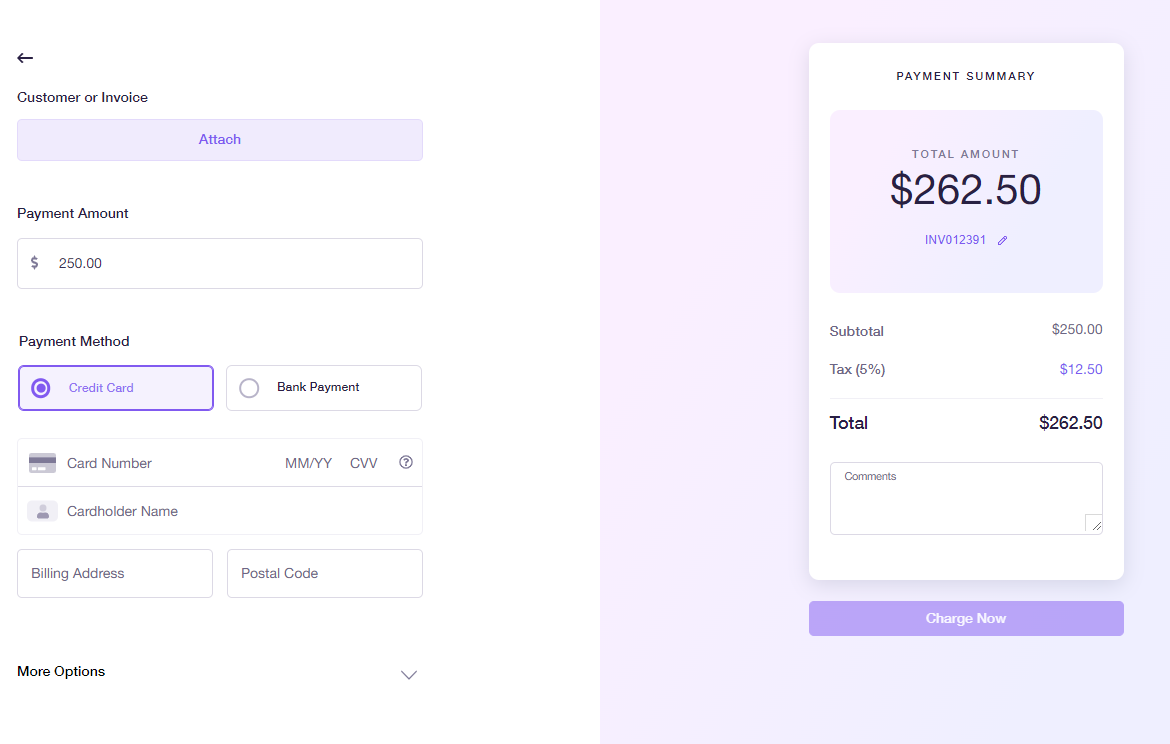

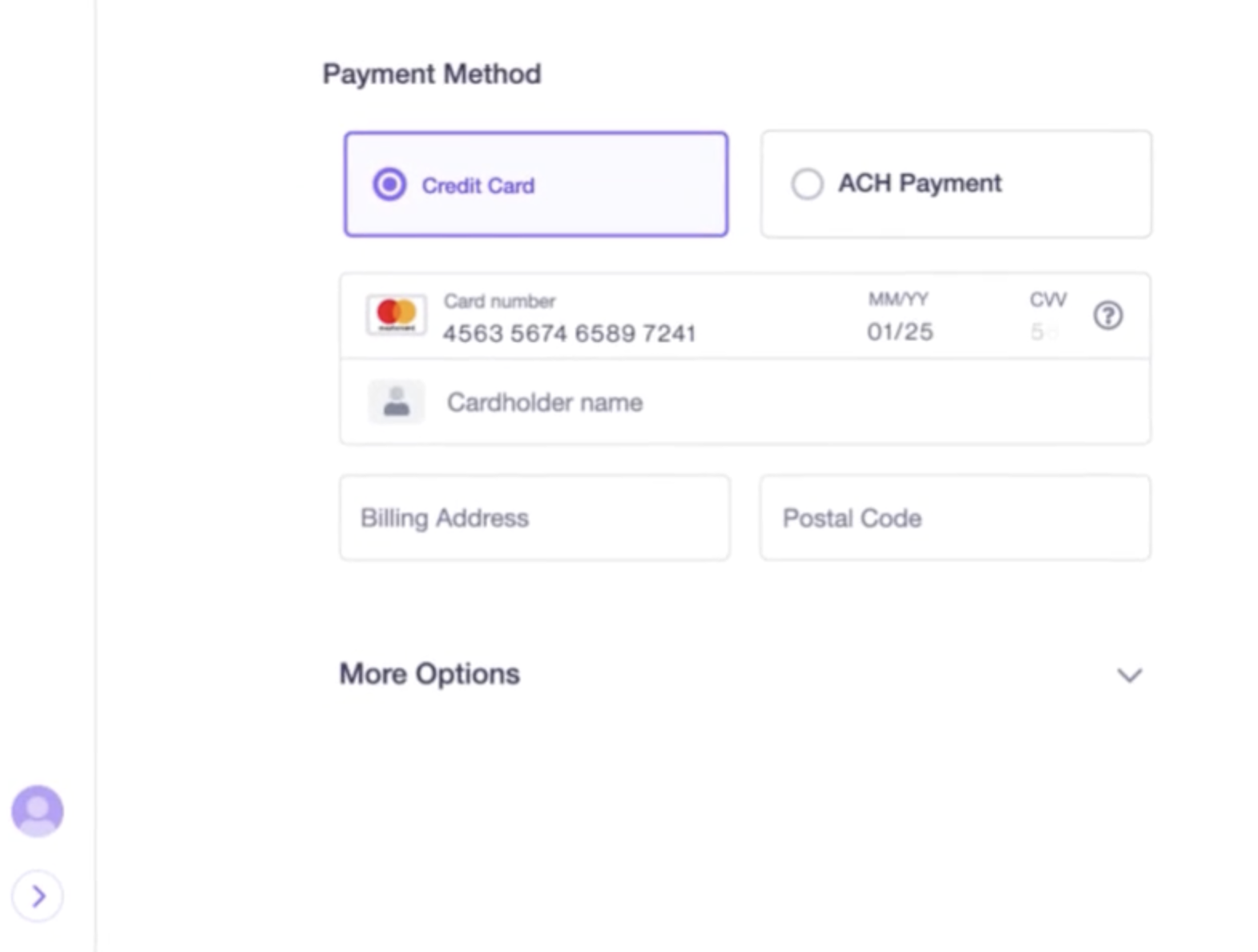

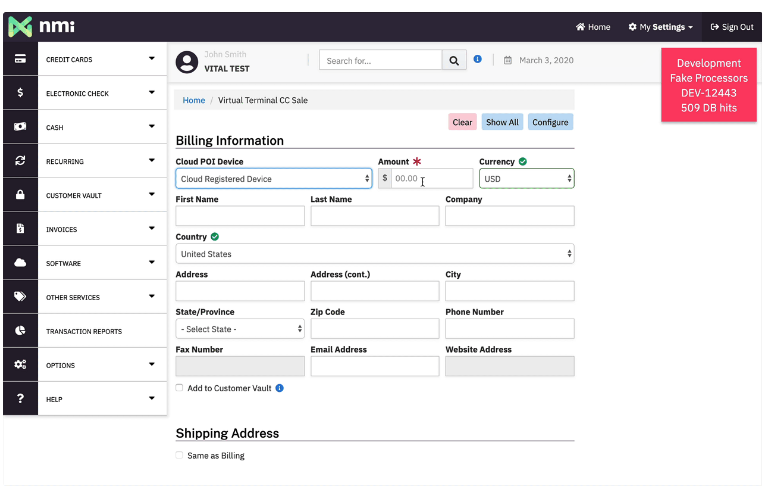

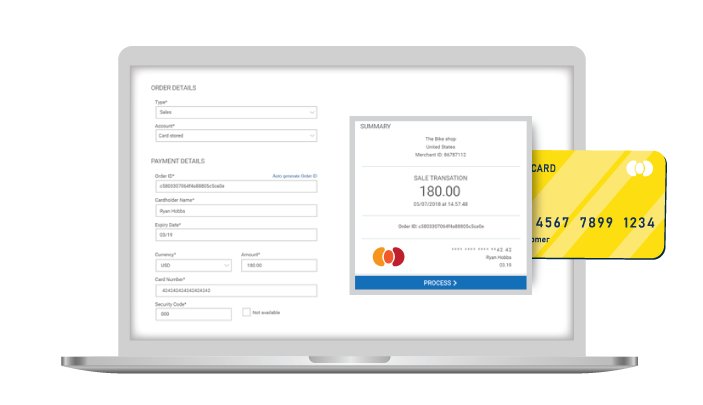

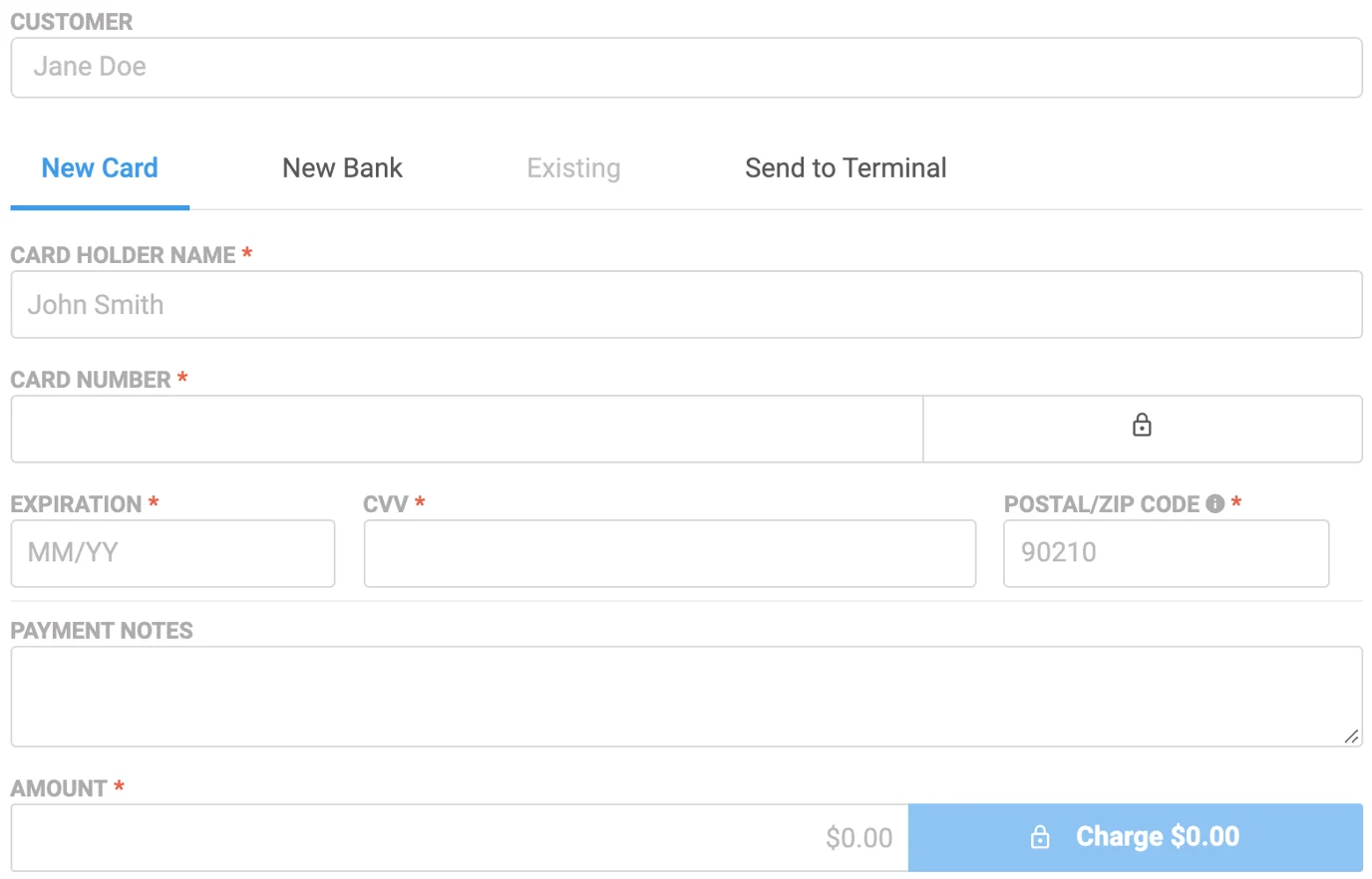

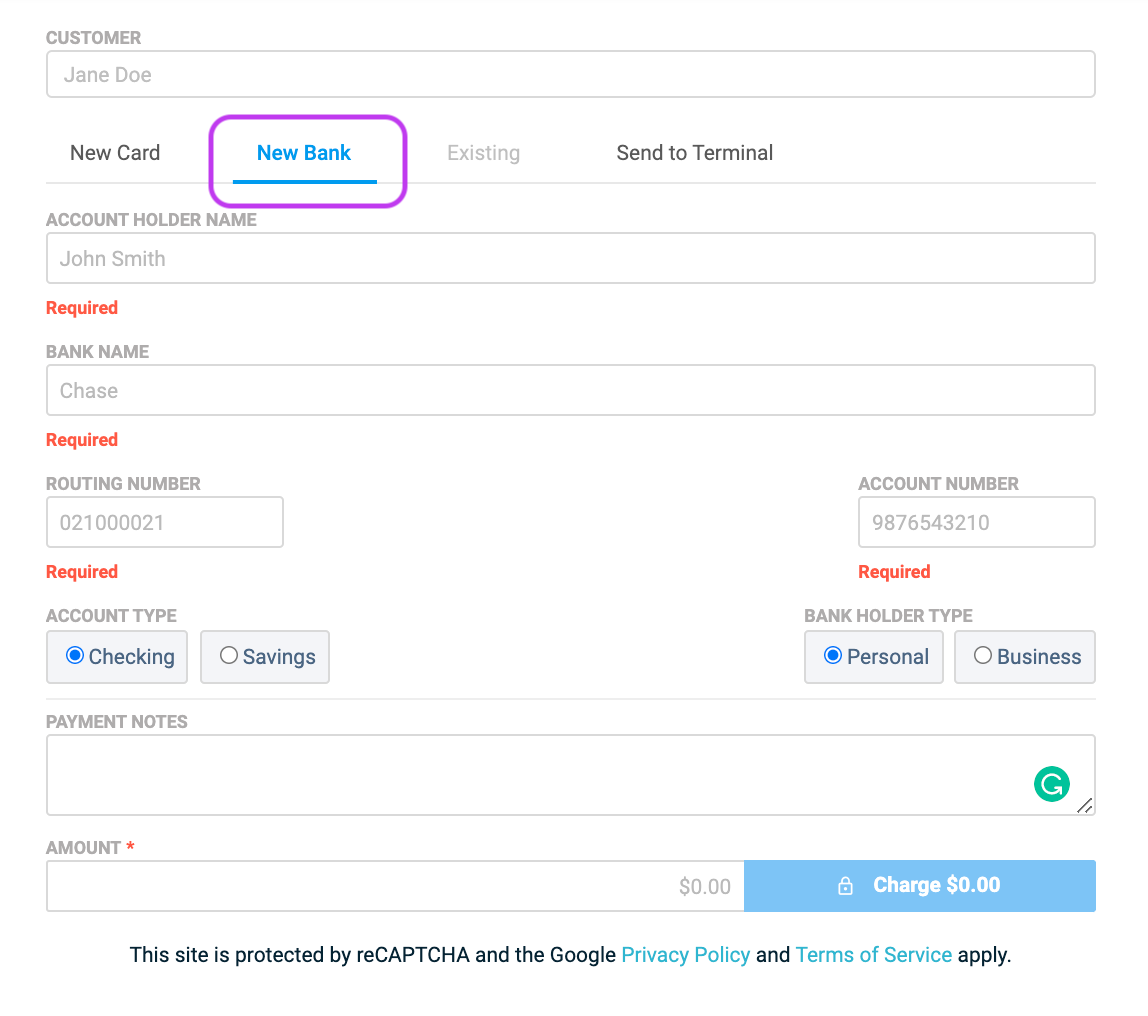

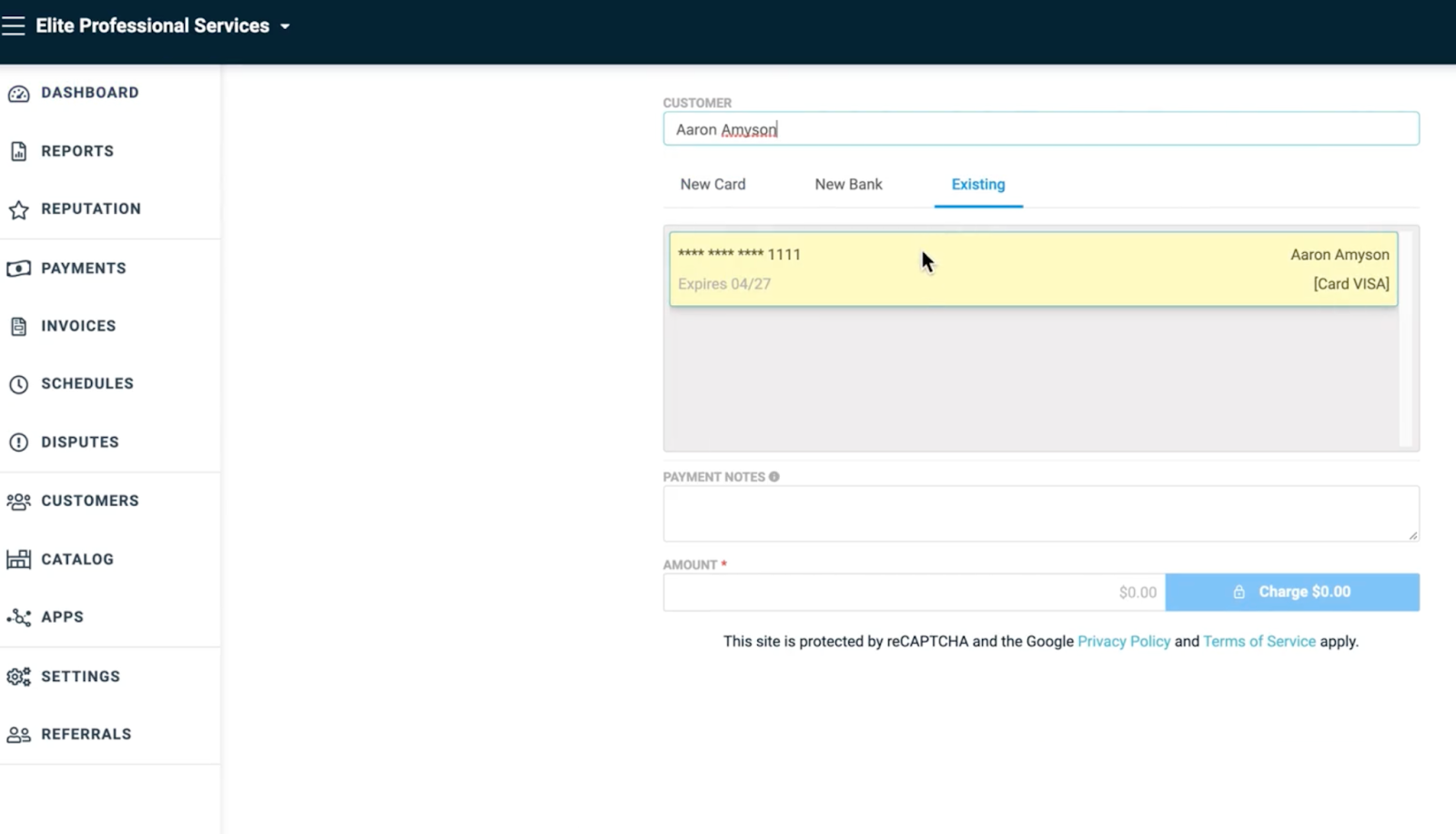

Virtual terminals are merchant-facing platforms that allow businesses to manually enter payment information and complete transactions on the customer’s behalf. This is especially useful for businesses that have customers who prefer to transact over the phone, via email, or messaging apps. Most payment processors come with a virtual terminal platform, but some offer better value for money and standout features.

As there are no one-size-fits-all solutions, I evaluated the top payment processors to help you choose an option that best matches your current goals.

Based on my evaluation, the best virtual terminals are:

| Best for | Monthly fee starts at | |

| Helcim | Minimizing fees | $0 |

| Payment Depot | Mid-size volume transactions | $0 |

| PaymentCloud | High-risk businesses | $10 |

| Stax | Wholesale transaction fees for large businesses | $99 |

| Square | Small and new businesses | $0 |

| PayPal | Accepting online international payments | $0 |

| CardX | Free credit card processing | $99 |

Best virtual terminals compared

| Our score (out of 5) | Merchant account fee | Virtual terminal (VT) fee | VT-supported payment methods | VT-supported transactions | |

