup or monthly fees. You only pay per transaction. But many of the platform’s most powerful features, like Stripe Tax, advanced fraud protection (Radar for Teams), and Revenue Recognition, come with additional costs.

Larger teams benefit from paid features like granular roles and permissions or advanced reporting tools. If you’re scaling beyond basic e-commerce or need more control over financial workflows, a paid plan or custom pricing arrangement becomes necessary to unlock Stripe’s full capabilities.

Cost to upgrade:

- Software: $0

- Hardware: $59-$349

- Add-on tools: From $10

Related: Stripe alternatives

- Customized online checkout: Stripe Checkout offers advanced customization options that let you tailor the look, feel, and behavior of your payment page to match your brand. You can modify elements like colors, logos, payment methods, and even post-payment redirects all while maintaining PCI compliance and mobile optimization.

- Developer tool kit: Stripe provides powerful developer tools and well-structured APIs that make it easy to build and customize complex payment workflows. Its comprehensive, clearly documented API guides and SDKs support rapid development, seamless integration, and scalability for businesses of all sizes.

- Security: As with all my recommendations, Stripe is a PCI Level 1 service provider. It uses TLS encryption and tokenization to secure cardholder data and provides Radar, its AI-powered fraud prevention tool. Stripe also supports 3D Secure and dynamic authentication for higher-risk transactions.

- Ease of onboarding: Stripe’s onboarding is frictionless for developers and business owners alike. You can create an account in minutes, and integrations with platforms like Shopify, WooCommerce, and QuickBooks are well-documented and easy to implement. Developers also get access to test environments and API keys immediately, which speeds up launch time.

- Scalability: Stripe was designed with scalability in mind. Whether you’re processing 100 or 100,000 transactions a day, the infrastructure adapts to your needs. With global currency support, embedded finance features, and modular APIs, Stripe is built to grow with you.

- Dispute management: Stripe’s dashboard provides a clear view of chargebacks and disputes, including automatic alerts and response deadlines. You can submit evidence directly within the dashboard, and Stripe guides you through what’s required for each case. Its robust API also allows automation of dispute workflows if you’re managing high volumes.

Payment Depot: Best for growing local US businesses

Overall Score

4.07/5

Pricing

4.25/5

Account features

3.44/5

Transaction features

4.75/5

User experience

3.75/5

Pros

- Custom-interchange plus pricing

- No setup or cancellation fees

- Compatible with most business platforms

- 24/7 customer support

Cons

- Next-day funding with fee

- Does not support high-risk industries

- Only for local US merchants

Why I chose Payment Depot

Payment Depot is a dedicated merchant account service that offers low credit card processing with no hidden fees or long-term contracts. It provides a custom interchange-plus model with variable rates as low as 0.2% to 1.95%, delivering cost savings, especially for high-volume businesses.

I chose Payment Depot because it supports advanced merchant services solutions from Stax, its parent company, without the high monthly price point, making it the more scalable solution of the two. For a dedicated merchant account, its setup process is fast even for brick-and-mortar businesses. Its US-based customer support is also responsive.

Unlike Helcim, Payment Depot offers seamless API integration with a wide range of POS systems, e-commerce platforms (such as Shopify, WooCommerce, and 3dcart), hardware (including Clover POS), and payment gateways. It also integrates with invoicing and bookkeeping platforms, such as QuickBooks. This allows businesses to continue using the service even as they upgrade their hardware or software.

Upfront cost: $0 (if you already have your own payment terminal); Payment Depot can integrate with most payment gateways, but there may be an additional setup cost if you need a new one

- Small businesses with high credit and debit card transaction volume that want custom pricing and no monthly account fee

- B2B businesses with stable processing needs and predictable payment volume

- Businesses that like Helcim’s cost-focused model but want a wider range of hardware options

- Payment processing

- Dedicated merchant account

- Digital invoicing

- Text2Pay mobile payments

- API key integration capabilities

- Hosted payment pages

- Secure card vault with automated updates

- Account reconciliation

- Recurring billing and scheduled payments

- One-click shopping with catalog management

- Shareable payment links

- Chargeback management

- Customizable reports

Transaction processing fees:

- In-person: Custom interchange-plus rate

- Online: Custom interchange-plus rate

- Keyed-in: Custom interchange-plus rate

- American Express transactions: N/A

- Volume discounts: N/A

- Chargeback fee: $25

- Application/set-up fee: $0

- Cancellation fee: $0

There are no plan tiers with Payment Depot, but some features, such as next day funding, level 2 and 3 data processing, ACH processing, and e-commerce plugins, require add-on fees. If you’re hitting volume thresholds or want more integration flexibility, consider upgrading to Stax.

