A nonprofit financial statement isn’t much different from a for-profit one. The terminology may vary slightly, but the overall structure, intent, and purpose remain the same — to show how funds are received, managed, and used.

Technically, a nonprofit financial statement is a formal record that summarizes an organization’s financial activities, including its revenues, expenses, assets, liabilities, and net assets. In this article, I’ll walk through what a nonprofit financial statement is, the main types of statements you’ll encounter, and how to read them effectively.

Featured partners

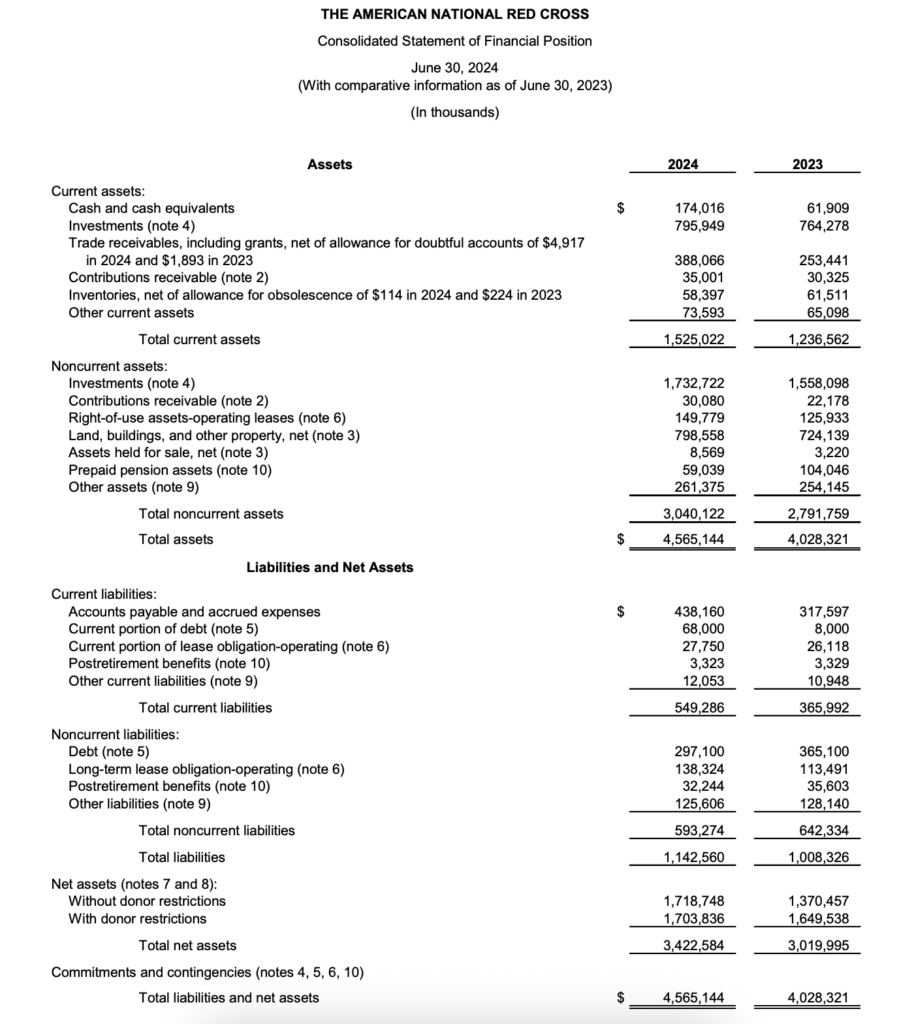

Statement of financial position

The “statement of financial position” might sound like a mouthful and a little too technical, but it’s simply the nonprofit version of a balance sheet. Don’t be thrown off if you see foreign companies use the same term. Under the International Financial Reporting Standards (the global counterpart of the US Accounting Standards Codification), the statement of financial position is actually their official name for the balance sheet.

The sample below is from the American National Red Cross. If you look at the title, it says “consolidated.” When you see a financial statement labeled as consolidated, it simply means it combines the financial results of a parent nonprofit and its affiliated entities into one report, giving a complete picture of the entire organization’s financial position.