| Helcim | 4.59 | $0 | $0 | Card, ACH, surcharging | One-time, invoice, B2B, international payments |

| Payment Depot | 4.46 | $0 | $0 | Card, ACH, surcharging | One-time, invoice, B2B |

| PaymentCloud | 4.43 | $10-$45 | $15-$45 | Card, ACH, surcharging | One-time, invoice, B2B |

| Stax | 4.42 | $99-$199 | $0 | Card, ACH, surcharging | One-time, invoice, B2B |

| Square | 4.33 | $0-$149 | $0 | Cash, card, ACH | One-time, invoice |

| PayPal | 4.27 | $0 | $30 | Credit and debit cards | One-time, invoice, international payments |

| CardX | 4.25 | $99+ | $0 | Credit and debit cards | One-time, invoice, B2B, |

Did you know?

Businesses can use virtual terminals without any additional hardware, so all you need is a computer or mobile device to log in to your merchant dashboard. However, card readers can be easily connected to process occasional in-person payments.

Consider the following questions as you go through my provider evaluations below:

- Can it work with your POS and other business systems?

- Is the software fee reasonable?

- Does it support transaction types and payment methods that your business needs?

- Does it support payment processing fit for your sales volume?

Helcim: Best overall virtual terminal (best for minimizing fees)

Overall Score

4.59/5

Pricing

5/5

Features

4.5/5

Support & Reliability

4.69/5

User Experience

4.69/5

Average User Review Scores

4.07/5

Pros

- No add-on or monthly fees

- Automated volume discounts

- Offers free credit card processing via surcharging

Cons

- Charges extra for AMEX transactions

- Application process not ideal for new businesses

Why I chose Helcim

Helcim is a traditional merchant account services provider known for its free and automated payment processing features, including a virtual terminal. You can use the virtual terminal to accept one-time and recurring payments from an unpaid invoice or simply from pulling up a customer profile. It can process credit card, ACH, and EFT payments. Plus, Helcim has tools for free credit card processing that you can access any time, which pass along the processing fees to your customers.

I chose Helcim for its strong cost optimization features. Aside from zero monthly fees and interchange plus rates, what makes Helcim stand out is its automatic volume discounts. In other words, your per-transaction fees will decrease automatically as your business scales and hits certain processing volumes. For B2B businesses, Helcim’s payment processing features automatically pull level 2 and 3 data so every qualified transaction can get discounted rates.

This makes Helcim the ideal solution for fast-growing small and mid-size businesses in industries like retail, professional services, automotive, healthcare, education, and wholesale.

Choose Helcim if: You want a low-cost virtual terminal with no monthly VT fee, interchange-plus pricing, ACH support, invoicing, recurring billing, and room to grow.

Avoid Helcim if: You are a brand-new business that needs instant approval or you prefer a flat-rate processor with minimal underwriting.