Cost to upgrade:

- Software: $0

- Hardware: From $59 for a basic SwipeSimple card reader, or use your own

- Add-on tools: Not disclosed

- Payment gateway flexibility: Payment Depot supports multiple payment gateways, including well-known options like Authorize.net, Network Merchants Inc. (NMI), and PayTrace. These gateways integrate seamlessly with leading e-commerce platforms, such as Shopify, offering flexibility and compatibility for growing businesses.

- Hardware flexibility: Payment Depot works seamlessly with a wide range of POS hardware and card terminals. It supports credit card processing through Clover’s full line of POS devices, while SwipeSimple’s mobile card reader and POS app are ideal for on-the-go payments. For businesses seeking a smart, standalone terminal, Dejavoo devices are also available and fully compatible.

- Security: Payment Depot ensures PCI compliance is built into every account. It works with top-tier processors that offer encryption, tokenization, and secure gateways. As a result, businesses get enterprise-grade security protections without needing to manage them manually.

- Ease of onboarding: The onboarding process is straightforward, typically taking one to two business days for approval. A dedicated account manager helps walk you through setup, whether you’re integrating e-commerce, in-store terminals, or mobile POS. Unlike aggregators, Payment Depot offers more personalized service from the outset.

- Scalability: With multiple membership tiers and compatibility with various hardware and software platforms, Payment Depot is well-suited for scaling. You can add users, locations, and integrations without switching providers. Plus, the flat-rate pricing ensures you’re not penalized for growth through higher percentage fees.

- Dispute management: As a full-service merchant account provider, Payment Depot gives you access to traditional chargeback resolution tools. You can receive notifications, respond through a processor-backed portal, and lean on customer support for guidance. Its model also reduces surprise holds, helping you maintain cash flow during dispute resolution.

PayPal: Best for freelancers and occasional sellers

Overall Score

4.04/5

Pricing

4.06/5

Account features

3.88/5

Transaction features

4.0/5

User experience

4.25/5

Pros

- Easy, fast setup

- Widely trusted brand

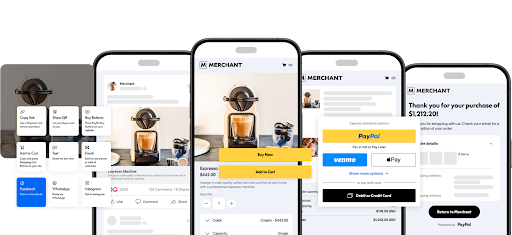

- Wide range of payment methods, including one-click solutions

- Integrated with major ecommerce platforms

Cons

- Monthly fee for virtual terminal

- Monthly fee for invoicing and recurring billing tools

- Account holds and freezes

Why I chose PayPal

PayPal is a globally recognized payment platform that allows businesses to accept online, in-person, and invoiced payments with ease. It offers a fast and familiar checkout experience for customers, as well as a broad range of tools that even freelancers and occasional sellers can easily manage from a smartphone.

I chose PayPal because of its brand trust, global reach, and frictionless setup and like Square, it is one of the easiest ways to start accepting payments in minutes. My favorite feature is PayPal’s ability to work as an add-on online payment method alongside most payment processors. And with built-in tools for e-commerce, invoicing, and recurring billing, businesses can manage their payment workflows without relying on third-party add-ons.

