ACH payment processing is an electronic payment method that moves funds directly between bank accounts through the Automated Clearing House (ACH) network. Instead of charging a credit card, ACH payments pull money from a customer’s bank account, which typically results in lower processing costs for businesses.

For small businesses, SaaS companies, and B2B teams that send invoices or collect recurring payments, ACH can be a practical way to reduce fees and improve payment reliability. In this guide, we’ll cover how ACH payment processing works, what it costs, the pros and cons to consider, and how to choose the right provider for your business.

Key takeaways

- ACH payment processing moves money directly between bank accounts through the ACH network.

- It usually costs less than credit card processing, making it a strong option for recurring billing and large invoices.

- ACH is commonly used by small businesses, SaaS companies, and B2B teams for subscriptions, invoices, and vendor payments.

- Settlement is slower than card payments (typically one to three business days), but fees are often lower.

- The best ACH payment processors vary by business type, but top options include Square, Stripe, and Helcim.

What is ACH payment processing?

At its core, ACH payment processing is a way to move money electronically from one bank account to another, without using a card network. Businesses use it to collect payments, send payouts, and automate recurring billing through the Automated Clearing House (ACH), the US system that handles batch bank transfers.

Unlike credit card payments, ACH transactions don’t go through card networks like Visa or Mastercard. This is why they typically come with lower processing costs, making them especially useful for recurring payments, high-value transactions, and B2B invoicing.

Related: Retail Payment Processing

How ACH differs from other payment methods

ACH is often compared to other electronic payment methods, but each serves a different purpose depending on speed, cost, and use case.

- Credit cards: Faster and widely accepted, but come with higher processing fees and chargeback risk.

- Wire transfers: Processed individually and typically settle the same day, but are more expensive and better suited for large, one-time transactions.

- Real-time payments (RTP): Instant bank transfers, but not yet as widely available as ACH, and may come with higher costs or limitations.

In comparison, ACH sits in the middle — it’s slower than cards and wires but significantly more affordable, which makes it a strong fit for recurring billing and predictable payment flows.

Related: Cheapest Credit Card Processing Providers

Common types of ACH payments

ACH payments can be categorized based on how funds are initiated and transferred. Understanding these payment types helps businesses choose the right setup, whether they’re collecting recurring payments or sending funds efficiently.

| ACH payment type | How it works | Common use cases |

|---|---|---|

| ACH debit (pull payments) | A business pulls funds from a customer’s bank account with prior authorization | Subscriptions, recurring billing, loan payments, utilities |

| ACH credit (push payments) | The payer sends funds to another bank account | Payroll, vendor payments, refunds |

| eChecks (electronic checks) | A digital version of a paper check processed as an ACH debit | Online checkouts, invoice payments |

How does ACH payment processing work?

ACH payments move through a structured, batch-based system, which is why they cost less than card transactions but take longer to settle. Instead of being authorized and funded instantly, ACH transactions are grouped and processed in scheduled windows throughout the day.

Here’s the typical flow from authorization to settlement:

- Payment authorization

The customer authorizes the transaction, either by entering their bank details online, signing an ACH authorization form, or agreeing to recurring billing terms. This authorization is required under NACHA rules and serves as the legal basis for the transfer.

- Submission to the payment processor (ODFI)

Once authorized, the payment request is sent to the business’s ACH processor or payment provider. The processor then forwards the transaction to the business’s bank, known as the Originating Depository Financial Institution (ODFI).

- Batch processing through the ACH network

The ODFI submits the transaction into the ACH network, where payments are grouped into batches and routed for processing. Unlike card payments, ACH is not processed one transaction at a time in real time.

- Receiving bank review (RDFI)

The customer’s bank — called the Receiving Depository Financial Institution (RDFI) — receives the ACH request and verifies the account details and available funds. If the account is valid and funded, the transaction is approved. If not, it may be returned with an ACH return code (such as insufficient funds).

- Settlement and funding

Once approved, funds are transferred and deposited into the business’s account. Most ACH payments settle within one to three business days, though some providers offer same-day ACH for an additional fee.