Related: B2B payments guide

- Monthly account fee: $0

- Virtual terminal fee: $0

- Manual entry transaction fee: Interchange plus 0.15% + 15 cents to 0.50% + 25 cents

- In-person transaction fee: Interchange plus 0.15% + 6 cents to 0.4% + 8 cents

- Domestic ACH transfers: 0.5% + 25 cents per transaction

- American Express transactions: Additional 0.10% + 10 cents

- Hardware cost: $99–$329

- Chargeback fee: $15

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: No long-term contract

Automatic volume discounts

Unlike some traditional merchant services providers, Helcim does not impose volume minimums or limits. Instead, it offers built-in discounts for sales above $50,000 per month (based on a three-month average). This ensures that businesses can always maximize savings without delay from having to request lower rates every time there is a significant increase in sales volume.

Free credit card processing

The fee-saving program is Helcim’s free credit card processing service. Users can choose to apply or remove this customer-facing fee at any time with a simple toggle feature. And like most of Helcim’s payment features, you won’t need to apply separately to qualify for this program. The fee saver is automatically available to Helcim clients that accept online ACH payments and those that use Helcim’s smart POS terminal, except for businesses located in Connecticut, Colorado, Maine, Massachusetts, Oklahoma, and Quebec.

Online invoicing and recurring billing

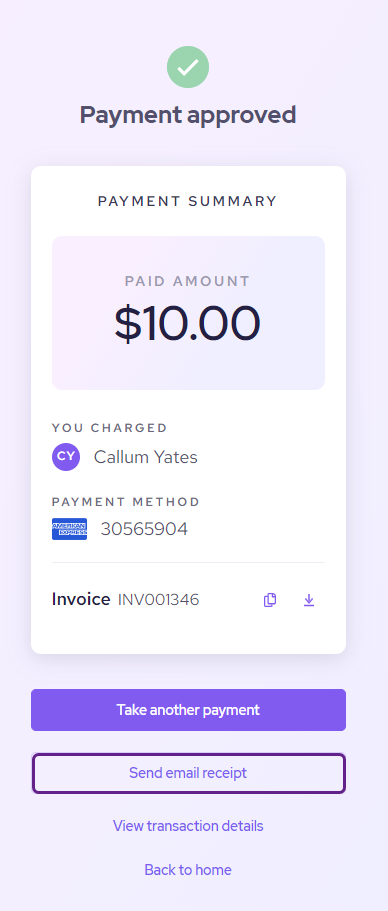

Helcim’s virtual terminal can be used to process unpaid one-time or recurring invoices. Users can initiate a payment by pulling up an unpaid invoice or specifying an invoice number in the payment form. The virtual terminal also comes with an address verification service (AVS) that helps protect businesses from chargebacks on card-not-present transactions.

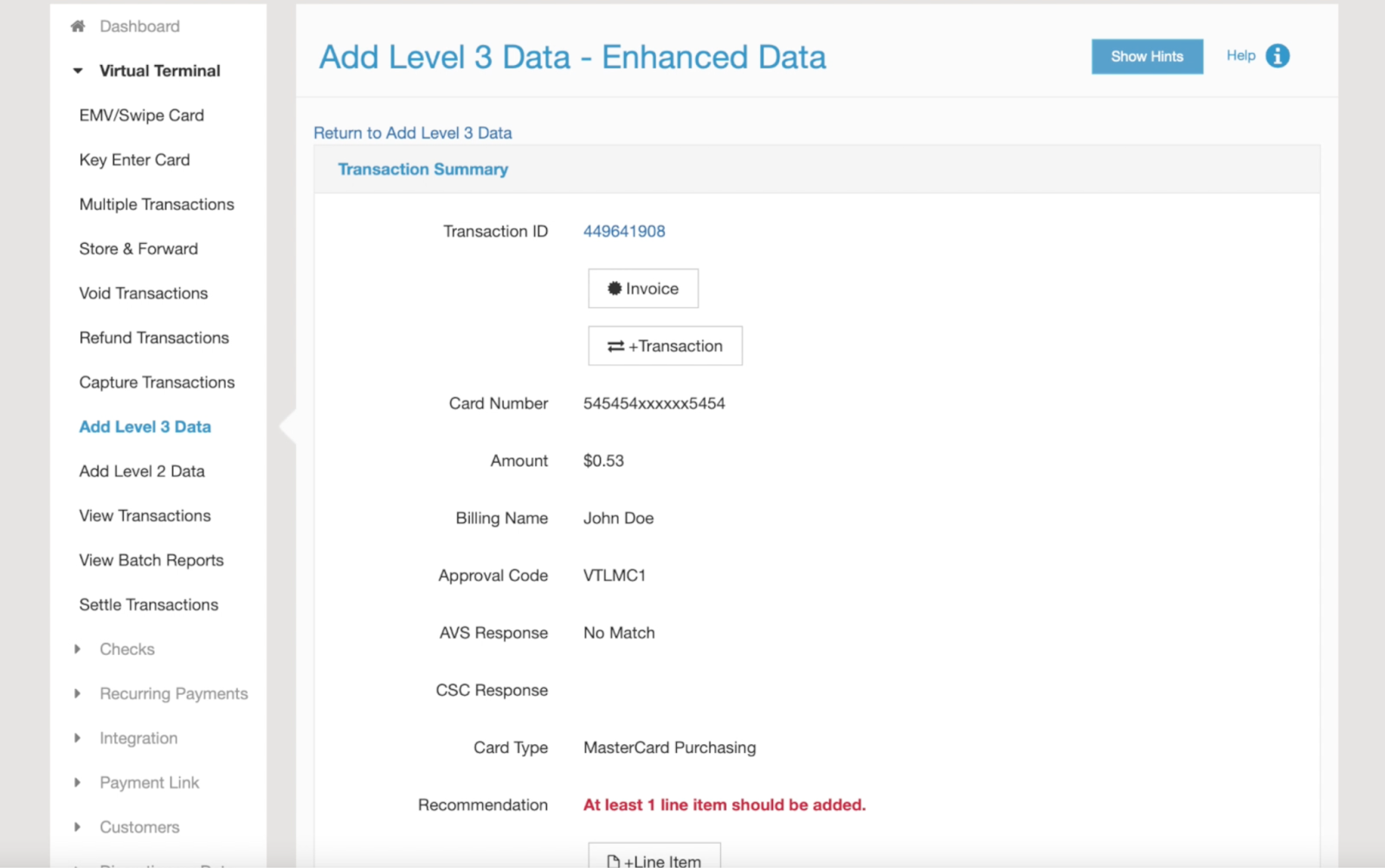

Automated level 2/3 data processing for B2Bs

As of December 2023, level 2 and 3 data processing are available for all Helcim clients. Again, this payment processing service does not require a separate application for users to qualify. Helcim’s level 2/3 interchange optimization feature can recognize cards that qualify for level 2/3 discounted rates and automatically retrieves the necessary additional transaction and customer information from the invoice and customer profile.

Payment Depot: Cheapest for mid-size volume transactions

Overall Score

4.46/5

Pricing

5/5

Features

4.25/5

Support & Reliability

4.38/5

User Experience

4.06/5

Average User Review Scores

4.63/5

Pros

- No monthly fees

- Custom interchange-plus rates

- Multiple virtual terminal integrations

Cons

- Only for U.S.-based businesses

- Lacks option for same-day funding

- ACH payment processing is an add-on

Why I chose Payment Depot

Payment Depot supports a variety of virtual terminal platforms from popular payment gateway integrations such as NMI, Authorize.net and PayTrace. There are no additional monthly fees, as Payment Depot’s custom pricing already includes every payment service that a business opts into, including a virtual terminal.

Until recently, Payment Depot operated under a similar subscription model (wholesale transaction rate + monthly fee) used by its parent company, Stax. It has since remodeled to custom interchange plus pricing. This makes Payment Depot more affordable and attractive to mid-size businesses that have yet to reach volume levels that can maximize savings with a monthly fee and wholesale rates.

Choose Payment Depot if: You process steady monthly volume and want custom interchange-plus pricing with access to multiple virtual terminal options, such as NMI, Authorize.net, or PayTrace.

Avoid Payment Depot if: You need same-day funding, built-in ACH without an add-on, or a processor that supports businesses outside the US.