Just like in a for-profit business, it shows three main components: assets, liabilities, and equity.

- Assets represent what the nonprofit organization owns or controls and can use to accomplish its mission.

- Liabilities represent what the organization owes to creditors or other parties.

The key difference lies in the equity part as nonprofits refer to equity as net assets. This net asset section is where things diverge from for-profit financials, as it reflects the unique way nonprofits categorize and track their funds.

Restricted and unrestricted net assets

In nonprofit accounting, net assets are divided into two categories: restricted and unrestricted. The distinction depends on whether donors place conditions on how or when the funds can be used.

Unrestricted net assets are the most flexible. They can be used for any purpose that supports the organization’s mission, such as covering operating costs or funding new programs without donor-imposed limitations.

Restricted net assets, on the other hand, come with specific donor instructions. These restrictions can be either temporary or permanent, depending on the donor’s intent:

- Temporary restrictions apply when funds must be used for a particular purpose or within a certain time frame. Below are examples of temporary restrictions:

- A $50,000 grant that must be spent by December 2026 to build a new community kitchen

- A donation given only for flood victims in any affected city in the US

- A $10,000 gift that must be used next summer to fund the “Bright Futures Youth Camp” in Denver, Colorado

- Permanent restrictions apply when the donor requires that the principal amount remain intact indefinitely, with only the income or investment returns available for use.

- A $1 million endowment fund where only annual interest earnings can support the nonprofit’s operations

- A scholarship fund intended to sponsor highly-qualified students who meet the GWA requirements

- A land conservation fund where the donor stipulates that the $250,000 must be used to acquire and permanently preserve a protected forest area, and that the property can never be sold, leased, or repurposed for non-conservation activities.

Restrictions must be clearly stated in the gift instrument, which is the formal document or agreement outlining the donor’s intent. This is where the donor specifies exactly how the funds can be used, whether for a particular purpose, within a set time frame, or to remain permanently restricted.

Looking for a nonprofit CRM solution? Check out our Nonprofit CRM Buyer’s Guide.

