Stripe is one of the most powerful developer-first payment platforms available. But it’s not always the best fit, especially for businesses that want simpler setup, built-in POS tools, lower interchange-based pricing, high-risk approval support, or more hands-on customer service. Some businesses may also need a different model altogether, such as a full-service merchant account or a merchant of record (MoR) provider that handles global tax and compliance responsibilities in addition to payment processing.

I compared the best Stripe alternatives and competitors in 2026 based on pricing, ease of use, multichannel payment tools, integrations, customer support, and user reviews to help businesses choose the right payment processor. Here are my top seven picks:

| Best for | Starting price per month | |

|---|---|---|

| Square | Best overall Stripe alternative | $0 |

| PayPal | Payment flexibility | $0 |

| Shopify Payments | Ecommerce | $5 |

| Helcim | Interchange pricing | $0 |

| CardX | Zero credit card processing | $29 |

| PaymentCloud | High-risk merchants | $10 |

| FastSpring | SaaS/merchant of record | $0 (revenue-share pricing) |

- Accept payments globally from one all-in-one platform

- Support payment needs across multi-country business operations

- Simplify payment acceptance for growing global teams

- Built for businesses that need flexible international payment options

My recommendations for the best free merchant account are based on more than three years of evaluating fintech and POS software and hardware across different industries and business types.

I evaluated Stripe alternatives using 27 payment-processing data points across pricing, hardware, online payments, POS tools, integrations, ease of use, support, and user reviews. When possible, I tested signup flows, dashboards, mobile payment tools, and product demos to compare how each provider works for small businesses, ecommerce sellers, SaaS companies, and high-risk merchants.

Best Stripe alternatives in 2026

Although Stripe is an excellent payment processor for online businesses, it may not be the best option for those needing a “plug-and-play” option or an easy-to-use multichannel point-of-sale (POS) system.

Below is a quick comparison of my recommended Stripe alternatives:

Provider

Payment Software score

Online rate

In-person rate

Merchant account type

Standout limitation

4.13

Starts at $99/month for some tools

Starts at $99/month

Surcharging provider

Narrow use case

*PSP: Payment Services Provider

For this list, I considered what would be essential for ecommerce businesses and online entrepreneurs. I added reputable providers known for their ease of use and customer satisfaction to the list for further analysis. I then evaluated each solution based on features, usability, integration capabilities, customization options, mobile access, and other relevant functionalities.

Finally, I curated a comprehensive list based on the previously stated factors, ensuring readers have the tools to make informed decisions.

I created an algorithm to calculate, based on many factors in the categories below, to calculate star ratings:

- User reviews: I considered user reviews from third-party software platforms Capterra, G2, and Software Advice in the overall score. These review sites offer real-world experience from actual users and are significant in bridging the gap between what providers present and what are delivered to their clients.

- Pricing: Providers with no setup costs, transparent pricing, and low processing fees received the highest scores. I also considered ongoing and hardware costs, which may matter for businesses looking for an omnichannel solution.

- Hardware: Although I mainly evaluated these providers for e-commerce businesses and online entrepreneurs, I also looked at hardware options for each provider since some businesses looking for Stripe alternatives do so for easier in-person payment processing with their online payment solution. Among the factors I considered are durability, ease of setup, and design of the devices.

- Payment features: Some of the important features of an online payment processor that I considered in my rating are the availability of different payment methods, ecommerce integrations, chargeback management, and developer tools.

- Support and reliability: Customer support is a crucial consideration when choosing an online payment processor, especially for online businesses. I also looked at security and system reliability, equally important when running a digital business.

- User experience: The ease of user experience, from sign-up and onboarding to growing the business, is an important consideration when choosing a payment solutions partner. I looked at the application process, contract terms, ease of use, and scalability.

What is Stripe, and who is it best for?

Stripe is a payment processing platform that combines a payment gateway, merchant services, subscription billing, and fraud prevention tools into a single system. It enables businesses to accept online payments, manage recurring billing, support global currencies, and integrate payments directly into websites and apps.

Unlike traditional full-service merchant account providers that assign a dedicated merchant account after underwriting, Stripe operates under a payment service provider (PSP) model. This means businesses can sign up quickly and begin accepting payments almost immediately, but accounts are monitored through automated risk systems rather than individual underwriting from the start.

Stripe works especially well for:

- SaaS and subscription-based businesses

- Marketplaces and platforms needing split payments

- Companies building custom checkout flows or embedded payments

- Businesses expanding internationally with multi-currency support

Its strength is flexibility. Stripe offers robust APIs, prebuilt components, and advanced billing tools that allow businesses to design highly customized payment experiences.