- Monthly account fee: $0

- Virtual terminal fee: $0

- Manual entry transaction fee: Custom interchange plus rate

- In-person transaction fee: Custom interchange plus rate

- Hardware cost: Depends on hardware provider

- Chargeback fee: $25

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: No long-term contract

All-in-one software

Payment Depot users get unlimited access to the same all-in-one payment software by Stax without the high monthly account fees. This includes features such as digital invoicing, hosted payment pages, one-click shopping with catalog management, card vault, recurring and scheduled payments, and choice of virtual terminals.

Wide range of business and payments integration

Payment Depot comes with a wide range of business and payment integrations. It is compatible with most POS systems and hardware, such as Clover. Payment Depot can also integrate easily with popular ecommerce platforms, including Shopify.

Multiple virtual terminal options

Payment Depot works with a number of payment gateways and its virtual terminal features. You can choose from popular options such as NMI, Authorize.net, and PayTrace. This is especially useful to avoid any downtime for businesses migrating from other payment processors that use the same virtual terminal platform.

PaymentCloud: Best for high-risk businesses

Overall Score

4.43/5

Pricing

3.75/5

Features

4/5

Support & Reliability

4.69/5

User Experience

5/5

Average User Review Scores

4.7/5

Pros

- Works with high-risk businesses

- Flexible fee structure

- Payment gateway agnostic

Cons

- Monthly account fee

- Add-on monthly cost for virtual terminals

- Lacks same-day funding option

Why I chose PaymentCloud

PaymentCloud is a traditional merchant services provider that supports all types of payment processing methods. While it caters to nearly all business types, PaymentCloud is particularly known for its expertise in working with high-risk businesses, which no other provider in our list can do. Virtual terminals are in-demand among these business types because most of these companies accept mail-order/telephone-order (MOTO) payments.

I especially like PaymentCloud’s attention to detail when handling accounts for high-risk merchants. It works with clients right from the application to provide the highest chance of being approved for a merchant account. I also like PaymentCloud’s flexibility as it can customize its rates based on what a potential client is familiar with and adapt the customer’s current payment gateway platform avoiding business downtime.

Choose PaymentCloud if: You run a high-risk business, accept MOTO payments, or need help getting approved for a merchant account with gateway flexibility and chargeback support.

Avoid PaymentCloud if: You want transparent published rates, instant setup, or the lowest monthly software cost.

Please note

All of PaymentCloud’s pricing is fully customized. The figures below are estimates provided by PaymentCloud and can vary significantly depending on your business profile.

- Monthly account fee: $10–$45

- Virtual terminal fee: $15–45

- Manual entry transaction fee: 2%–$4.3%

- In-person transaction fee: 2%–$4.3%

- Hardware cost: Depends on hardware provider

- Chargeback fee: $25

- Application/set up fee: $0

- Cancellation fee: Waived

- Contract term: Mostly short-term

Payment gateway agnostic

PaymentCloud is compatible with all payment gateways—a huge deal for businesses that are considered high-risk. Because not all service providers can work with high-risk merchants, the payment types and payment methods in standard payment gateways are not readily available to them. This makes migrating to a new merchant services provider a struggle for high-risk businesses without payment gateway agnostic and high-risk experts like PaymentCloud.

Customizable pricing

PaymentCloud’s flexibility includes its ability to adapt a potential client’s pricing structure, which is why pricing is primarily custom quoted. If a business is more familiar with flat rate pricing, or if a large high-risk business prefers a subscription-based model to maximize its savings, PaymentCloud can design a pricing plan to fit its needs.

High-risk business expertise

PaymentCloud possesses the industry knowledge needed to help high-risk businesses successfully get approved for a merchant account. It works with a number of banks and financial institutions that are capable of shouldering the chargeback risk involved in accepting credit card payments. PaymentCloud offers the highest level of fraud protection, risk management, and customer support that high-risk businesses need to stay compliant and avoid cancellation of their merchant accounts.

Stax: Cheapest, wholesale transaction fees for large businesses

Overall Score

4.42/5

Pricing

4.69/5

Features

4.5/5

Support & Reliability

4.69/5

User Experience

4.38/5

Average User Review Scores

3.83/5

Pros

- Wholesale transaction fees

- No long-term contract

- Text2pay feature

Cons

- High monthly fees

- Lacks same-day funding option

- ACH payment processing is an add-on

Why I chose Stax

Stax is a popular merchant services provider, offering wholesale interchange rates ideal for high-volume businesses. Its virtual terminal is built into Stax Pay, allowing businesses to accept card and bank payments, set recurring transactions, send invoices, payment links, and even SMS to collect payments.

What’s also great about Stax is that it offers a range of products that can easily keep up with fast-growing businesses and large, enterprise-level companies. For example, Stax Bill offers advanced billing and recurring payment services for businesses that run subscriptions. There’s also Stax Connect for software vendors that want to integrate an end-to-end payment processing service to their software platforms (SaaS).

Choose Stax if: You process enough volume to justify a monthly subscription and want wholesale-style transaction pricing with strong invoicing, recurring billing, and reporting tools.

Avoid Stax if: You process low or inconsistent monthly volume. The monthly fee can outweigh the savings if your virtual terminal use is occasional.

Learn more: Cheapest credit card processing companies

- Monthly account fee: $99–$199

- Virtual terminal fee: $0

- Manual entry transaction fee: Interchange + 18 cents

- In-person transaction fee: Interchange + 8 cents

- Hardware cost: Depends on hardware provider

- Chargeback fee: $25

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: No long-term contract

All-in-one payment software

Stax provides an all-in-one payment software, Stax Pay, that comes with every merchant account. This feature facilitates everything from integrating with card terminals to generating high-level analytics and reports. Businesses can use Stax Pay to add checkout carts on ecommerce platforms, generate payment links for embedded payments, initiate manual payments on a virtual terminal, and create invoices.

Wide range of business integrations

Aside from POS systems, Stax Pay can be integrated with popular business systems such as QuickBooks, Salesforce, and Calendly. This allows users to sync various tasks to its virtual terminal functions, such as manually collecting outstanding receivables, integrating customer profiles, and setting appointments over the phone that require partial payments.

Advanced payment processing features

Large, enterprise-level businesses often require more specialized payment processing tools. Stax offers different products that support these needs, such as Stax Connect, an end-to-end payment processing integration with SaaS platforms used by large nonprofits, educational institutions, and professional services. For subscription-based businesses, Stax also offers Stax Bill, which can automate large-scale accounts receivable and billing management tasks.

