Key takeaways

Deciding when to use a payment gateway vs payment processor or when to use both comes down to a few factors. A payment gateway is a technology to encrypt payment data from the customer to your business. A payment processor is a service that authorizes payments from customers to businesses. They work in tandem, and small businesses likely need both, but you can usually get both from a payment processor. If all this seems confusing, keep reading for a more thorough explanation, use cases, and answers to frequently asked questions about payment gateways and payment processors.

What is a payment gateway?

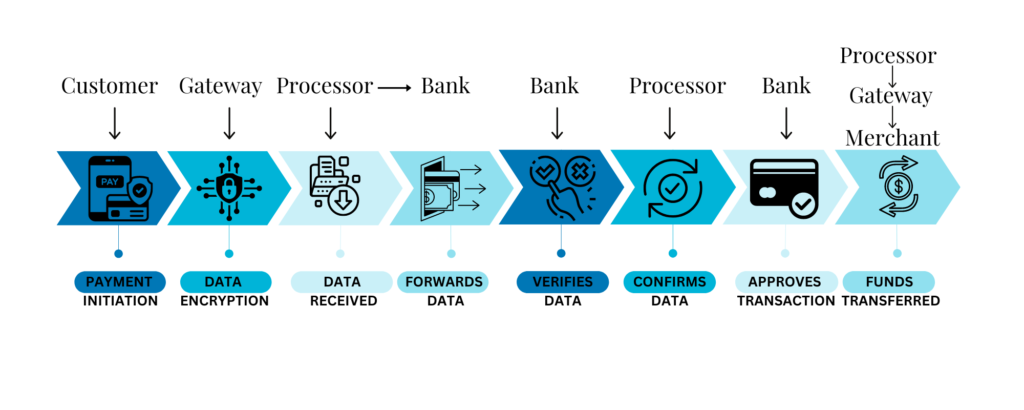

A payment gateway is responsible for encrypting and securing the data transmitted for payments. Services that provide a payment gateway tend to be the liaison between customers and payment processors. Once the payment data is secured, it’s “handed over” to a payment processor for authorization and fraud checks. Whether you sell goods or services in person, online, over the phone, or by mail (though the latter is less common these days), you need a payment gateway.

Types of payment gateways

There are four different types of payment gateways: hosted, self-hosted, API-hosted, and bank integration. A hosted payment gateway is most often found on ecommerce websites that redirect a customer to pay on a payment gateway’s website, like PayPal. It works, but it isn’t a seamless shopping experience. Bank-integrated payment gateways are similar, but the customer is directed to a bank’s website to enter payment details.

A self-hosted gateway is one of the most common ecommerce options in which you have a payment gateway that integrates with an online shopping cart. This keeps your customers on your site as they check out. An API-hosted payment gateway gives you more control over the look and feel of your checkout, but you won’t get the benefits of a third party’s security, and you need to have more technical know-how.

Examples of payment gateways:

- Authorize.net

- Stripe

- WorldPay

- PayPal

Read more: Stripe vs PayPal: Which is Better?

Read More: Square vs Paypal: Which Should You Choose in 2024?

What is a payment processor?

A payment processor is a service that is responsible for almost the entire payment transaction process. It works with a payment gateway to complete a card payment from a customer to a merchant, along with authentication and fraud checks through banks. Whenever a customer swipes, taps, or dips a debit or credit card into a physical POS, the process begins to ensure the account has the funds to cover the transaction and that the card belongs to the person who uses it.

Authentication

Cardholder details are encrypted by the payment gateway and then sent to authentication servers through the card network, such as Visa, Mastercard, or American Express. At this point, communication between the card network and the customer’s bank is necessary to check for sufficient funds.

Anti-fraud checks

To make sure no one is making an unauthorized purchase, a payment processor may require a customer to enter the billing zip code of their card or the card verification value (CVV) number, which is usually a three-digit (sometimes four-digit) number found on the back or front of their card.

Transaction fees

There’s always the cost of doing business. All payment processors charge transaction fees. The average range of fees isare 1.5% to 3.5% per transaction. These fees can be higher or lower depending on the type of business you run and the type of payment processor you choose.

Types of payment processors

If you run a high-risk business, such as a gun shop or a vape store, you may need to pay higher transaction fees with a high-risk payment processor. If you’re an established business that brings in a high volume of sales and you choose a merchant services provider (MSP), your fees will likely be variable and lower. Newer businesses have the best luck with aggregate payment processors such as Square or Stripe that charge flat-fee transaction rates rather than merchant accounts that provide variable fees.

Examples of payment processors:

- Square

- Stripe

- Helcim

- Payment Depot

- Shopify

Read more: Credit Card Processing Fees: Complete Guide

Read more: Ecommerce Payment Processing: The Complete Guide

Payment Gateway vs. Payment Processor

To be clear, there is no competition of payment processor vs payment gateway; you need both regardless of whether you run a brick-and-mortar store or you want to learn how to accept payments online. There’s no real all-in-one solution such as a payment processor gateway, but there are some payment processors that offer services that include a payment gateway.

Square and PayPal are great examples of payment aggregates. Both services charge merchants flat percentage rates for payments and provide a gateway, payment processor, and security. There’s no need to set up a merchant account with a bank to receive payment. However, what you pay in fees is likely higher with a service like these aggregates.

Read more: Best Credit Card Processing Companies

Differences

Although it’s common to see or hear the terms payment processor and payment gateway used interchangeably, they each play different roles in the transaction process. Here’s how payment gateways and payment processors differ:

| Payment gateway | Payment processor |

|---|---|

| Encrypts payment details | Authorizes and processes payments |

| Transmits data between all parties | Usually includes additional services such as fraud checks and chargebacks |

| Typically integrates with processors | Requires integration with payment gateway and merchant account |

Together, a payment processor and payment gateway securely and quickly process transactions. What the two services have in common is that integration is needed between the two, unless you choose an end-to-end payment service solution.

Integration

As mentioned earlier in this article, a payment gateway is the technology used to encrypt and transmit payment data, while a payment processor handles the authorization and movement of funds and detects fraud. There are third-party payment gateways you can use and integrate with a shopping cart system on your ecommerce website or with a POS system for the necessary security protocols, but you’ll still need a payment processor to handle transactions.

For the easiest payment solution, you may want to choose a payment aggregate in which you share a merchant account with other merchants. It’s quick and easy to get started with accepting payments. For a better rate on transaction fees, you need to apply for a dedicated merchant account and payment processor. This is a longer process for approval, and you may get the option to choose your own payment gateway.