ACH payment timeline at a glance

While the exact timing depends on the processor and bank cutoffs, most ACH transactions follow this pattern:

- Day 0: Customer authorizes payment

- Day 1: Transaction is submitted and processed through ACH

- Day 2-3: Funds settle and become available in the business account

Because ACH is batch-based, it’s best suited for planned payments like subscriptions, invoice collections, and recurring billing, not urgent or instant transactions.

ACH payment processing fees and costs

One of the biggest reasons businesses choose ACH is cost. Compared to credit card processing, ACH fees are usually lower and more predictable, especially for recurring payments and high-ticket invoices.

Most ACH payment processing companies use one of three pricing models:

Flat fee per transaction

This is the most common ACH pricing model. You pay a fixed amount for each transaction, often in the range of $0.20 to $1.50 per payment. Flat-rate pricing is easy to forecast and usually the most cost-effective option for larger transactions, since the fee stays the same regardless of payment size.

Percentage-based pricing

Some providers charge ACH fees as a percentage of the transaction amount, typically around 0.5% to 1%, often with a maximum cap (for example, $5 per transaction). This model can work for smaller payments, but costs can add up quickly on larger invoices if there’s no cap.

Monthly platform fees

In addition to transaction fees, some providers charge a monthly fee for ACH access, advanced billing tools, or gateway services. These fees can range from $10 to $50+ per month, depending on the platform and features included.

ACH vs credit card processing costs

ACH is generally much cheaper than credit card processing. Card payments typically cost 2.5% to 3.5% per transaction, plus fixed fees, while ACH often costs less than 1% or a flat amount under $1.

That cost difference becomes significant as payment amounts increase. For example, a $5,000 invoice paid by card could cost $125 to $175 in processing fees, while the same payment via ACH may cost only a few dollars.

Hidden ACH fees to watch for

Even though ACH is low-cost overall, there are a few extra fees that can catch businesses off guard:

- Return fees: Charged when a payment is rejected due to insufficient funds, invalid account details, or authorization issues.

- NSF (non-sufficient funds) fees: A common type of return fee when the customer’s account doesn’t have enough money to cover the payment.

- Chargeback or dispute-related fees: ACH doesn’t have traditional card chargebacks, but unauthorized returns and disputes can still result in penalties.

- Same-day ACH fees: If you need faster settlement, many processors charge an extra fee for same-day ACH transfers.

Before choosing a provider, check the full pricing schedule, not just the advertised transaction rate. The lowest ACH fee doesn’t always mean the lowest total cost, once monthly and exception fees are included.

Pros and cons of ACH payment processing

ACH payment processing is a strong option for businesses that want to lower payment costs and automate recurring billing, but it comes with tradeoffs in speed and payment reliability. Here’s a quick side-by-side view:

Pros

- Lower processing costs than credit cards, especially for high-ticket payments

- Ideal for recurring billing and subscription payments

- Reduced chargeback risk compared to card payments

Cons

- Slower settlement times (typically 1-3 business days)

- Higher risk of returns due to insufficient funds (NSF)

- Requires bank authorization and NACHA-compliant consent

In general, ACH is best for businesses that prioritize cost savings and predictable billing cycles, while card payments remain better for instant approvals and faster funding.

ACH vs other payment methods

ACH is often compared to other electronic payment options, especially when businesses are deciding between cost, speed, and customer convenience. While no single method is best for every situation, understanding the differences can help you choose the right mix for your payment strategy.

Here’s how ACH payment processing compares to other common payment methods:

| Payment type | ACH | Credit cards | Wire transfers |

|---|---|---|---|

| Speed | 1-3 business days | Instant approval; 1-2 days funding | Same day |

| Cost | Low | High (2.5%-3.5%) | High (flat fees per transfer) |

| Best for | Recurring billing, B2B payments, large invoices | Retail, ecommerce, everyday transactions | Large, time-sensitive payments |

ACH stands out for its affordability, making it a strong choice for businesses that handle recurring payments or high-value transactions. Credit cards, on the other hand, offer speed and convenience, while wire transfers are best reserved for urgent or high-value transfers where timing is critical.