Square: Best for new and small businesses

Overall Score

4.33/5

Pricing

4.06/5

Features

4.5/5

Support & Reliability

4.06/5

User Experience

4.38/5

Average User Review Scores

4.67/5

Pros

- Free POS software

- No monthly fees for payment processing

- Waived chargeback fees

Cons

- Not the cheapest transaction fees

- Invoicing customization for a fee

- Account stability issues

Why I chose Square

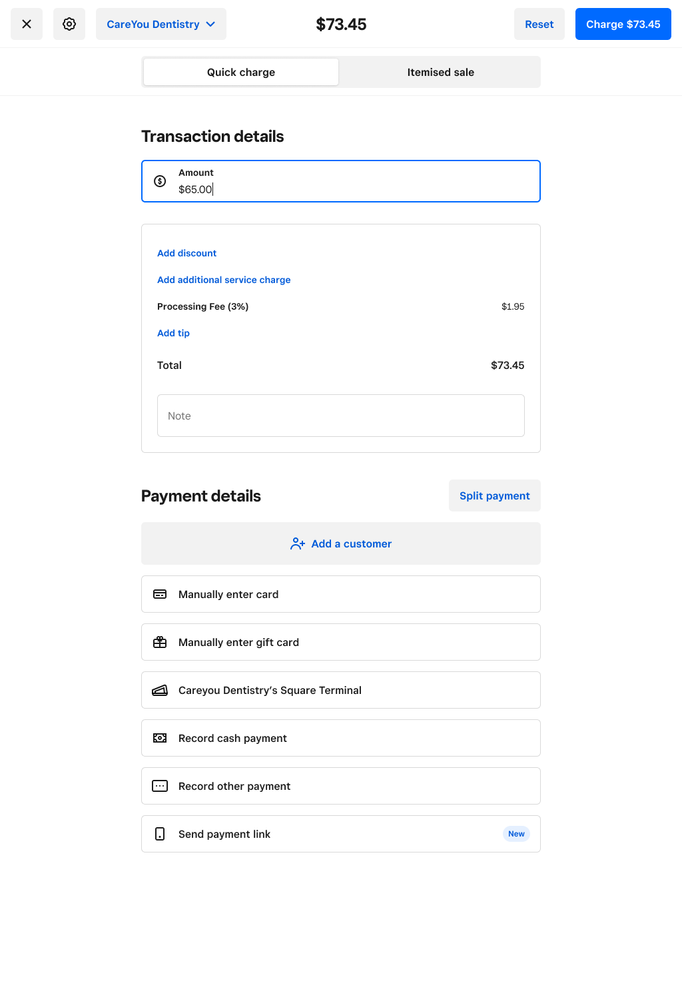

Square is the ideal all-in-one business solution for new businesses. There are no monthly fees for using its payment processing service, which comes built into Square’s suite of POS software. Square’s virtual terminal is also free with every merchant account and can just as easily handle all the payment methods supported by the other providers on our list. You can use it to manually enter card information, record a cash or check payment, and send a payment link. But what makes Square stand out from the rest is its overall small and new business friendly features.

Unlike Helcim, Payment Depot, PaymentCloud, or Stax, there is no application process to go through with Square, making it ideal for startups that don’t have a payment processing history. I particularly like how Square offers an all-in-one business solution of POS, hardware, ecommerce, and payments processing with the most feature-rich free account you’ll ever find in the market today. And while flat rate fees are not as cost-effective as interchange plus rates, this pricing structure is simple to manage particularly for new merchants. Square even offers proprietary business management tools, most of which you can get for free.

For larger businesses, Square now has an enterprise solution that allows you to create customized POS and payment processing platforms that will work with your current business set up. You can also qualify for custom rates if you process more than $250,000 in annual sales. However, note that you can only process ACH payments on Square’s virtual terminal if the transaction goes through an invoice. And while you can accept credit card payments from other countries, you will only be able to hold funds in your local currency.

Choose Square if: You are a new or small business that wants a free virtual terminal, fast setup, built-in POS tools, invoices, payment links, customer profiles, and simple flat-rate pricing.

Avoid Square if: You process high monthly keyed-in volume or need custom underwriting, high-risk approval, or the lowest possible interchange-plus rates.

Learn more: Best mobile credit card processors

- Monthly account fee: $0-$149 (includes POS software)

- Virtual terminal fee: $0

- Manual entry transaction fee: 3.5% + 15 cents

- Payment link generated via VT: 3.3% + 30 cents

- In-person transaction fee: 2.6% + 15 cents

- Hardware cost: $0-$299

- Chargeback fee: Waived up to $250/month

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: No long-term contract

All-in-one POS system

Square is an all-in-one POS system with a built-in payment processor. Additionally, Square offers a suite of business management tools, such as inventory, employee and payroll, loyalty and rewards, and CRM. Square also comes with a long list of third-party integrations, such as accounting, delivery, and project management tools.

Chargeback management

Square’s merchant dashboard includes a chargeback and dispute management feature. Businesses can receive chargeback alerts, respond to communications, and upload documents all from the Square dashboard.

CBD program

New businesses that intend to sell CBD products (hemp and hemp-derived CBD products that have less than, or equal to, 0.3% THC) can apply for Square’s CBD program where it is legal in the U.S. This is especially useful for businesses on a limited budget looking for a fast and easy setup, although expect higher transaction rates and some additional requirements before getting approved for an account.