Stripe may be less suitable for:

- Businesses that prefer a fully underwritten, traditional merchant account

- Merchants operating in high-risk industries

- Companies that want dedicated account management

- Businesses seeking transparent interchange-plus pricing

In these cases, a traditional merchant account provider, omnichannel POS system, or merchant-of-record solution may be a stronger alternative.

Stripe, Square, and PayPal operate as payment gateways/payment service providers (PSPs). They process payments, but your business remains the legal merchant of record. This means you are responsible for tax compliance, chargebacks, fraud liability, and regulatory requirements.

A merchant of record (MoR) provider, such as FastSpring, acts as the legal seller for payment purposes. The MoR handles global tax calculation and remittance, compliance, and much of the financial liability associated with transactions.

You may consider a merchant of record if you:

- Sell SaaS or digital subscriptions internationally

- Need automated VAT/GST compliance

- Want to reduce regulatory and chargeback risk

- Prefer outsourcing tax and payment complexity

If you want full control and customization, a gateway like Stripe may be ideal. If simplifying global compliance is a priority, an MoR model may be a better fit.

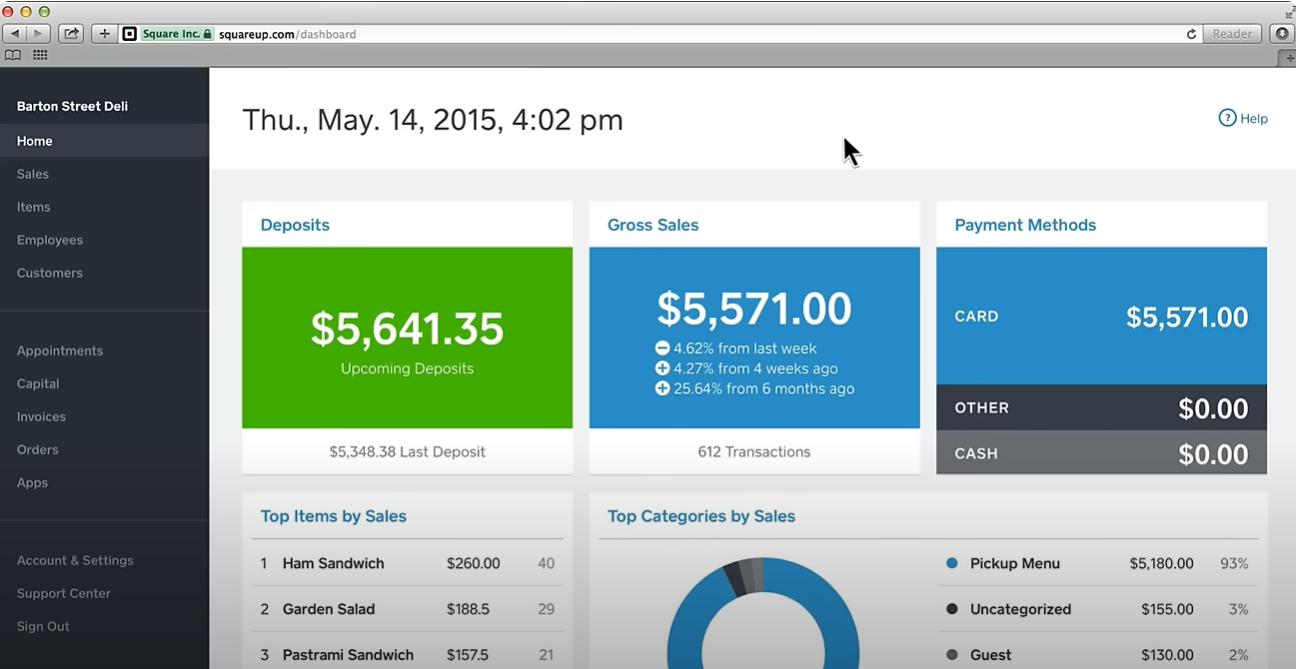

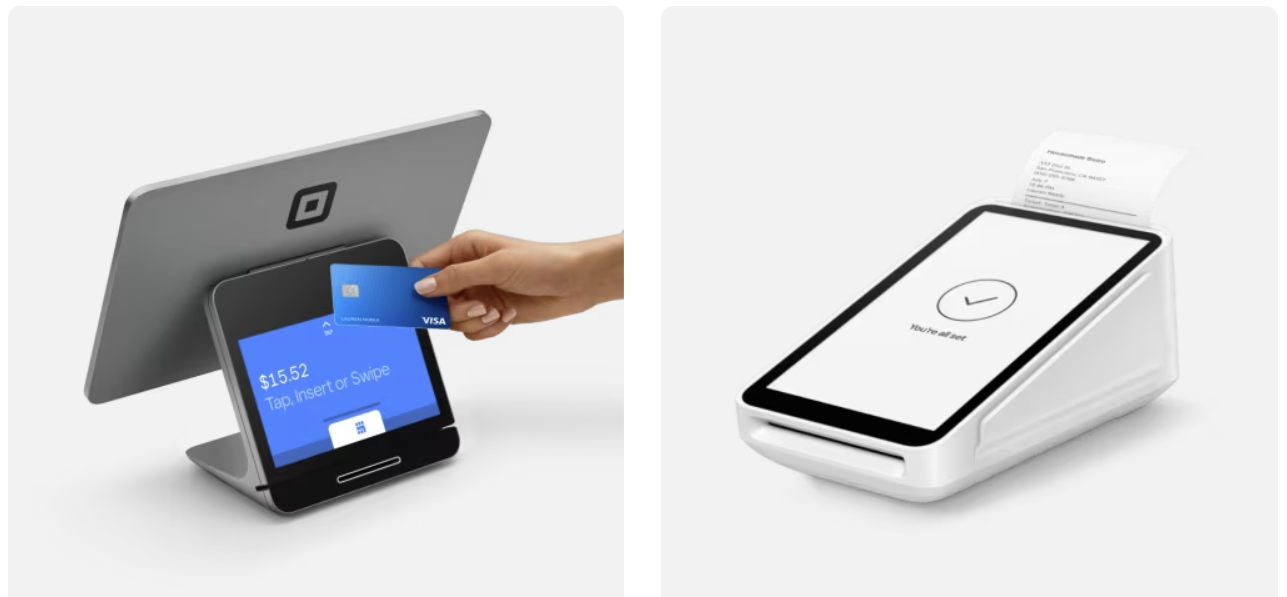

Square: Best overall Stripe alternative

Overall Score

4.34/5

Pricing

4.25/5

Hardware

4.5/5

Features

4.17/5

Support and reliability

3.75/5

User experience

4.69/5

User scores

4.67/5

Pros

- No monthly fees

- Omnichannel payment processing tools

- Easy to set up

Cons

- Payments exclusive to Square POS

- Limited support for cross-border sales

- Developer-based solutions only for enterprise accounts

Why I chose Square

Square is an all-in-one POS system that supports in-person, online, and mobile payments from a single platform. With no upfront software cost and plug-and-play hardware, it’s especially appealing to startups and small businesses that want a quick, easy setup. Square also integrates with major ecommerce platforms, making it a practical option for omnichannel sellers.

Its main limitation is ecosystem lock-in. Businesses must use Square’s POS software and add-ons, and it doesn’t offer the same level of open API customization as Stripe unless you move to enterprise plans.

Stripe vs Square

Stripe is ideal for online-first businesses that need advanced customization, subscription tools, and global payment support. Square is better for merchants that want a ready-to-use POS system with built-in hardware and minimal technical setup.