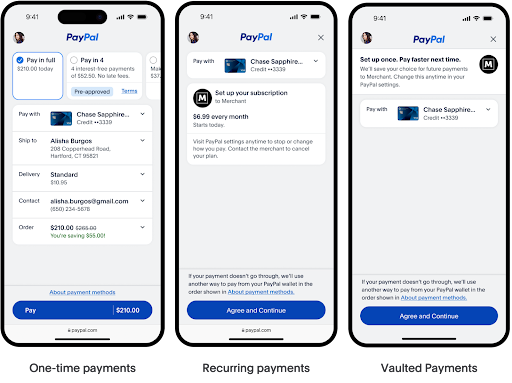

The ability to accept credit cards, PayPal balances, Venmo (US only), and Pay Later options provides businesses with flexibility in how they serve customers. There’s no need for a traditional merchant account or gateway integration as PayPal handles it all under one roof. PayPal is really a smart starting point if you’re looking for instant credibility and a streamlined way to process payments.

Upfront cost: From $0 for those who will opt to accept payments via Tap to Pay for iOS and Android. You can get your first PayPal card reader discounted at $29 (regular price at $79).

- Freelancers and occasional sellers that need fast setup and a familiar payment option

- Online service providers and digital goods sellers that want simple invoices, payment links, and checkout tools

- Businesses selling internationally that want access to PayPal’s global buyer network and faster access to funds

- PayPal payment methods

- Online card services

- Hosted checkout

- International payments processing

- Payment links

- PayPal POS software

- Nonprofit payments

- Instant funding via PayPal wallet

- Micro transactions

- Native BNPL tools

- Cryptocurrency payment processing

Transaction processing fees:

- In-person: 2.29% + 9 cents

- Online: 2.29% + $0.09 (QR) to 3.49% + $0.49

- Keyed-in: 3.49% + 9 cents

- American Express transactions: N/A

- Volume discounts: Interchange plus pricing for enterprise

- Chargeback fee: $15-$20

- Application/set-up fee: $0

- Cancellation fee: $0

As your business grows, you’ll likely need features only available through its paid solutions, such as PayPal Payments Pro, Advanced Credit and Debit Card Payments, or Braintree. For instance, if you want to host a fully branded checkout page, access advanced reporting, or use virtual terminals, those require a monthly fee.

You’ll also find that PayPal’s standard checkout flow keeps users on PayPal’s site, which can hurt conversions. Upgrading to a paid plan lets you embed the checkout into your own site for a more seamless customer experience. Additionally, larger businesses may outgrow the limited customization and integration options of the free plan and benefit from more robust developer tools and lower negotiated rates.

Cost to upgrade:

- Software: $0

- Hardware: From $79 for a basic card reader

- Add-on tools: From $5/month for a custom embedded checkout page

Related: Stripe vs. Paypal: Which is Better in 2025? and Square vs PayPal: Which Should You Choose?

- Online checkout compatibility: PayPal Checkout provides a flexible online payment solution that can serve as either your primary checkout system or an additional option alongside other processors. It integrates easily with most e-commerce platforms, giving customers the choice to pay using PayPal, credit/debit cards, or PayPal Pay Later, all without leaving your site.

- International payments: PayPal supports international payment processing in over 200 markets and accepts payments in 25+ currencies, making it ideal for global e-commerce. It automatically handles currency conversion and compliance, allowing businesses to reach international customers with minimal setup.

- Security: PayPal is PCI-compliant and encrypts every transaction using advanced security protocols. It also offers buyer and seller protection policies to reduce fraud risk. Account monitoring and AI-driven fraud detection help prevent unauthorized activity and chargebacks.

- Ease of onboarding: Signing up for PayPal is fast — just a few steps and you’re ready to accept payments. There’s no underwriting or application process like traditional merchant accounts. It integrates easily with ecommerce platforms like Shopify, WooCommerce, and BigCommerce.

- Scalability: PayPal supports everything from side hustles to enterprise-grade e-commerce. You can start with simple checkout buttons and grow into subscription billing, multi-user access, and global payments. Its business suite also includes lending, working capital, and partner integrations.