Alternatives to ACH: FedNow, RTP, and other bank transfer options

ACH is still the default choice for low-cost bank-to-bank payments, but it is not the only option. For businesses comparing speed, reach, and settlement models, the closest alternatives are Same Day ACH, the FedNow Service, the RTP network, and wire transfers.

| Payment option | Speed | Availability | Similar to ACH | What makes it different |

|---|---|---|---|---|

| ACH | 1-3 business days; same-day options are available in some cases | Business-day processing | Direct bank-to-bank transfers with broad US account reach | Batch-based rather than instant. |

| Same Day ACH | Same business day, often within hours | Business-day processing windows | It still runs on the ACH Network and follows the same basic model | Faster than standard ACH, but not real-time or 24/7. |

| FedNow Service | Seconds | 24/7/365 | It also moves money directly between bank accounts | Funds are available immediately, the service supports instant interbank clearing and settlement, and banks can enable features, such as requesting for payment. |

| RTP network | Seconds | 24/7/365 | It is also an account-to-account bank payment rail | Payments are final and irrevocable, funds are made available immediately, and the network supports requests for payment messaging. |

| Fedwire / wire transfers | Same day; processed in real time during service hours | Mon-Fri, 9 p.m.-7 p.m. | It is still a bank-to-bank transfer | Each payment is processed individually with immediate, final settlement, making it better suited to urgent or mission-critical transfers. |

The simplest way to think about it is this: standard ACH is the low-cost default, Same Day ACH is the faster ACH option, FedNow Service and RTP are the instant-payment alternatives, and wire transfers are the high-urgency option. ACH also still has the broadest reach, while FedNow Service and RTP depend on participating financial institutions.

Top ACH payment processing companies (2026)

The best ACH payment processing solutions vary depending on your business model, transaction volume, and technical needs. Some providers focus on ease of use and all-in-one tools, while others offer more flexibility, lower costs, or support for high-risk industries.

Here’s a side-by-side comparison of top ACH providers to help you quickly evaluate your options:

| Provider | Best for | Starting monthly fee | ACH processing rate | Key ACH features |

|---|---|---|---|---|

| Square | Small businesses and omnichannel sellers | $0 | 1%, minimum of $1 | Bank payments with invoicing, integrated POS and ecommerce, recurring billing tools |

| Stripe | Developers and SaaS | $0 | 0.8%, $5 cap | ACH debits, micro-deposit verification, recurring billing, customizable APIs |

| Helcim | Transparent pricing | $0 | 0.5% + $0.25, $6 cap | ACH payments with low per-transaction fees, invoicing, recurring billing |

| PaymentCloud | High-risk businesses | Custom | Varies | ACH processing with dedicated merchant accounts, fraud monitoring, flexible underwriting |

| Stax | High-volume businesses | $99+ | $0.60 per transaction | ACH + card processing, advanced reporting, subscription billing tools |

Square stands out for its all-in-one ecosystem, combining ACH payments with POS, invoicing, and subscription tools in a single platform. Stripe is a strong choice for SaaS and tech-driven businesses that need customizable workflows, while Helcim offers some of the most transparent and affordable pricing.

For businesses in high-risk industries, PaymentCloud provides more flexible approval options and hands-on support. Meanwhile, Stax is best suited for companies processing large volumes that can benefit from subscription-based pricing.

Choosing the right provider ultimately depends on how you plan to use ACH, whether for recurring billing, B2B payments, or as part of a broader payment stack.

Related:

How to choose the best ACH payment processing company

Choosing the right ACH payment processing software depends on how your business accepts payments, your risk profile, and how much you want to automate billing. While most providers offer similar core functionality, the differences in pricing, approvals, and integrations can significantly impact your overall costs and workflow.

Here are the key factors to consider when evaluating your options:

Pricing structure

ACH pricing can vary widely between providers. Some charge a flat fee per transaction, while others use percentage-based pricing with caps or monthly subscription models.

If you process large payments, look for capped or flat-rate pricing to keep costs predictable. For smaller transactions, a percentage-based model may be more practical. Always review additional fees, such as returns or same-day ACH, to understand the total cost.

Approval requirements

Not all businesses are approved at the same rates. Traditional providers may have stricter underwriting, while others specialize in high-risk industries like CBD, gaming, or subscription-based services.

If your business operates in a high-risk category, choosing a provider like PaymentCloud that offers hands-on underwriting can improve your chances of approval.