Choose Stripe for developer flexibility and international ecommerce. Choose Square for simplicity and integrated in-person selling.

Read more: Stripe vs Square

What users think of Square

Users highlight Square’s ease of use, quick setup, and all-in-one POS capabilities as major advantages, especially for small businesses. Many also appreciate the free plan and built-in tools. On the downside, some users report account stability issues, including payment holds, and say customer support can be inconsistent.

- Seamless omnichannel payment solution: Square’s strongest feature is its omnichannel capability, which makes it easy and convenient for businesses that sell online and at physical locations. Both online and in-store systems sync, making it easy to track sales, inventories, and transactions.

- Free basic plan: Whether you need an online payment solution or a physical POS system, you can start and use Square with zero costs. Square’s website builder is free to use, it offers a free magstripe reader, and it supports Tap to Pay on iPhone and Android devices. These inclusions mean you can start accepting payments without upfront payment.

- Add-on tools to scale up: While Square makes it easy for startups and small businesses to start accepting payments, it also provides growing businesses with various tools and options for scaling up. Aside from the free POS software and website builder, it also comes with free invoicing, a virtual terminal, social selling, and a team management system. Businesses may also create a loyalty program for their customers, offer subscription plans, and sell gift cards.

| Square Plans | Free Plan | Plus Plan | Premium Plan |

|---|---|---|---|

| Monthly fee | $0 | $49 | $149 |

| Online transaction fee | 3.3% + 30 cents | 2.9% + 30 cents | 2.9% + 30 cents |

| Keyed-in transaction fee | 3.5% + 15 cents | 3.5% + 15 cents | 3.5% + 15 cents |

| In-person transaction fee | 2.6% + 15 cents | 2.5% + 15 cents | 2.4% + 15 cents |

PayPal: Best for payment flexibility

Overall Score

4.21/5

Pricing

4.25/5

Hardware

4.25/5

Features

4.17/5

Support and reliability

3.33/5

User experience

4.69/5

Average User Review Scores

4.6/5

Pros

- Widely available and easy online checkout integration

- Well-known and trusted by consumers

- Easy to use

Cons

- Complicated pricing structure

- Extra fee for virtual terminal

- Account holds

Why I chose PayPal

PayPal is one of the most recognized online payment platforms, with over 400 million active users worldwide. It allows businesses to accept payments through credit and debit cards, PayPal and Venmo accounts, and alternative payment methods, all with simple website integration.