PayPal: Best for accepting online international payments

Overall Score

4.27/5

Pricing

3.75/5

Features

4.25/5

Support & Reliability

3.75/5

User Experience

5/5

Average User Review Scores

4.6/5

Pros

- Free merchant account

- Fast set up and no long-term contract

- Supports multi fiat and cryptocurrencies

- Free instant access to funds via PayPal balance

Cons

- Monthly fee for virtual terminal

- Does not support ACH payments on virtual terminal

- Access to recurring billing features w/fee

- Not covered by PayPal Seller Protection policy

Why I chose PayPal

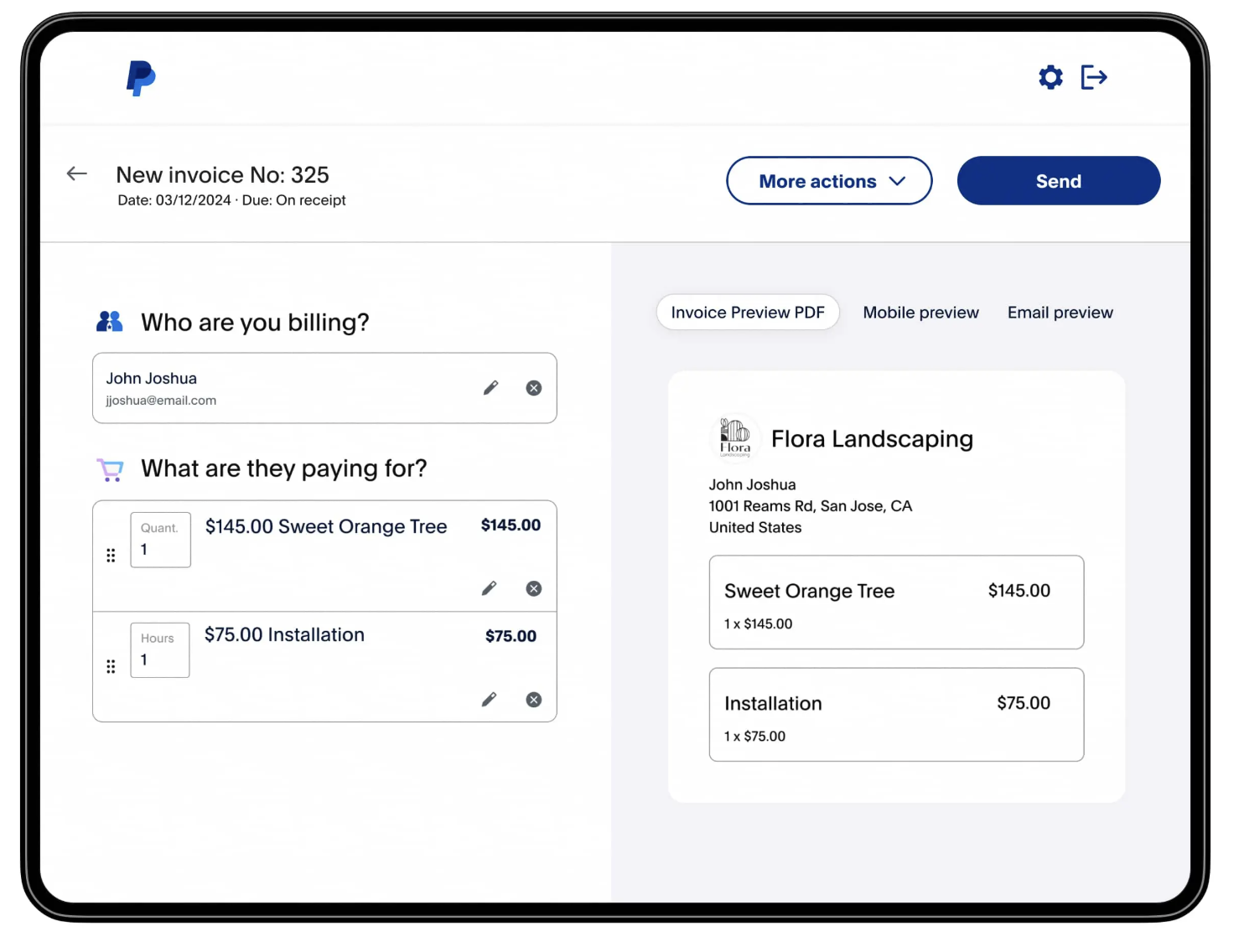

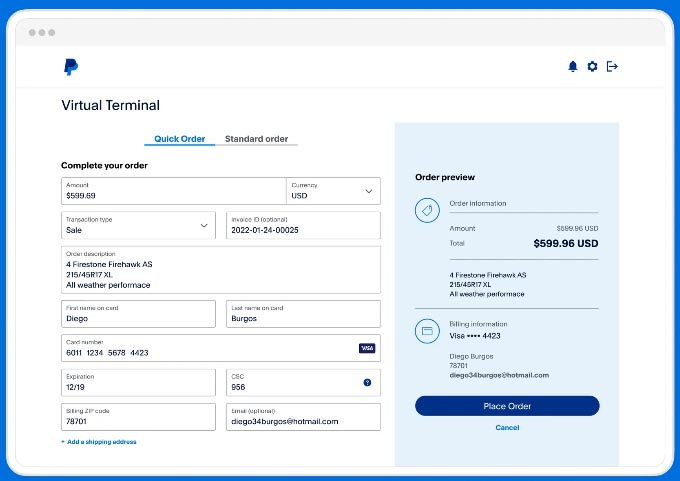

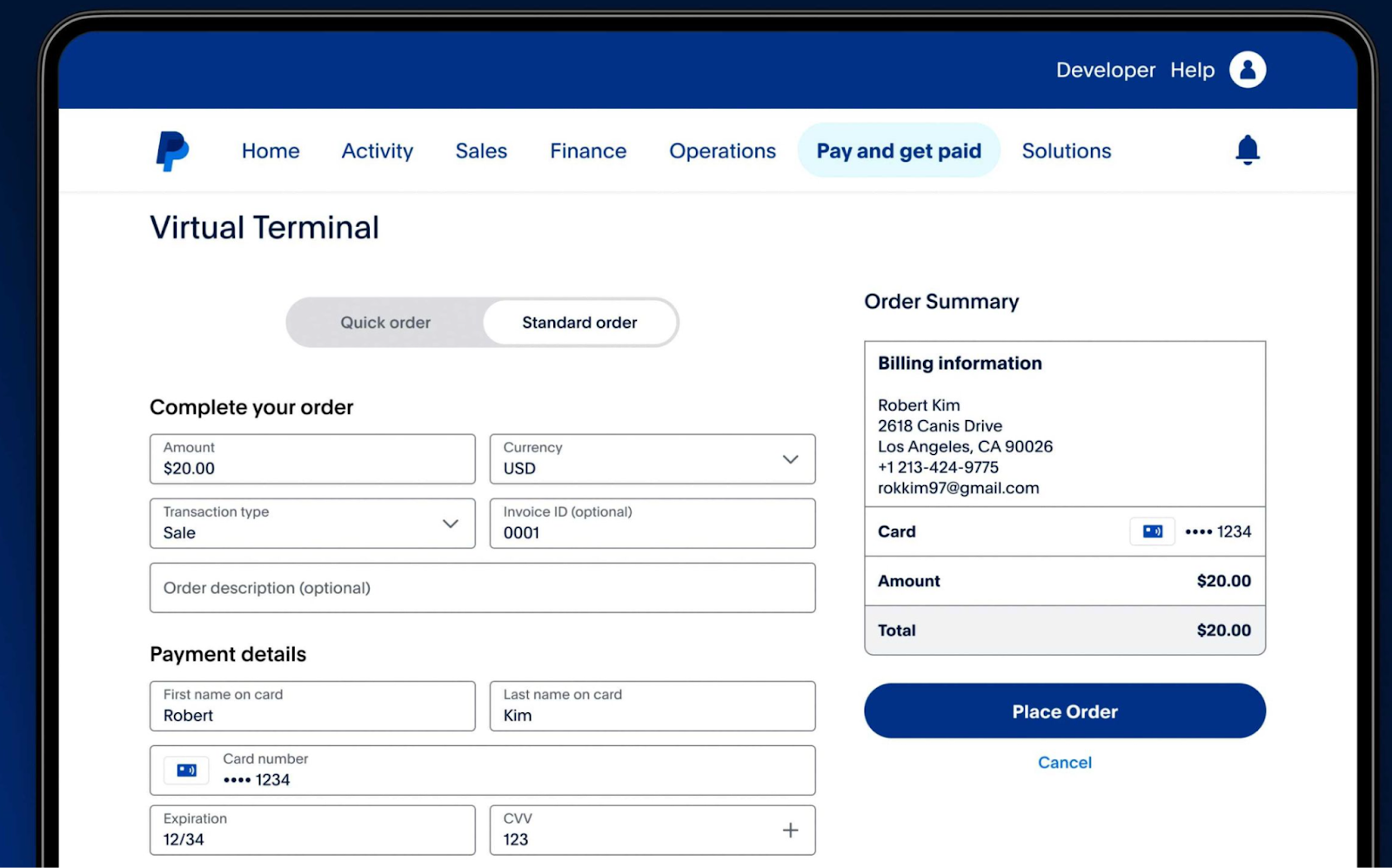

PayPal is the pioneer of mobile payment platforms and the most trusted brand with over 400 million active users around the globe to date. Like Square, the merchant account is easy to set up and free to use with no long term contracts. And while it can’t match Square’s versatile POS software options, PayPal stands out among my list of providers for its ability to handle 100+ currencies, making it the best mobile payment solution for businesses that accept international payments.

As a virtual terminal I particularly like PayPal because of how easy it is to use. While I can say the same for other contenders like Helcim, Square, and CardX which I all tried, PayPal’s layout and interface is simply more user-friendly. Whether you are preparing a quick manual order, pulling an outstanding invoice, or creating an invoice within the virtual terminal itself, all you need to do is choose a different option from the choices in the dropdown boxes. Plus, you also get instant access to your funds from your PayPal balance.

A few caveats if you choose PayPal though: First, its virtual terminal can only process credit and debit card payments unless you use PayPal enterprise to upgrade the service with developer tools. Second, unlike Square and Helcim, PayPal charges a monthly fee to use the virtual terminal platform. Third, manual payments processed on the customer’s behalf are not covered by PayPal’s seller protection policy so make sure to have solid chargeback protection protocols in place to protect you from fraudulent claims.

Choose PayPal if: You need a recognizable payment brand for remote and international customers, or you already use PayPal for online payments and want to keep payment activity in one ecosystem.

Avoid PayPal if: You mainly need a low-cost US virtual terminal. The monthly VT fee and transaction costs can make PayPal less competitive than no-monthly-fee providers.

Related: Best online payment processors

- Monthly account fee: $0

- Virtual terminal fee: $30 per month

- Manual entry transaction fee: 3.09% + 49 cents

- In-person transaction fee: 2.29% + 9 cents

- Invoicing: 3.49% + 9 cents

- Crossborder fee (for international payments): +1.5% per transaction

- Recurring billing tools: +$10 per month

- Hardware cost: From $29 (discounted mobile card reader)

- Chargeback fee: $20 for transactions not processed through a buyer’s PayPal account or through guest checkout

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: Pay as you go

International payments

PayPal is known for its ability to accept international payments, handling 100+ currencies for more than 200 countries. You can use the virtual terminal to collect one-time transactions over the phone or manually process outstanding invoices for customers across the globe.

Discount for charities

PayPal offers discounted transaction rates of 1.99% + 49 cents per transaction to qualified nonprofits. Use the virtual terminal to accept pledges and donations over the phone and create digital receipts to send to your donors.

Instant access to funds

PayPal gives you instant access to funds in two ways. You can access it for free via your PayPal balance which can be used for online payments or opt for instant funding to your linked business bank account for an additional fee.

CardX: Best for free credit card processing

Overall Score

4.25/5

Pricing

4.69/5

Features

4/5

Support & Reliability

4.69/5

User Experience

4.38/5

Average User Review Scores

3.5/5

Pros

- Automated surcharging

- Built-in invoicing and virtual terminal

- Exclusive Mastercard partner

Cons

- Charges a monthly fee

- Some limitations on invoicing tools

- Lacks same-day funding

Why I chose CardX

CardX is the leading expert in credit card surcharging services and is the exclusive surcharging partner for Mastercard. It comes with built-in invoicing and a virtual terminal feature that users can access at no extra cost. CardX also provides businesses with the necessary surcharging signage and staff training to assist with start-up.