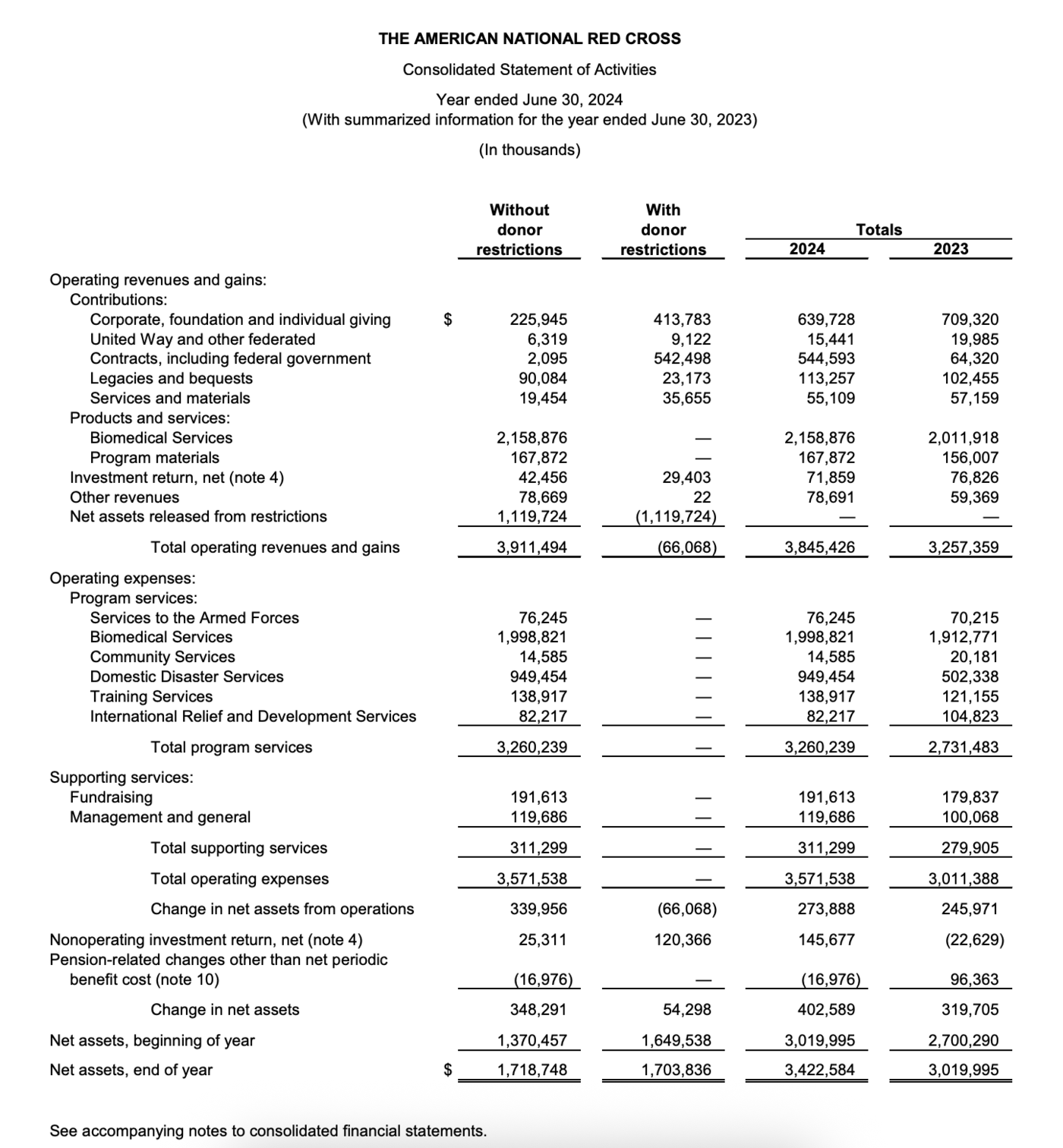

Statement of activities

The statement of activities is the nonprofit equivalent of an income statement. It reports how the organization’s revenues, expenses, and gains change over a specific period, showing whether total resources increased or decreased. Its main purpose is to present how funds were earned and spent during the year, essentially telling the story of how the nonprofit carried out its mission financially.

A key line to pay attention to is “net assets released from restrictions.” This shows the amount of donor-restricted funds that have met their purpose or time condition and are now available for general use. For example, if a donor gave money to build a community center and the project is completed, those funds move from the “with restrictions” column to the “without restrictions” column.

You’ll also notice that instead of showing net income, this statement reports the change in net assets. That’s because nonprofits don’t have owners or shareholders. Their goal isn’t profit, but stewardship.

So, “net assets” simply represents what remains after expenses, showing how much the organization has retained to continue its work.