I recommend PayPal as a Stripe alternative for its ease of setup and strong consumer trust. Many ecommerce platforms offer one-click PayPal integration, making it quick to add at checkout. Its brand recognition can also help improve buyer confidence and conversion rates.

However, PayPal’s pricing can be complex, and certain tools, such as the virtual terminal, come with additional fees.

Stripe vs PayPal

Stripe offers more customization and developer flexibility, making it better for businesses building tailored checkout flows or managing complex subscription models.

PayPal is stronger for ease of use and brand recognition. It requires less technical setup and is widely trusted by consumers, which can help increase conversions. Choose Stripe for advanced customization; choose PayPal for simplicity and built-in buyer trust.

Read more: Stripe vs PayPal

What users think of PayPal

Users value PayPal for its widespread recognition, ease of integration, and the trust it builds with customers at checkout. Many businesses say it helps improve conversion rates. However, some users find the pricing structure confusing and report issues with account holds, disputes, and slow customer support resolution.

- Wide and easy integration: PayPal is simple and easy to use, and the best part is that it provides integration with almost any online platform. Many ecommerce platforms already offer a one-click PayPal integration — with this feature, you only need to provide your PayPal account details and toggle it on to make it an available payment method on your website.

- Cryptocurrency payment processing: PayPal is one of two providers on this list that offers cryptocurrency payment processing. Online businesses that want to accept cryptocurrencies will find PayPal an easy and suitable payment processor option.

- Buy Now, Pay Later (BNPL) options: PayPal is the only provider on this list that offers a native buy now, pay later option. Other providers that have this option, including Stripe, partner with BNPL apps.

- PayPal online checkout fee: 2.99% + 49 cents

- PayPal expanded online checkout fee: 2.89% + 29 cents

- Standard PayPal checkout fee: 3.49% + 49 cents

- Standard Venmo payments: 3.49% + 49 cents

- Cross-border fee: +1.5%

In-person transactions:

- POS option: $0 PayPal POS

- In-person fees: 2.29% + 9 cents

- QR payment: 2.29% + 9 cents

PayPal applies different rates based on how the merchant processes credit card payments. Find the complete list of PayPal business fees here.

Shopify Payments: Best Stripe alternative for ecommerce

Overall Score

4.16/5

Pricing

3.5/5

Hardware

4.25/5

Features

4.17/5

Support and reliability

4.17/5

User experience

4.38/5

Average User Review Scores

4.5/5

Pros

- Full integration with Shopify platform

- No Shopify Payments transaction fee for higher Shopify plans (card transaction fee still applies)

- More mobile payment options compared to Stripe

Cons

- Only available on Shopify

- Requires at least a Shopify Basic ecommerce plan for waived transaction fee

- Limited virtual terminal functionality

Why I chose Shopify Payments

Shopify Payments is Shopify’s built-in payment processor, allowing merchants to accept credit card payments directly within the Shopify dashboard. Because it’s fully integrated, businesses can manage products, orders, and payments in one place without setting up a third-party gateway.

I recommend Shopify Payments for businesses already using Shopify. It eliminates additional transaction fees charged for third-party processors on most plans and ensures seamless compatibility with Shopify’s tools and POS system. Merchants also benefit from 24/7 Shopify support.

The main drawback is platform lock-in; Shopify Payments is only available to Shopify users, so switching platforms would require changing payment processors.

Stripe vs Shopify Payments

Stripe offers greater flexibility and can be used across multiple ecommerce platforms. It’s better suited for businesses that want customization or aren’t committed to Shopify.

Shopify Payments is ideal for merchants fully invested in the Shopify ecosystem. It simplifies setup, reduces extra platform fees, and keeps everything centralized. Choose Stripe for flexibility across platforms; choose Shopify Payments for seamless Shopify integration.

What users think of Shopify Payments

Users appreciate Shopify Payments for its seamless integration with the Shopify platform and the convenience of managing everything in one dashboard. Many highlight the absence of extra transaction fees as a major benefit. However, some users note limited flexibility outside the Shopify ecosystem and report occasional payout delays or account review holds.