I chose CardX primarily for its credit card surcharging service. While other merchant account service providers in this list, like Helcim and PaymentCloud, also offer this feature, it’s hard to ignore CardX’s expertise. This makes CardX an overall more reliable solution for businesses where credit card surcharging is a key consideration.

However, like PayPal, CardX only supports credit and debit card payments, which is partly why the two land at the tail end of this buyers’ guide. CardX also charges a monthly merchant account fee which may be a deal breaker for those looking to minimize their monthly operating expenses, but keep in mind that the surcharging means there are no transaction fees to be paid unless your customer uses a debit card. CardX also does not charge extra for its subscription/recurring billing tools which will cost you an additional $10 per month with PayPal.

Choose CardX if: You want a virtual terminal built around surcharging and need automated tools to help pass eligible credit card processing costs to customers.

Avoid CardX if: You operate in a state or industry where surcharging is restricted, or you do not want customers to see added card fees at checkout.

- Monthly account fee: $99+

- Virtual terminal fee: $0

- Manual entry transaction fee: From 2.91% for debit card payments

- In-person transaction fee: From 2.91% for debit card payments

- Hardware cost: $375–$540 (plans available)

- Chargeback fee: $0

- Application/set up fee: $0

- Cancellation fee: $0

- Contract term: No long-term contract

Compliance

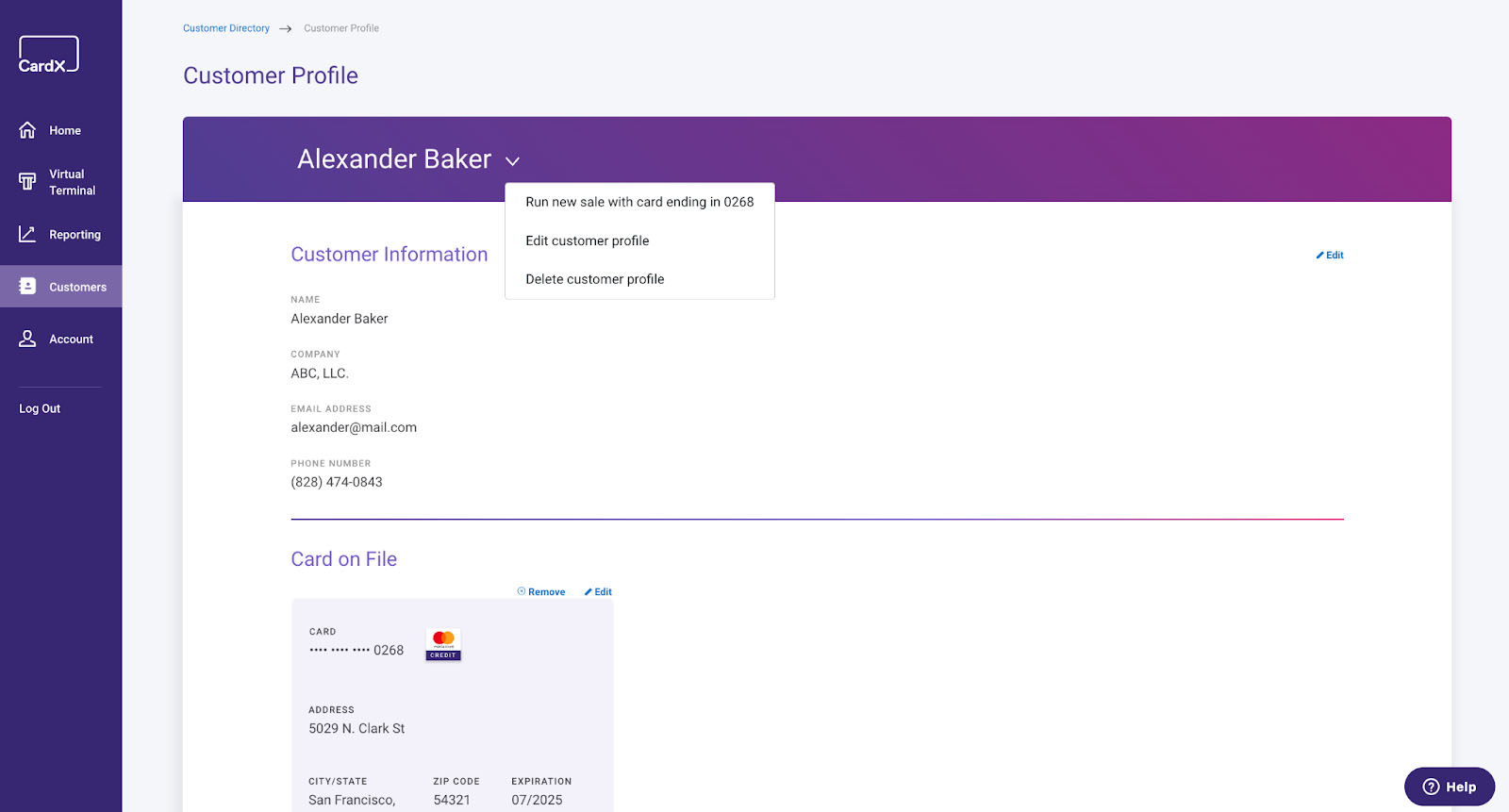

CardX strictly adheres to surcharging guidelines. It stays on top of industry developments and ensures that its system is always up to date on state regulations. The CardX merchant dashboard also comes with fraud monitoring and protection settings that allow users to fine-tune fraud detection rules based on their comfortable risk level.

Billing and invoicing

The CardX virtual terminal can be used to manually charge one-time and recurring transactions. It also has a CRM feature that collects customer data, including payment information. Transaction records are also available, making it possible to initiate transactions from the customer profile.

Online payment processing

CardX supports online payment processing tools like any other merchant service provider. It can generate payment links and design checkout pages via Lightbox to integrate with your ecommerce websites. CardX also comes with API integrations to provide more advanced customizations.

Finding the right virtual terminal for your business

Virtual terminals allow you to manually enter payment information on the customer’s behalf, as well as create shareable payment links to add on websites, social media posts, or send to customers via email and instant messaging platforms.

But while not all virtual credit card processing terminals are the same, there are key features you should look for when narrowing your list for the best option:

Virtual terminal cost examples

Virtual terminal pricing depends on the provider’s monthly fee, keyed-in transaction rate, chargeback fees, and whether ACH, invoicing, or recurring billing are included. The cheapest option is not always the one with the lowest monthly fee. A free virtual terminal can be a better fit for low-volume businesses, while interchange-plus or subscription pricing may save more as processing volume grows.

| Scenario | Best fit to consider | Why |

| New business processing occasional phone payments | Square | Square has no monthly virtual terminal fee, simple setup, and built-in tools for invoices, payment links, customer profiles, and reporting. The tradeoff is that keyed-in payments use a higher flat rate. |

| Growing SMB processing regular invoice, phone, or B2B payments | Helcim | Helcim has no monthly virtual terminal fee and uses interchange-plus pricing with automatic volume discounts. It is a stronger fit when savings matter more than instant setup. |

| Mid-size business with steady monthly volume but not enough to justify a high subscription fee | Payment Depot | Payment Depot’s custom interchange-plus pricing and multiple virtual terminal options can work well for businesses that want lower processing costs without Stax’s higher monthly starting price. |

| Large business processing high remote payment volume | Stax | Stax’s subscription-style pricing can make sense when transaction volume is high enough to offset the monthly fee. It is less attractive for low-volume businesses. |

| High-risk merchant taking MOTO payments | PaymentCloud | PaymentCloud is better suited for businesses that need underwriting support, flexible gateway options, and chargeback tools. Pricing is less predictable because it depends on the merchant profile. |

| Business that wants to pass credit card fees to customers | CardX | CardX is built around compliant surcharging workflows. Check state rules and card network requirements before using surcharging. |

As a rule of thumb, choose a no-monthly-fee option if you process occasional virtual terminal payments. Compare interchange-plus or subscription pricing if remote payments are a regular part of your revenue. For high-risk businesses, approval odds, chargeback support, and gateway flexibility may matter more than the lowest advertised rate.

Related: 7 Best credit card processing companies