Read more: Nonprofit Accounting Software Buyer’s Guide

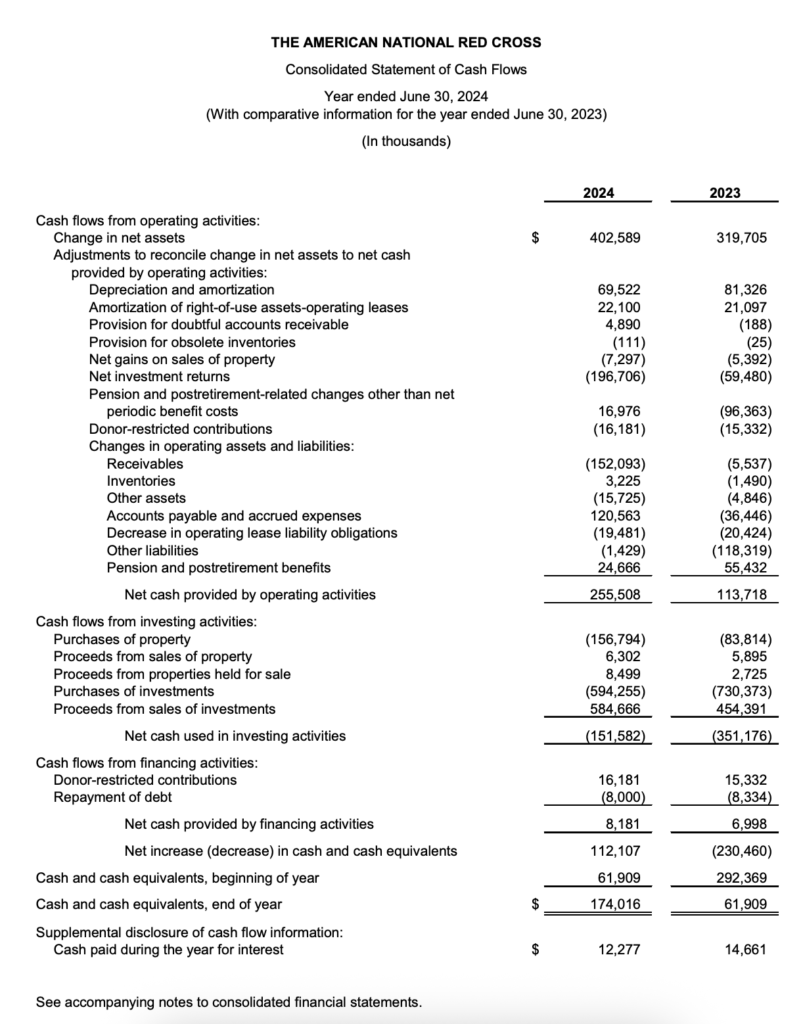

Statement of cash flow

The statement of cash flows for a nonprofit isn’t much different from that of a for-profit business. It shows how cash moves in and out of the organization during the year. The sample from the American Red Cross uses the indirect method, which is the most common approach because it’s easier to prepare using information from the statement of activities.

Here are the key components typically found in a nonprofit statement of cash flows:

- Cash flows from operating activities: This section shows the cash generated or used in the nonprofit’s daily work, like collecting donations, paying bills, and funding programs. Because the sample above uses the indirect method, this part doesn’t list every cash transaction. Instead, it starts with the change in net assets (the nonprofit version of profit) and adjusts it to show actual cash movement. Here’s why some items are added or deducted:

- Non-cash expenses like depreciation are added back because they reduce accounting income but don’t use any cash. For example, recording depreciation lowers net assets on paper, but no money actually leaves the bank.

- Non-cash gains (like gains from investments) are subtracted because they increase income but don’t bring in cash.

- Increases in current assets (such as receivables or inventory) are deducted because they represent cash that hasn’t been received yet. For instance, if donors promised money but haven’t paid, the nonprofit doesn’t have that cash yet.

- Decreases in current assets are added because they mean cash was collected.

- Increases in liabilities (like accounts payable) have been added because the nonprofit retained cash by delaying payment.

- Decreases in liabilities are deducted because paying off those obligations uses cash.

- Cash flows from investing activities: This includes buying or selling long-term assets such as buildings, equipment, or investments. It tells whether the organization spent money to grow its capacity or earned cash by selling assets.