- Waived transaction fees: If you are already using Shopify as your ecommerce platform, switching to Shopify Payments gives you the advantage of waived transaction fees (which range from 0.5% to 2% when using third-party payment processors). Powered by Stripe, Shopify Payments gives you the same reliability and security — without the additional cost.

- Hardware for in-person selling: Like Square, Shopify Payments offers seamless omnichannel selling through its available POS devices.

- 24/7 customer support: Among Shopify’s strongest features is its 24/7 customer support, which extends to any issues or concerns specific to Shopify Payments.

Although there are no monthly fees for using Shopify Payments, you will need to sign up for a Shopify plan.

| Shopify Ecommerce Plan | Basic | Shopify | Advanced |

|---|---|---|---|

| Monthly Fee | $39/month | $49/month billed annually ($65 monthly) | $299/month billed annually ($399 monthly) |

| Online Transaction Fee | 2.9% + 30 cents | 2.6% + 30 cents | 2.4% + 30 cents |

In-person transactions:

- POS options

- Starter: without ecommerce $5

- Retail: with ecommerce $89

- Transaction fees: 2.6% + 10 cents or 5%

Helcim: Best Stripe alternative for interchange pricing

Overall Score

4.13/5

Pricing

4.75/5

Hardware

4/5

Features

3.75/5

Support and reliability

3.75/5

User experience

4.38/5

Average User Review Scores

4.17/5

Pros

- Interchange-plus pricing

- Automatic volume discount

- Free access to all payment tools

- Built-in surcharging with Fee Saver

Cons

- Add-on transaction fee for AMEX cards

- Requires merchant account approval

Why I chose Helcim

Helcim is a traditional merchant account provider that uses interchange-plus pricing instead of flat rates. With a fixed markup and automatic volume discounts, businesses can benefit from lower effective processing costs as they grow.

In addition to transparent pricing, Helcim includes built-in tools such as invoicing, subscription billing, a virtual terminal, CRM features, and Level 2/3 data support at no extra cost. Its browser-based Payment Extension also allows businesses to embed Helcim’s secure payment tools directly into compatible third-party software without major workflow changes.

Helcim is a strong Stripe alternative for businesses prioritizing cost transparency, B2B processing optimization, and long-term savings.

Stripe vs Helcim

Stripe uses flat-rate pricing and offers extensive APIs and integrations, making it ideal for highly customized online businesses.

Helcim’s interchange-plus model can result in lower overall costs, particularly for higher-volume or B2B merchants. It also provides a fully underwritten merchant account, which may offer greater account stability compared to Stripe’s aggregated model.

Choose Stripe for developer flexibility and global integrations. Choose Helcim for transparent pricing and potential cost savings as your volume increases.

What users think of Helcim

Users frequently praise Helcim for its transparent interchange-plus pricing, lack of hidden fees, and strong value for growing businesses. Many also highlight its helpful customer support and all-in-one payment tools. On the downside, some users mention the approval process can take longer than with PSPs like Stripe, and that certain features may feel less advanced or customizable.

- Interchange-plus rates with automatic volume discounts: Helcim’s processing rates are among the cheapest processing rates on this list. Besides offering interchange-plus rates instead of flat rates, it also offers automatic volume discounts based on your monthly transaction volume.

- Option to pass on credit card fees to customers: The Helcim Fee Saver is a feature that Helcim merchants can enable. This tool lets merchants pass on the credit card fees to their customers, a practice called surcharging.

- Customer management portal: Helcim’s customer management portal is robust and does not incur any additional fees. It helps to effectively manage customer lists and track profiles and transaction history.

| Monthly Transaction Volume | Online and Keyed-In Transaction RatesInterchange + | In-Person Transaction RatesInterchange + |

| $0-$50,000 | 0.50% + 25 cents | 0.40% + 8 cents |

| $50,001-$100,000 | 0.45% + 25 cents | 0.35% + 8 cents |

| $100,001-$500,000 | 0.35% + 25 cents | 0.25% + 8 cents |

| $500,001-$1,000,000 | 0.25% + 25 cents | 0.20% + 8 cents |

| $1,000,001 up | 0.15% + 25 cents | 0.15% + 8 cents |

CardX: Best Stripe alternative for zero credit card processing

Overall Score

4.13/5

Pricing

4.75/5

Hardware

3.25/5

Features

4.38/5

Support and reliability

4.4/5

User experience

4.06/5

Average User Review Scores

3.75/5

Pros

- Auto surcharging

- Fully compliant credit surcharging

- Auto-detection of debit and credit cards

Cons

- Limited invoicing and POS integrations

- Does not accept cross-border payments

- Underwriting requires at least $5,000 in monthly sales

Why I chose CardX

CardX is designed for businesses that want to eliminate credit card processing costs through compliant surcharging. Instead of absorbing processing fees, merchants can pass those fees to customers paying by credit card, significantly reducing payment expenses.