- Dispute management: PayPal offers a centralized Resolution Center for handling disputes and chargebacks. You’re guided through submitting evidence, timelines, and communication with buyers. While the system is standardized, PayPal acts as both processor and arbitrator, which may limit merchant control — but it simplifies the process for most use cases.

Adyen: Best for international businesses

Overall Score

3.84/5

Pricing

4.19/5

Account features

3.63/5

Transaction features

4.5/5

User experience

2.75/5

Pros

- Direct global acquiring network

- Dynamic currency conversion

- Single integration for multiple local payment methods

- Customizable embedded payment solutions

Cons

- Invoicing available via integration

- Complex pricing and setup for non-technical users

- May require a monthly minimum

Why I chose Adyen

Adyen is a global payment platform that provides businesses with a unified solution to accept payments across online, in-person, and mobile channels. Known for powering major brands like Salesforce and eBay, Adyen combines acquiring, processing, and risk management into a single platform, making it a strong contender in the embedded payments space.

I chose Adyen because it offers full-stack control over the entire payment lifecycle, which means better performance, fewer intermediaries, and increased visibility. But what truly elevates it is its ability to provide enterprise-grade infrastructure without compromising on flexibility. I also like how the platform’s modular structure allows businesses to start simple and add advanced features, such as tokenization or risk scoring, when they’re ready.

With support for 150+ currencies and hundreds of local payment methods, Adyen is most ideal for businesses with international ambitions. Though this may sound much like Stripe, Adyen offers seamless omnichannel commerce, helping businesses bridge the gap between digital storefronts and physical retail locations. For large B2Bs, its customizable embedded payment solutions make it especially attractive.

Upfront cost: From $0, Adyen supports Tap to Pay for iOS and Android as well as a wide range of payment terminals (pricing not disclosed)

- High-volume B2C businesses that process payments across multiple channels

- Enterprise and global brands that need international payment support and local payment methods

- Businesses looking for unified commerce across online, in-store, mobile, and cross-border sales

- Global payment processing

- Direct acquiring

- In-person POS solutions and hardware integration

- Unified omnichannel payment support

- Customizable embedded checkout

- Access to API-based integration and developer tools

- AI-powered fraud detection and risk management

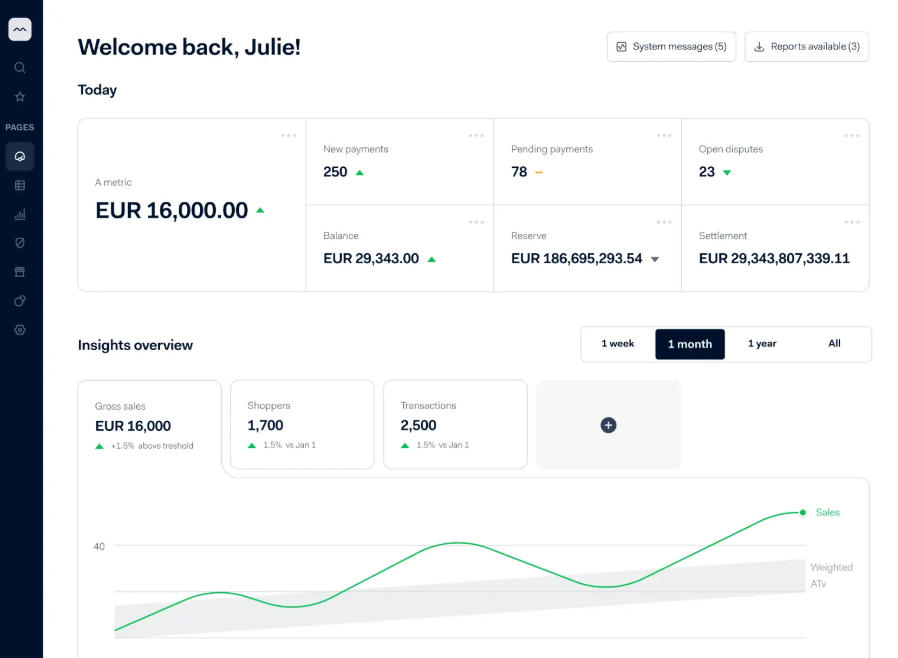

- Real-time payment analytics and reporting dashboard

- Dynamic payment routing

- Pay Later integration

Transaction processing fees:

- In-person: Interchange + 13 cents for Visa and MC, 3.3% + 23 cents for AmEx, 3%–3.95% + 13 cents for other card brands

- Online: Interchange + 13 cents for Visa and MC, 3.3% + 23 cents for AmEx, 3%–3.95% + 13 cents for other card brands

- Keyed-in: Interchange + 13 cents for Visa and MC, 3.3% + 23 cents for AmEx, 3%–3.95% + 13 cents for other card brands

- American Express transactions: N/A

- Volume discounts: Custom volume discounts

- Chargeback fee: $5-$100

- Application/set-up fee: $0

- Cancellation fee: $0

Adyen doesn’t operate on a traditional “free plan” model; it primarily targets mid-size to large businesses with a volume-based pricing structure. There’s no setup fee or monthly subscription, but you’ll still need to meet minimum volume requirements (typically $100K/month) to avoid being turned away.

Features like custom risk rules, payment orchestration, and advanced fraud tools are available, rare for inexpensive merchant account providers, but as your business scales or enters new markets, working with Adyen’s account team to enable more complex features and integrations becomes essential.

Cost to upgrade:

- Software: $0

- Hardware: Not disclosed

- Add-on tools: Varies, third-party integrations for invoicing and other tools

Related: How to Accept Payments Online

- Direct processor: Adyen offers direct acquiring capabilities that streamline payment processing and reduce failed transactions. By eliminating reliance on third-party acquirers, Adyen increases efficiency, speeds up settlements, and delivers a more stable experience.

- Dynamic payment routing: Adyen’s dynamic payment routing intelligently selects the most efficient path for each transaction based on real-time data, helping to maximize approval rates. By analyzing factors like card type, issuer location, and past performance, it automatically reroutes payments to the acquirer most likely to approve them, reducing declines and boosting revenue.

- Security: Adyen is PCI Level 1-compliant and offers end-to-end encryption, tokenization, and 3D Secure 2.0 for enhanced transaction security. Its real-time risk engine uses behavioral analytics and machine learning to prevent fraud. Businesses also benefit from built-in compliance and regulatory support across global markets.

- Ease of onboarding: Onboarding with Adyen can be more technical than with plug-and-play processors, but it’s well-supported by comprehensive API documentation and a dedicated implementation team. Larger merchants get personalized onboarding with technical consultations. Once live, the unified dashboard simplifies day-to-day management across all sales channels.

- Scalability: Adyen’s platform is built for scale, making it a strong fit for multi-region, high-volume businesses. It allows seamless expansion into new markets without needing new payment partners or systems. Features like recurring billing, payout splitting, and multicurrency settlement are already built-in and ready to activate.

- Dispute management: Adyen provides an integrated dispute management system with real-time alerts, evidence submission tools, and analytics on chargeback trends. It supports dynamic 3D Secure to reduce fraud-related disputes and optimize conversion rates. Merchants also receive guidance on improving authorization rates and reducing false declines.

Free merchant account vs free merchant processing

A free merchant account does not mean free payment processing. Most providers remove monthly or setup fees, but businesses still pay transaction fees, chargeback fees, hardware costs, or optional software fees.

| Term | What it means | What to watch for |

| Free merchant account | No monthly account fee or setup fee | You still pay transaction fees |

| Free merchant processing | Usually means surcharging or passing fees to customers | Rules vary by state, card type, and provider |

| No monthly fee processor | No recurring software or account fee | Processing rates, chargebacks, and hardware still apply |

| Inexpensive merchant account | Lower overall cost based on rates, fees, and volume | May require underwriting or minimum volume |

Free is not always cheapest: A provider with no monthly fee may be the best choice for new or low-volume businesses. But if your business processes higher monthly volume, a provider with interchange-plus or custom pricing may cost less overall, even if the account is not marketed as “free.”

How to choose the best free merchant account

Choosing the best free merchant account means looking beyond “no monthly fee.” A provider may be free to start, but you still need to compare transaction rates, hardware costs, funding speed, security tools, support, and how well the platform fits the way your business accepts payments.