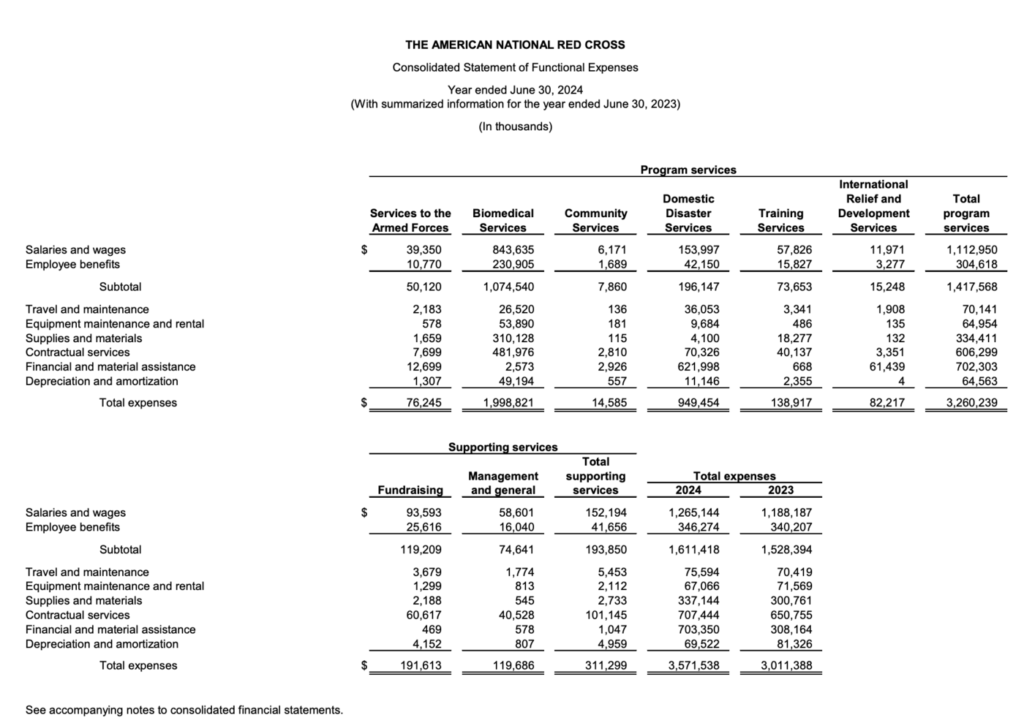

Statement of functional expenses

The statement of functional expenses is a financial report unique to nonprofits. It shows how a nonprofit spends its money, breaking down total expenses by both function (the purpose of the expense) and nature (the type of expense). Its main purpose is to provide transparency to donors, regulators, and the public, so that they can see exactly where the organization’s money goes.

The layout is intentional. Each column represents a major activity or function of the organization. There are two types:

- Program services: These are the activities that directly fulfill the nonprofit’s mission. Every dollar spent here supports the organization’s core programs or services like disaster relief, blood donations, or community outreach (as shown in the Red Cross example). High spending in this area is generally seen as a sign that the organization is effectively using funds for its intended purpose.

- Supporting services: These are necessary costs that keep the organization running but don’t directly carry out the mission. They include management and general expenses (like accounting, HR, and office operations) and fundraising expenses (like campaigns and donor communications). Although they don’t produce direct program outcomes, they’re essential for planning, compliance, and sustaining funding. Too high a percentage here can raise questions about efficiency, while too low may suggest underinvestment in infrastructure.

Each row lists the natural categories of expenses, such as salaries, travel, supplies, and depreciation. This format makes it easy to see not only how much was spent in total but also what types of costs make up each area of work.

Nonprofits are required to present this statement under US Generally Accepted Accounting Principles (GAAP). The Financial Accounting Standards Board (FASB) requires nonprofits to show expenses by both function and nature, either in the financial statements themselves or in the notes. This requirement promotes accountability and helps stakeholders assess whether the organization is spending resources effectively to fulfill its mission rather than on excessive administrative or fundraising costs.

Read more: Best Nonprofit Software

Nonprofit accounting software choices

Choosing the right nonprofit accounting software is about finding the right balance between functionality, flexibility, and simplicity. The ideal platform should help track restricted funds, manage grants, and produce required reports without overwhelming the team.

QuickBooks Online: Best general accounting software for multi-program nonprofit accounting

QuickBooks Online is one of the most widely used accounting platforms — cloud-based, user-friendly, and flexible enough to model nonprofit structures. It supports tracking through Classes, Locations, and Projects, making it easy to organize funds, programs, grants, and campaigns. It also integrates well with donation platforms and payroll tools, allowing nonprofits to manage contributions and expenses in one place.

Sage Intacct: Best for complex and multi-entity fund management

Sage Intacct is designed for advanced fund accounting and scales easily for larger nonprofits. It includes built-in nonprofit reports such as the Statement of Activities and Statement of Functional Expenses, along with strong grant, project, and multi-entity management tools. Its role-based controls and audit-ready dimensions make it ideal for organizations that manage restricted funds and need strict accountability.

Aplos: Best dedicated nonprofit accounting software

Aplos is built specifically for small to mid-sized nonprofits, offering native fund accounting, donor management, and online giving in one platform. Its interface aligns naturally with nonprofit reporting standards, helping users produce clear Statements of Activities and Functional Expenses without customization.