It handles the required card brand registrations and ensures compliance with federal and state surcharging regulations. Businesses can accept payments online through its Lightbox integration, via virtual terminal, or in person using compatible card readers. Merchant training is also included to help ensure proper implementation.

CardX is best suited for businesses focused on cost control and compliance rather than advanced integrations or POS features.

Stripe vs CardX

Stripe uses a traditional flat-rate pricing model where merchants absorb processing fees. CardX takes a different approach by enabling compliant surcharging, allowing businesses to offset most credit card processing costs.

Choose Stripe for customization and broader integrations. Choose CardX if your primary goal is reducing or eliminating credit card processing expenses through a regulated surcharging model.

What users think of CardX

Users appreciate CardX for helping eliminate credit card processing costs through compliant surcharging and for its hands-off setup. Many also value its focus on regulatory compliance and guided onboarding. However, some users note limited integrations and features compared to traditional processors, and say it’s not ideal for businesses needing advanced POS or ecommerce tools.

- Auto surcharging: CardX offers auto surcharging, allowing businesses to pass on credit card transaction fees to their customers in 48 states and the District of Columbia.

- Fully compliant with federal and local regulations: Businesses will need to register with card brands and comply with requirements set by these brands to pass on fees. CardX makes surcharging easy by completing the registration on behalf of businesses and making sure its payment solution is compliant with relevant rules and regulations.

- Merchant training: Since surcharging differs from standard card payment processing, CardX offers a merchant training session to ensure you and your employees learn the system and the required protocols for surcharging.

- Virtual terminal+Online credit card processing: Starts at $99/month

- In-person credit card processing: Starts at $99/month

- Debit card processing: 1.25% + $0.25

PaymentCloud: Best Stripe alternative for high-risk merchants

Overall Score

4.1/5

Pricing

3.75/5

Hardware

3.75/5

Features

3.75/5

Support and reliability

4.58/5

User experience

4.06/5

Average User Review Scores

4.7/5

Pros

- Accepts high-risk merchants

- High approval rate

- Offers cryptocurrency payment processing

Cons

- Longer application and approval process

- Extra fee for virtual terminal

- Pricing is not publicly disclosed

Why I chose PaymentCloud

PaymentCloud is a merchant account provider specializing in high-risk and hard-to-place businesses. It supports industries such as CBD, supplements, adult products, and other verticals that are often declined by mainstream payment processors.

In addition to credit card processing, PaymentCloud offers ACH and eCheck payments, fraud prevention tools, and chargeback management support tailored to higher-risk environments. Its higher approval rate makes it a practical option for businesses that may struggle to qualify with providers like Stripe.

While pricing is customized and the approval process can take longer, PaymentCloud provides more flexibility for businesses operating in regulated or high-risk industries.

Stripe vs PaymentCloud

Stripe uses an aggregated merchant model with automated risk monitoring, which can lead to account freezes or declines for high-risk businesses.

PaymentCloud works with a network of acquiring banks to place higher-risk merchants and provides more individualized underwriting. Choose Stripe for fast setup and standard-risk businesses. Choose PaymentCloud if your industry faces higher approval barriers and requires specialized risk support.

What users think of PaymentCloud

Users praise PaymentCloud for its high approval rates and ability to support high-risk businesses that struggle to get accepted elsewhere. Many also highlight its responsive, hands-on customer support. However, some users note that pricing is less transparent and can vary widely, and that the application and underwriting process can take longer than with standard providers.

- High-risk merchant support: PaymentCloud is one of the top payment service providers for high-risk merchants. If your business is in a medium- and high-risk industry, you will not be accepted by most payment processors, including Stripe. PaymentCloud, on the other hand, supports businesses in these industries with a high approval rate.

- Cryptocurrency payment processing: Aside from supporting high-risk merchants, another uncommon feature with PaymentCloud is its cryptocurrency payment processing. Businesses that would like a Bitcoin checkout option for Bitcoin and other cryptocurrencies such as Ethereum, Litecoin, Tether, and XRP will find PaymentCloud a suitable option.

- Chargeback and fraud protection: PaymentCloud places heavy importance on chargeback and fraud protection, especially since it caters to high-risk businesses. It has partnered with a specialized chargeback protection provider to help detect, track, and resolve disputes.

Read more: 6 Best High Risk Merchant Account Providers

PaymentCloud rates depend on your business’s risk assessment. High-risk merchants are assigned higher rates than mid- and low-risk businesses.