Best free merchant account by business type

| Business type | Best free merchant account | Why |

| New small business | Square | Fast setup, no monthly fee, free POS tools, and built-in payment processing |

| B2B business | Helcim | Interchange-plus pricing, invoicing, Level 2 and Level 3 processing, and no monthly fee |

| Ecommerce business | Stripe | Free online merchant account with checkout, subscriptions, invoices, and developer tools |

| Growing local business | Payment Depot | No monthly fee, custom pricing, and hardware flexibility |

| Freelancer or solo seller | PayPal | Easy setup, payment links, invoicing, and familiar checkout for customers |

| International business | Adyen | Global payment support, multi-currency tools, and unified commerce features |

- Step 1: Start with how you accept payments. Decide whether you need in-person, online, mobile, invoice, ACH, recurring, or international payments. A freelancer may only need invoices and payment links, while a retailer may need POS tools, card readers, and same-day deposit options.

- Step 2: Check the real upfront cost. A free merchant account should not require setup, application, or monthly account fees just to get started. Still, check for hardware costs, gateway fees, add-ons, or optional software charges that can increase your total cost.

- Step 3: Compare pricing models. Look at how each provider charges for transactions. Flat-rate pricing is simple and predictable, while interchange-plus or custom pricing may be cheaper for businesses with higher volume, larger tickets, or B2B payments.

- Step 4: Review free plan limits. Check what is included for free and what requires an upgrade. Reporting, team access, custom branding, advanced fraud tools, invoicing, subscriptions, or ecommerce features may be limited depending on the provider.

- Step 5: Evaluate ease of setup and use. Choose a provider with minimal paperwork, clear terms, and a dashboard your team can use without extensive training. Look for fast onboarding, clean reporting, and integrations with your POS, ecommerce store, accounting software, or invoicing tools.

- Step 6: Check security and compliance. Your provider should support PCI-compliant payment processing and offer security tools such as encryption, tokenization, fraud detection, and chargeback monitoring. If you sell online, also check for tools like 3D Secure and fraud filters.

- Step 7: Review support and account stability. Free does not help much if you cannot get support when payments fail or funds are held. Review support channels, funding speed, chargeback assistance, account review policies, and whether the provider is suitable for your business type and sales volume.

Best free merchant accounts by feature

Some free merchant accounts are easier to start with, while others are better for security, scalability, dispute tools, or a stronger free feature set. Use the table below to match each provider to the feature that matters most for your business.

| Feature | Best providers | Why |

| Security | Adyen and Stripe | Adyen offers enterprise-grade PCI Level 1 compliance, 3D Secure 2.0, tokenization, and real-time risk tools for global payments. Stripe also offers strong security features, including 3D Secure, tokenization, and Stripe Radar. |

| Ease of onboarding | Square and PayPal | Square offers fast signup, no monthly fee, built-in payment processing, and pre-integrated POS tools. PayPal is also quick to set up and works across many online platforms. |

| Scalability | Stripe and Adyen | Stripe is a strong fit for growing digital businesses because of its API tools, global currency support, subscriptions, and modular payment features. Adyen is better for larger omnichannel brands expanding across countries and channels. |

| Dispute management | Adyen and Stripe | Adyen offers real-time dispute tools, chargeback analytics, and dynamic 3D Secure. Stripe offers programmable dispute handling, which is useful for developer-led businesses. |

| Feature-rich free plan | Helcim and Square | Helcim includes no monthly fee, interchange-plus pricing, invoicing, subscriptions, CRM, inventory, and ecommerce tools. Square includes free POS tools, invoicing, reporting, digital receipts, and ecommerce features. |

For most new and low-volume businesses, ease of onboarding and free built-in tools will matter most, which makes Square and PayPal strong starting points. Businesses with more technical needs, larger payment volume, or international growth plans should compare Stripe and Adyen more closely, while cost-conscious B2Bs should pay close attention to Helcim’s included tools and pricing model.

Also read: 7 Best Merchant Services for 2025