Integrations and compatibility

Your ACH provider should work seamlessly with your existing tools. Look for integrations with:

- POS systems (for in-person payments)

- Ecommerce platforms (for online checkout)

- Accounting software (like QuickBooks or Xero)

- CRM systems (for customer and billing management)

An all-in-one platform like Square can simplify operations, while providers like Stripe offer more flexibility through APIs.

Recurring billing support

If you plan to use ACH for subscriptions or installment payments, make sure your provider supports automated billing. Features and tools to look for that can reduce manual work and improve payment collection rates include:

- Scheduled payments

- Saved bank account details

- Invoice automation

- Retry logic for failed payments

Risk tolerance and business type

Some providers are better suited for standard, low-risk businesses, while others are designed to support higher-risk industries with more flexible underwriting and fraud monitoring.

Choosing a provider that aligns with your risk level can help you avoid account holds, sudden terminations, or unexpected fees.

Quick checklist

Use this checklist to narrow down your options:

Common use cases for ACH payment processing

ACH payment processing is widely used for transactions that are recurring, high-value, or predictable. It is best suited for payment scenarios where cost savings and automation matter more than instant settlement, making it a go-to option for recurring and B2B transactions. Here’s how businesses typically use ACH:

| Use case | How ACH is used | Why it works well |

|---|---|---|

| B2B payments | Sending and receiving invoice payments, vendor payouts | Lower fees than cards or wires; ideal for large transactions |

| Subscription billing | Automatically collecting recurring payments for SaaS, memberships, or services | Reduces failed payments and supports automated billing |

| Payroll and contractor payments | Direct deposit for employees, freelancers, and reimbursements | Faster and more secure than paper checks |

| Rent and utilities | Recurring payments for rent, utilities, and insurance | Predictable billing cycles with automated collection |

ACH payment processing risks and compliance

ACH payment processing requires businesses to follow network rules, collect valid customer authorization, and manage returns and fraud risk. For most businesses, compliance comes down to three things: getting authorization right, keeping return rates under control, and using fraud controls that match how you collect bank payments.

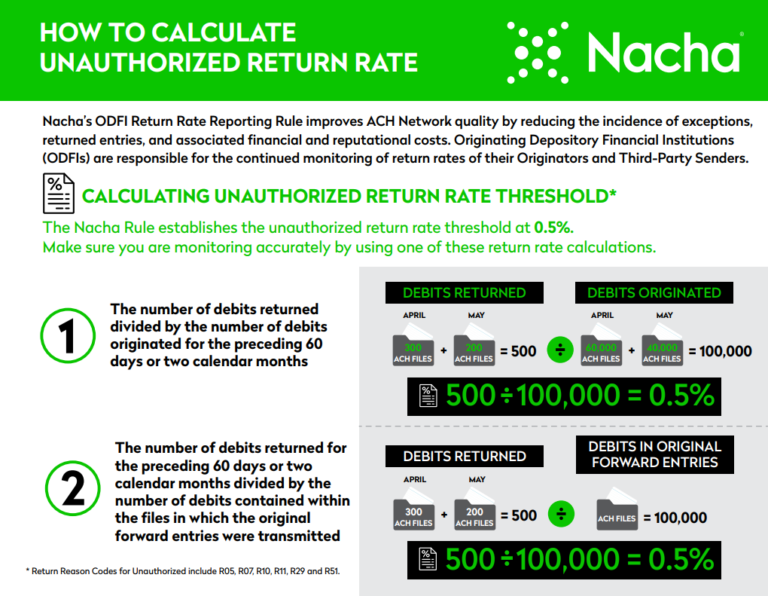

Nacha sets the operating rules for the ACH Network, and its compliance program can escalate violations through inquiries, warnings, and fines. Unauthorized debit returns are one of the biggest watch points; Nacha’s threshold for those returns is 0.5%.

Nacha rules overview

At a high level, Nacha’s rules govern how ACH entries are authorized, transmitted, returned, and corrected. In practice, the issues that draw the most scrutiny are unauthorized entries, invalid account numbers, and incorrect returns.

Authorization requirements

Authorization is the foundation of ACH compliance. For consumer debits, the authorization must be clear and readily understandable, comply with applicable law, and spell out the key terms of the payment, including timing and amount.

The customer must receive a copy, and the business must be able to produce proof of authorization if its processor or originating bank asks for it. A common failure point is weak proof of authorization — for example, when the authorization record does not match the account holder being debited.