- Monthly fee: $10-$45

- Low-risk transaction fee: 2%-3.1%

- Mid-risk transaction fee: 2.3%-3.4%

- High-risk transaction fee: 2.7%-4.3%

- Virtual terminal fee: $15-$45 per month

FastSpring: Best for SaaS and as merchant of record

Overall Score

3.83/5

Pricing

4.5/5

Hardware

3.33/5

Features

3.28/5

Support and reliability

4.58/5

User experience

3.75/5

Average User Review Scores

4.3/5

Pros

- Merchant of record model (handles global tax and compliance)

- Built-in subscription and SaaS billing tools

- Chargeback and fraud liability coverage

- Supports international currencies and payment methods

Cons

- Revenue-share pricing can be higher than Stripe’s flat rates

- Slower payout timelines

- No POS or in-person payment support

Why I chose FastSpring

FastSpring is a merchant of record (MoR) provider built for SaaS companies and digital product sellers. Unlike Stripe, where your business remains responsible for tax compliance and chargebacks, FastSpring becomes the legal seller of record. It handles global VAT/GST calculation and remittance, regulatory compliance, and chargeback liability on your behalf.

I included FastSpring because many SaaS businesses looking for Stripe alternatives are trying to reduce international tax complexity and compliance risk, not just change payment processors. FastSpring simplifies cross-border selling with localized checkout, multi-currency support, and built-in subscription management.

It’s best suited for digital and subscription-based businesses expanding globally.

Stripe vs FastSpring

Stripe provides flexible APIs and customization, but your business remains responsible for global tax compliance and financial liability.

FastSpring operates as a merchant of record, taking on tax collection, remittance, and much of the compliance burden. Choose Stripe for developer control and customization. Choose FastSpring if reducing global tax and regulatory complexity is a priority.

What users think of FastSpring

Users value FastSpring for simplifying global sales, particularly its handling of taxes, compliance, and chargebacks under the merchant of record model. Many SaaS businesses appreciate its built-in subscription tools and international payment support. However, some users mention higher overall costs due to revenue-share pricing and note that payouts can be slower compared to traditional payment processors.

- Merchant of record model: FastSpring assumes responsibility for global tax compliance, fraud management, and regulatory obligations, allowing businesses to focus on product and growth rather than backend financial complexity.

- Subscription management: Built-in tools support recurring billing, upgrades, downgrades, usage-based pricing, and subscription analytics without additional add-ons.

- Global payments support: Accepts multiple currencies and localized payment methods to improve international conversion rates.

- Chargeback and fraud management: Advanced fraud prevention tools and dispute handling are included, reducing merchant liability.

FastSpring uses a revenue-share pricing model rather than flat transaction rates.

- No monthly fee

- Custom transaction rates based on volume and business model

- No chargeback fees (FastSpring assumes liability under MoR model)

Pricing is customized and typically negotiated based on annual revenue and geographic distribution of sales.

Why is Stripe so popular?

Stripe was launched in 2011 as a developer-first platform for building secure, seamless online payment processing integrations. As of June 2023, Stripe powers payments on over 1.2 million live websites across 135 currencies in 45+ countries, including big names like Shopify, Xero, and Amazon.

Businesses of all sizes turn to Stripe for a number of reasons:

- Unlike other payment services, Stripe’s developer-based customization and integration tools are available to anyone. Users will find a well-documented list of APIs, SDKs, and code samples on the provider’s website to create their own custom checkouts, subscriptions, app integrations, and mobile apps.

- Since its launch, Stripe has also developed a long list of business products, including embedded finance, payment orchestration, and revenue and finance automation.

- Stripe provides small businesses with a free merchant account without the lengthy application process, no long-term contract, and simple, transparent pricing.

- Large-volume companies can avail of interchange plus rates to help maximize savings.

Advantages: Why use Stripe

Stripe’s strength lies in its ability to provide nearly unlimited customization possibilities for online payment processing.

Robust online payment customization tools

Use Stripe if your business runs primarily through a website and is looking to customize checkout with useful automations such as identity verification, address autocomplete, and card brand identification.

Supports international payments

Use Stripe if your business accepts international payments through a website. Stripe offers ready integration with numerous local banks and payment methods from 45+ countries.

Strong payment security measures

Use Stripe to ensure payment security and minimize chargebacks. Stripe’s strategic partnership with Visa allowed Stripe to harness Visa’s tokenization tools. Today, Stripe is well known for its fraud detection and management features using machine-learning algorithms to flag suspicious transactions.

Wide range of integrations

Use Stripe if your current business goal is to grow through strategic integrations. Stripe provides 660 third-party integrations and 450 platform extensions for everything from payment optimization to finance automation.

Also read: How to Accept Payments Online

Disadvantages: When to use a Stripe alternative

While Stripe has taken strides to provide more ease of use and multichannel support for payment processing, Stripe competitors continue to be a better choice for several reasons:

Limited payment method for pre-built mobile payment app

Use a Stripe alternative if you intend to accept swipe, EMV chip, and other NFC-based payments. I had a chance to try out Stripe’s mobile payment app, Stripe Dashboard, and in-person payment processing limited to Tap-to-pay (which costs an additional 10 cents per authorization) and manual card entry. Stripe’s mobile credit card reader can only be configured to use with paid third-party Stripe apps.

Read more:Best mobile payment processors

Payment terminal requires customization

Use a Stripe alternative if you prefer an out-of-the-box POS terminal. While Stripe Terminal comes with pre-built elements for payment processing, it does not include complete POS software. You will still need custom integration to add your current POS application and integrate it with the tools included in the Stripe Terminal.

Limited no-code payment processing options

Use a Stripe alternative if you need a quick and painless payment setup. In my experience creating a Stripe merchant account, I’ve found it easy to get lost during the account setup stage, even with the guide. You get no-code payment links and ecommerce website checkout pages, but everything else will require some level of coding skill just to add small customizations, including virtual terminal functions.

How to choose the best Stripe alternatives

When choosing a Stripe alternative, you will need to take your business goals into consideration.

Consider other payment processors, such as Stripe, if your goal is to improve features you currently get from Stripe but lack in-house upgrade options. Some examples are:

- Better rates for accepting international payments (Stripe currently charges 1.5% + 1% for currency conversion

- Free or more affordable use of invoicing and billing management tools (Stripe charges 0.4%-0.5% per paid invoice and 0.7% of the monthly billing volume)

- More established mobile app that can accept more mobile payment methods (Stripe Dashboard only supports tap-to-pay and manual card entry)

Read more: Best online payment processors

| Choose this Stripe alternative | If you need |

| Square | Online, in-person, and mobile payments in one system |

| PayPal | A recognizable checkout option with broad consumer trust |

| Shopify Payments | Native Shopify checkout and POS support |

| Helcim | Interchange-plus pricing and a dedicated merchant account |

| CardX | A compliant way to pass credit card fees to customers |

| PaymentCloud | High-risk merchant account support |

| FastSpring | Merchant of record support for SaaS and digital goods |

Check out other payment processors that differ from Stripe if your goal is fast setup and simple integrations to expand your payment channels. Examples include:

- Ease of use from out-of-the-box payment processing solutions instead of code-based setup and customizations

- Proprietary POS software pre-built into the standalone payment terminal instead of custom integration or as a mobile app instead of third-party Stripe apps

- Provider transaction fee discounts instead of just the standard card network interchange discount for qualified nonprofits

- Ready integration with surcharging programs/platforms

Once you have narrowed down your available options, you can begin looking into the costs. Start by comparing the estimated monthly fees for each Stripe competitor, then evaluate the overall value for money of each provider. If you are going to have to pay for services that you don’t need, then it’s best to look at other options.

FAQs

PayPal is Stripe’s biggest competitor in the online payments space. Not only is PayPal easy to set up and integrate with any ecommerce platform, but it is also the most trusted brand proven to boost online conversions, plus a more established mobile payment and POS app for better multichannel sales.

Square is the cheapest Stripe alternative for most small businesses because it has no monthly fee, includes free POS software, and supports online, in-person, mobile, and keyed-in payments. Helcim is also a strong low-cost option for businesses that want interchange-plus pricing and do not mind a longer merchant account approval process.

Shopify Payments is the best Stripe alternative for ecommerce businesses already using Shopify. It is built into the Shopify checkout, supports online and POS payments, and helps sellers manage orders, payments, and store operations from the same platform.

FastSpring is the best Stripe alternative for SaaS businesses that need merchant of record support. It handles payments, global tax compliance, subscriptions, and digital product transactions, making it a strong fit for software companies selling internationally.

PaymentCloud is the best Stripe alternative for high-risk merchants because it specializes in helping businesses that may not qualify for standard payment processors. It supports industries with higher chargeback risk, stricter underwriting needs, or more limited processor options.

Square is better than Stripe for businesses that want simple setup, built-in POS tools, and ready-to-use hardware. Stripe is better for developer-led businesses that need advanced online checkout customization, APIs, subscriptions, and global payment flexibility.

PayPal is better than Stripe for businesses that want a familiar checkout option with less technical setup. Stripe is better for businesses that need more control over checkout design, developer tools, subscription billing, and custom payment workflows.

FastSpring is the best merchant of record alternative to Stripe for SaaS and digital product businesses. Unlike Stripe, FastSpring acts as the legal seller for many transactions and can handle global tax calculation, remittance, compliance, and payment processing.