Return codes and disputes

ACH exceptions are handled through return codes. For consumer disputes, the two most important codes are R10, which means the debit was not authorized, and R11, which means an authorization existed but the debit did not match its terms, such as the wrong amount or settlement date.

R11 claims still require a Written Statement of Unauthorized Debit and use a 60-day return window, but they also matter operationally because the underlying error may sometimes be corrected and resubmitted without a new authorization.

Fraud considerations

Fraud and operational risk often overlap in ACH. For online consumer debits (WEB entries), Nacha requires account validation as part of a commercially reasonable fraud-detection system before the first use of an account number or before a changed account number is used.

Beyond that, businesses should verify customer identity, use secure channels when sharing authorization or exception documents, and keep routing and account data current to reduce failed payments, avoidable returns, and added exception costs.

How to set up ACH payment processing

Setting up ACH payment processing is usually straightforward, but the exact setup depends on whether you choose an all-in-one platform or a provider that requires separate underwriting and gateway tools. In most cases, the process looks like this:

- Choose an ACH payment processor

Start by selecting a provider that fits your business model, transaction volume, and billing needs. If you want simplicity, look for a platform that combines ACH, invoicing, and recurring billing in one system. If you need more customization or high-risk support, you may need a more specialized provider.

- Apply for a merchant account (if needed)

Some ACH payment processing companies require underwriting before you can accept bank payments. This step may include a business application, bank verification, and a review of your processing history. Others, like all-in-one payment platforms, may handle this behind the scenes.

Related:

- Set up your payment gateway or software

Once approved, connect ACH to the tools you already use, such as your payment gateway, invoicing software, ecommerce platform, or billing system. This is also where you’ll configure payment forms, customer authorization language, and any recurring billing settings.

Related: Best Payment Gateways

- Enable ACH in checkout or invoicing

After setup, turn on ACH as a payment option wherever customers pay you. That may be at online checkout, on invoices, through a customer portal, or as part of an automated billing workflow. Make sure the payment experience clearly explains that funds will be pulled from a bank account.

Related: 10 Best Ecommerce Platforms for 2026

- Test and go live

Before rolling it out fully, run a few test transactions to confirm that authorizations, bank account verification, notifications, and settlement timing all work as expected. Once everything is in place, you can begin accepting live ACH payments.

For most businesses, the biggest setup decisions come down to provider fit, underwriting requirements, and how ACH will be used, whether for one-time invoices, recurring payments, or both.

Frequently asked questions (FAQs)

ACH payment processing is the electronic transfer of money between bank accounts through the ACH Network. Businesses use it for bank payments such as direct deposit, bill pay, recurring debits, and eChecks.

ACH payments can sometimes clear the same day, but most take one to three business days to complete. Same Day ACH is available for eligible payments and can settle within hours during business-day processing windows.

Yes. For consumer ACH debits, the authorization generally must be clear, readily understandable, and retained as proof, and the customer must receive a copy of the authorization.

An ACH debit pulls money from the receiver’s account, while an ACH credit pushes money into the receiver’s account. Direct deposit is a common ACH credit example, while recurring bill payments are a common ACH debit example.

Yes. ACH payments can be returned for reasons such as insufficient funds, no authorization, or a payment that does not match the authorization terms. Nacha uses R10 for debits the receiver says were not authorized and R11 for debits that were authorized but processed incorrectly, such as the wrong amount or wrong date.

ACH can be a secure payment method, but businesses still need strong controls. Nacha requires account validation for first-use or changed account numbers on online consumer debit entries, and consumers also have federal error-resolution rights for unauthorized electronic fund transfers.

ACH payments are processed in batches through the ACH Network, while wire transfers are processed individually through wire systems such as Fedwire. In general, ACH is better suited for routine and recurring bank payments, while wires are typically used for more urgent transfers.

Is ACH payment processing right for your business?

ACH payment processing is a good fit for businesses that want lower fees, recurring billing, and a cost-effective way to accept larger payments. It works especially well for B2B companies, SaaS businesses, and service providers that rely on invoices or subscriptions.

If you want to process ACH payments alongside cards, invoicing, and online payments, Square is a strong option for ACH payment processing for small businesses. See if Square is the right fit for your business.